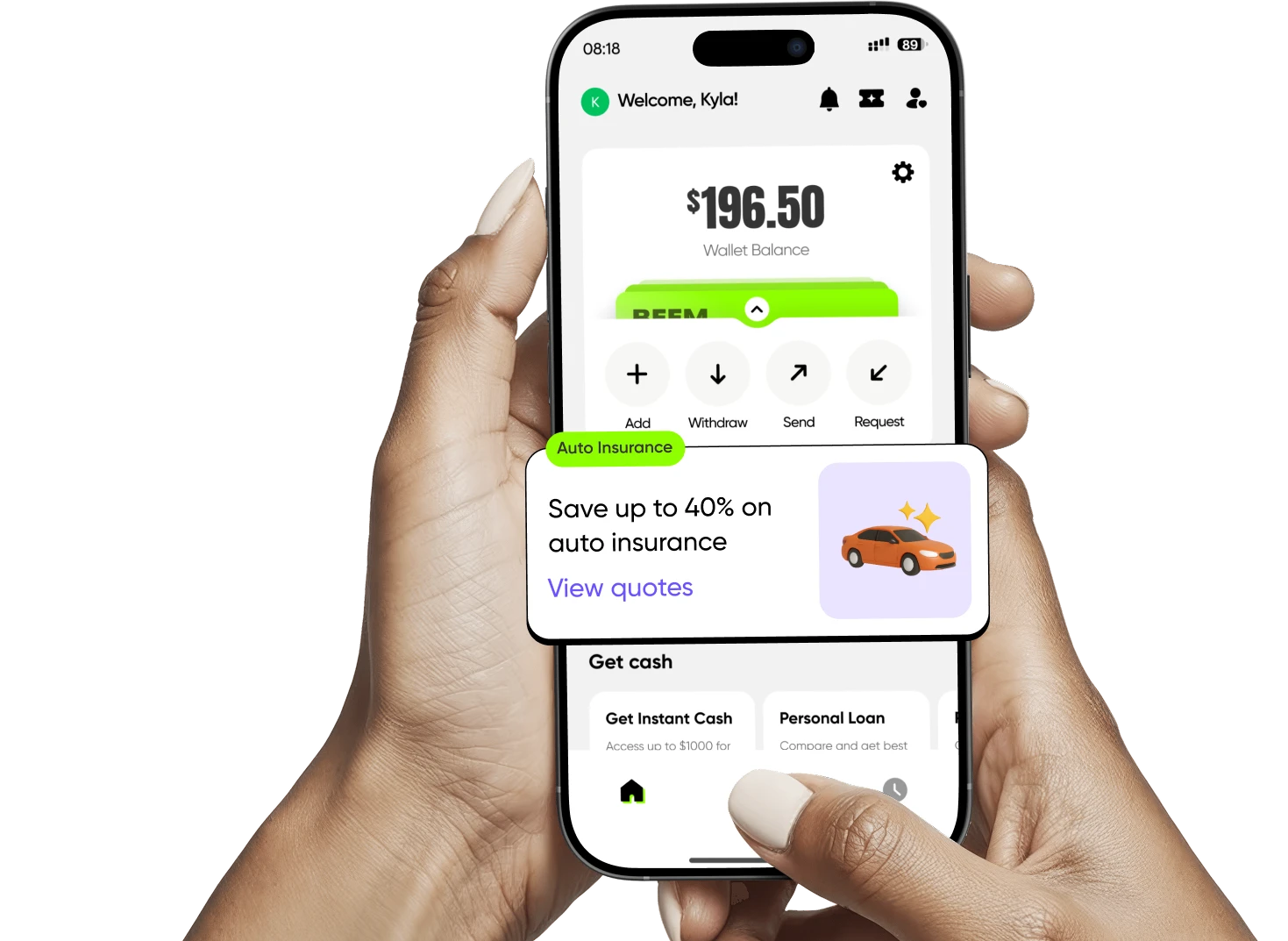

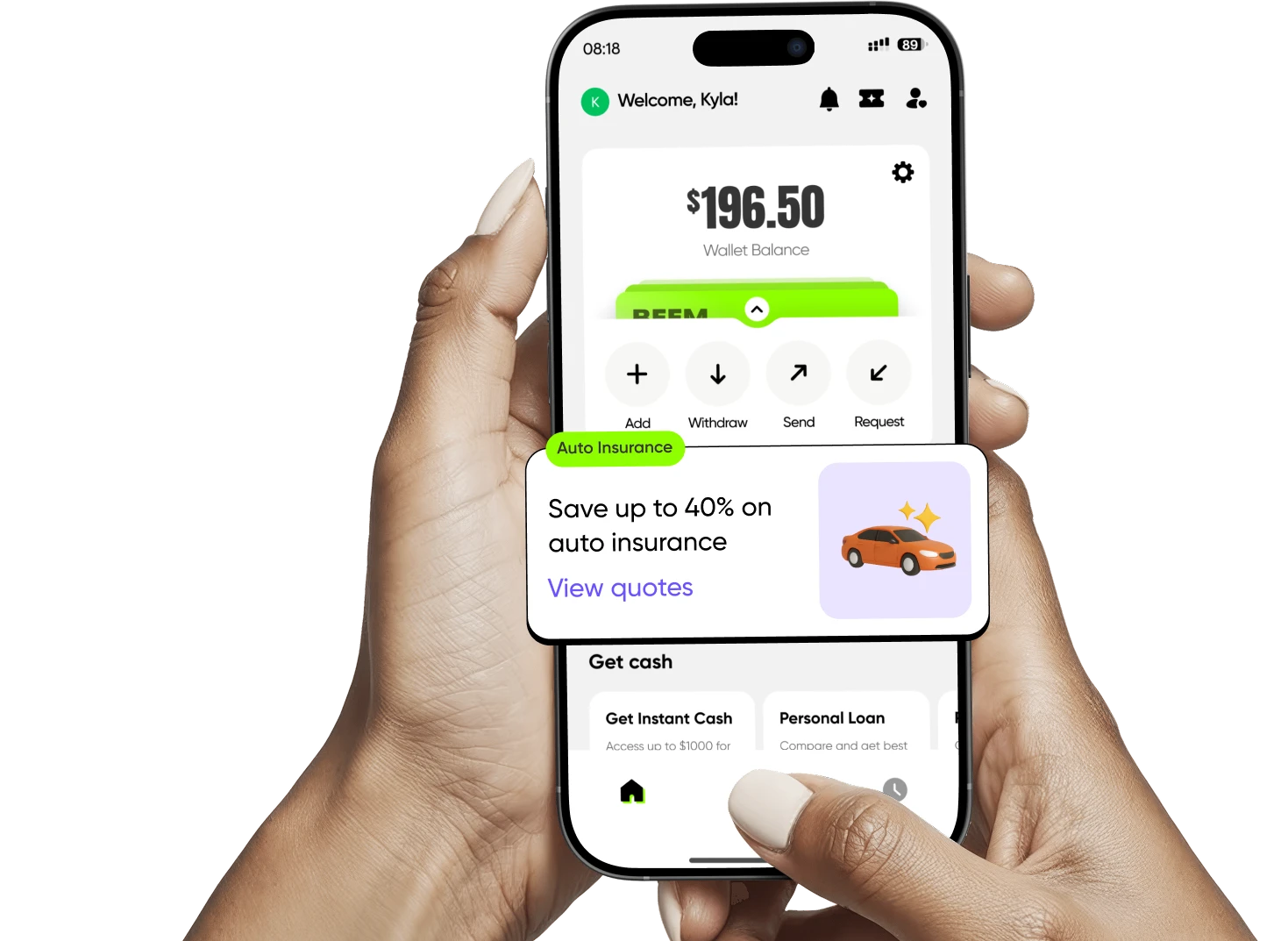

Save up to 40%

on car insurance

Get personalized car insurance quotes from industry leading insurance providers. Compare rates in one place.

