Your 2026 Guide

to Federal &

State Taxes

to Federal &

State Taxes

Navigate your taxes this year easily with Beem’s essential resources and tools

Estimate Your 2026

Tax Refund Fast with

Our FREE Tool!

Tax Refund Fast with

Our FREE Tool!

- Get an accurate and quick estimate for your 2026 federal and state tax returns, free of charge. Know your refund amount in a snap with our easy-to-use tool!

Why Trust Beem for Your Tax Resources?

Simplified Tax

Insights

We break down the essentials with easy-to-understand guides so you can file with confidence.

State-Specific

Tax Guidance

Find resources for your state, including tax rates, credits, and deadlines—all in one place.

Max Your Refund

with Smart Tips

Discover tax-saving strategies to ensure you keep more of your hard-earned money.

100% Accurate

Calculations

Use our FREE Income Tax Calculator to quickly estimate your federal and state tax returns.

Real-time Updates

You Can Trust

Our tax resources bring you the latest information to answer all your doubts.

Tax Deadlines

at a Glance

Never miss an important date again. Stay ahead with a clear calendar of tax deadlines.

Filing Taxes in 2026: A Complete Guide to Navigating Your Federal and State Taxes

Filing taxes is one of those responsibilities most people don’t think about until deadlines start approaching. By then, confusion around forms, deductions, credits, and changing rules can quickly turn tax season into a stressful experience.read more...

Filing taxes in 2026 comes with its own set of updates, adjustments, and planning considerations that every U.S. taxpayer should understand ahead of time.

Whether you’re a salaried employee, self-employed professional, gig worker, investor, or someone managing multiple income streams, having a clear understanding of how the tax filing process works can save you time, money, and frustration.

This complete guide breaks down everything you need to know about filing taxes in 2026, from what’s changed and how to file step by step, to avoiding common mistakes and making smarter financial decisions with your refund.

Tax laws are adjusted regularly to reflect inflation, economic changes, and policy updates. Filing taxes in 2026 means navigating several important updates that could affect how much you owe or how much you get back.

The IRS adjusts federal tax brackets each year to account for inflation. In 2026, income thresholds for each tax bracket are expected to be higher than previous years. This adjustment helps prevent “bracket creep,” where inflation pushes taxpayers into higher brackets without an actual increase in purchasing power.

While tax rates themselves may remain the same, the income ranges they apply to could shift. Understanding where your income falls can help you estimate your tax liability more accurately and plan ahead, especially if you expect a raise or change in income.

The standard deduction is also adjusted annually for inflation. In 2026, most taxpayers can expect a higher standard deduction compared to prior years. This means more income may be shielded from taxation without needing to itemize deductions.

For many filers, especially those without large mortgage interest or significant charitable contributions, the standard deduction will continue to be the simpler and more beneficial option.

Families should pay close attention to changes related to the Child Tax Credit. While exact eligibility rules and amounts depend on income thresholds and legislative updates, 2026 is expected to continue offering broader access for qualifying families.

This credit directly reduces the amount of tax owed and, in some cases, may be partially refundable. Understanding income limits and age requirements for dependents is key to claiming the full benefit.

Remote work remains common across many industries. While W-2 employees generally cannot deduct home office expenses, self-employed individuals and independent contractors may still qualify if they meet IRS requirements.

For those eligible, home office deductions can include a portion of rent, utilities, internet, and other home-related expenses used exclusively for business purposes.

Cryptocurrency taxation continues to evolve. In 2026, taxpayers must continue reporting crypto-related transactions, including selling, trading, staking rewards, and income earned through digital assets.

Even small transactions can trigger reporting requirements. Accurate recordkeeping throughout the year is essential to avoid underreporting income or miscalculating gains and losses.

You can start filing your 2026 federal income tax return for the 2025 tax year as soon as the IRS begins accepting returns. For 2026, that acceptance period typically begins in late January. The exact IRS start date is usually announced in early January but tends to fall around the last week of January each year.

Once the IRS opens the filing season, you can submit your return electronically or by mail. Filing early helps you get your refund sooner and reduces the chance of identity theft or errors caused by last-minute filing.

Keep in mind that while you can start filing as soon as the IRS opens, you should wait until you receive all necessary tax documents like your W-2, 1099s, and other income or deduction records to avoid amendments later. Filing with incomplete or incorrect information typically leads to delays or the need to file an amended return.

Filing taxes doesn’t have to be overwhelming if you approach it systematically. Following these steps can help ensure a smoother process from start to finish.

The foundation of accurate tax filing is having the right paperwork ready before you begin. Missing documents can delay filing or result in errors.

Common documents you’ll need include:

- W-2 forms from employers

- 1099 forms for freelance, gig, or contract work

- Bank interest statements

- Investment income statements

- Records of retirement contributions

- Student loan interest statements

- Health insurance coverage forms

- Receipts for deductible expenses if itemizing

Organizing these documents early makes filing faster and reduces the risk of mistakes.

Once you know your income and expenses, you’ll need to decide whether to take the standard deduction or itemize.

The standard deduction is simpler and works well for most taxpayers. Itemizing may make sense if your total deductible expenses exceed the standard deduction amount.