+1

Insurance offerings

Personalized\n quotes In 5

mins

Get a quote tailored to your needs, based on

your driving habits and preferences

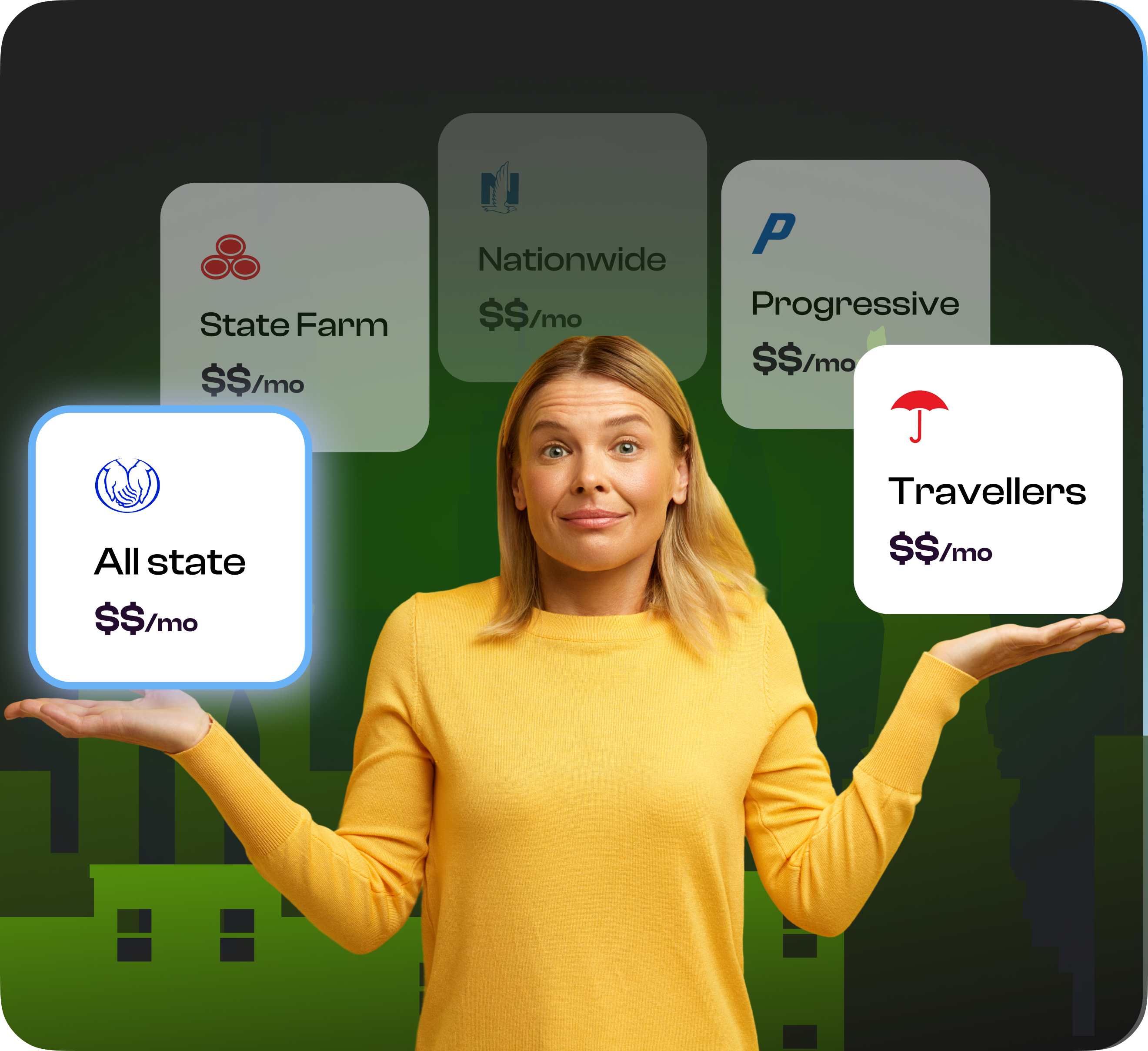

Compare rates

in one place

See the best car insurance rates from top

providers in one simple comparison

Drive safe &

save big

Safe driving habits pay off. Enjoy discounts on

your driving behavior and save on premiums

Why should you trust Beem?

- Beem is trusted by 5M+ users for their daily financial activities. Beem partners with the industry leading insurance companies to provide the best insurance quotes tailored to your needs.

Drive Safe and save up to

40% on car insurance!

40% on car insurance!

Life happens. Whether it’s for bills, family, or an unexpected

expense, Beem’s Everdraft™ is here when you need backup.

With Beem, I always know my money is going to successfully withdraw.

Renee S.

Secure and reliable I love that i can trust Beem with my financial needs always gets me funds when needed no stress about payback timing its peace of mind I really really need.

Breanna G.

Customer service rep Suresh Kashyap helped me fix an issue with multiple accounts by walking me through the required steps. About the app itself i liked the Everdraft option and the financial advice the app gave me.

Keri C.

I love use Beem app, it’s has variety of benefits not only just cash advance! I’m highly recommended for family and friends.

Amanda J.

They refer exclusively to other Beem offerings.

Do more with Beem

Fast personal loans, health program, & so much more!

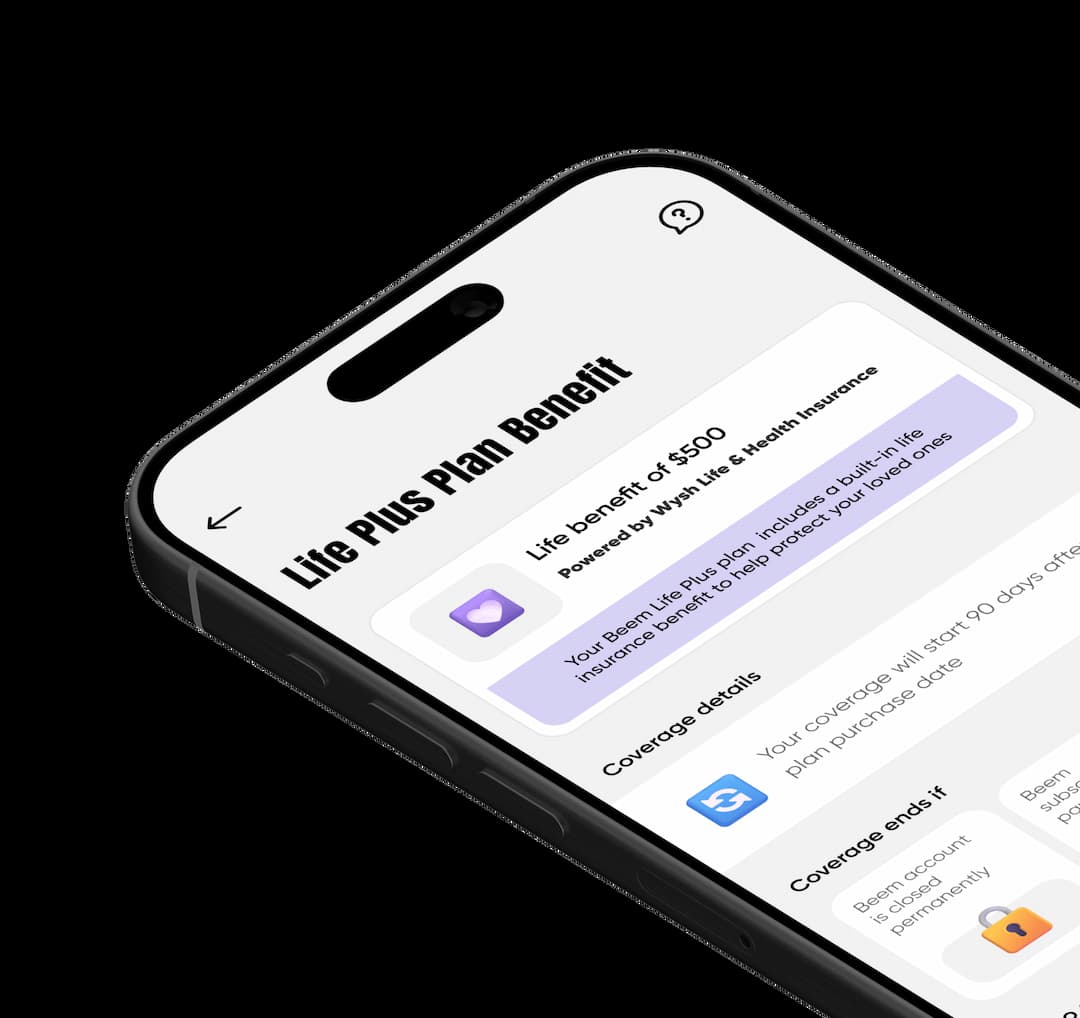

Life insurance that protects your family

No underwriting, no complex terms. Just protection with your Beem subscription.

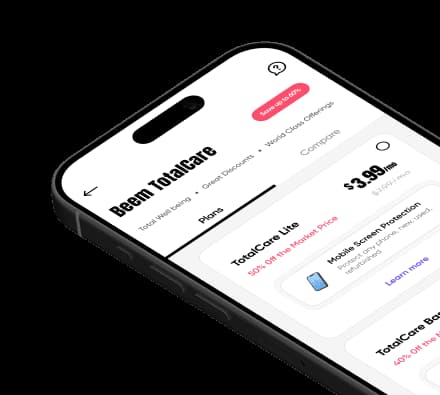

Boost your wellness & protect your devices

Get device protection, mental wellness, fitness, and online privacy

Life insurance that protects your family

No underwriting, no complex terms. Just protection with your Beem subscription.

Boost your wellness & protect your devices

Get device protection, mental wellness, fitness, and online privacy

Life insurance that protects your family

No underwriting, no complex terms. Just protection with your Beem subscription.

Boost your wellness & protect your devices

Get device protection, mental wellness, fitness, and online privacy