Common itemized deductions include:

- Mortgage interest

- State and local taxes (subject to limits)

- Charitable donations

- Medical expenses above the IRS threshold

Running both calculations can help you choose the option that lowers your tax bill the most.

Tax credits are one of the most valuable parts of the tax code because they reduce your tax bill dollar for dollar.

Some of the most relevant credits for 2026 include:

- Child Tax Credit

- Earned Income Tax Credit

- Education-related credits

- Energy efficiency credits for qualifying home improvements

Eligibility rules vary, so it’s important to review income limits and documentation requirements carefully.

Most taxpayers choose to file electronically, either through tax software or with the help of a tax professional. E-filing is faster, more secure, and reduces processing errors.

Paper filing is still an option, but it often results in longer processing times and slower refunds.

If your tax return shows a balance due, payment options include direct bank transfers, card payments, or mailed checks.

If paying the full amount isn’t possible, the IRS offers installment plans that allow you to pay over time. Filing on time, even if you can’t pay in full, helps reduce penalties.

Even small mistakes can cause delays, audits, or penalties. Being aware of common errors can help you avoid unnecessary issues.

Many taxpayers leave money on the table by overlooking credits or deductions they qualify for. Reviewing your situation carefully or using financial tools to track expenses throughout the year can help prevent this.

Simple errors like misspelled names or incorrect Social Security numbers can cause significant delays in processing your return.

Missing the filing deadline can result in penalties and interest. If you need more time, filing for an extension is better than not filing at all.

Marriage, divorce, a new child, or a change in employment can all affect your filing status and tax obligations. Make sure your return reflects these changes accurately.

Getting the largest refund possible often comes down to planning and awareness rather than last-minute filing.

Contributions to retirement accounts like IRAs or employer-sponsored plans can reduce taxable income, which may increase your refund or reduce what you owe.

Keeping organized records throughout the year makes it easier to identify deductions and credits when tax season arrives.

Your filing status affects tax brackets, deductions, and credits. Reviewing all available options can sometimes result in meaningful tax savings.

The time it takes to receive your tax refund depends on how you file your return and whether there are any issues that require extra review. For most U.S. taxpayers, refunds are issued fairly quickly when returns are filed correctly.

If you file your taxes electronically and choose direct deposit, the IRS typically issues refunds within 21 days. Many taxpayers receive their refund even sooner, especially when filing early in the tax season and submitting an error free return.

Electronic filing is the fastest option because it reduces processing delays and manual handling.

Paper filed tax returns take longer to process. Refunds for mailed returns usually take six to eight weeks, and sometimes longer during peak tax season.

Delays are more common with paper returns because they must be manually reviewed and entered into the system.

Several factors can slow down your refund, even if you file electronically:

- Errors or missing information on your return

- Claims for certain refundable credits that require extra verification

- Identity verification or fraud prevention reviews

- Filing late in the season when the IRS is processing high volumes

- If the IRS needs additional information, they will contact you by mail, which can extend the timeline.

To receive your refund as quickly as possible:

- File electronically instead of mailing your return

- Choose direct deposit rather than a paper check

- Double check all personal and financial information before submitting

- File early once you have all required tax documents

Accurate and early filing is the best way to avoid unnecessary delays.

Most taxpayers who file electronically can expect their refund within about three weeks. Paper filers should plan for a longer wait. While refund timing varies by situation, filing early, filing accurately, and using direct deposit significantly improve how fast you get your money.

A tax refund isn't free money—it's often a return of overpaid taxes. Still, it can be a powerful financial tool if used intentionally.

Using your refund to cover unexpected expenses can reduce reliance on credit cards or loans later.

Reducing balances on high-interest debt can improve your financial health long after tax season ends.

Putting part of your refund toward retirement or other long-term goals can help build financial security over time.

For most taxpayers, the federal filing deadline is Wed, April 15, 2026. If that date falls on a weekend or holiday, the deadline may shift slightly.

Filing an extension gives you until October 15, 2026, to submit your return, but any taxes owed are still due by the April deadline.

Beem is built to support everyday financial decisions, and that support becomes especially valuable during tax season. From staying organized throughout the year to accessing money when timing becomes an issue, Beem helps reduce the stress that often comes with filing taxes.

One of the biggest challenges during tax season is remembering what expenses qualify as deductions and finding proof for them. Beem helps you track spending in real time, making it easier to identify expenses that may be deductible.

Instead of sorting through months of bank statements, you can review categorized transactions and stay prepared well before you file. This level of visibility helps reduce errors and ensures you do not overlook potential deductions.

Uncertainty around refunds or tax bills is a common source of anxiety. Beem analyzes your income and spending patterns to help estimate what you may owe or receive before filing. Having a clearer picture ahead of time allows you to plan better, avoid last minute surprises, and make informed financial decisions during tax season.

Keeping financial documents scattered across emails, apps, and folders can slow down the filing process. Beem helps centralize your financial data, making it easier to locate important records when it is time to file. Organized information leads to faster filing and lowers the risk of missing key details that could delay processing or affect accuracy.

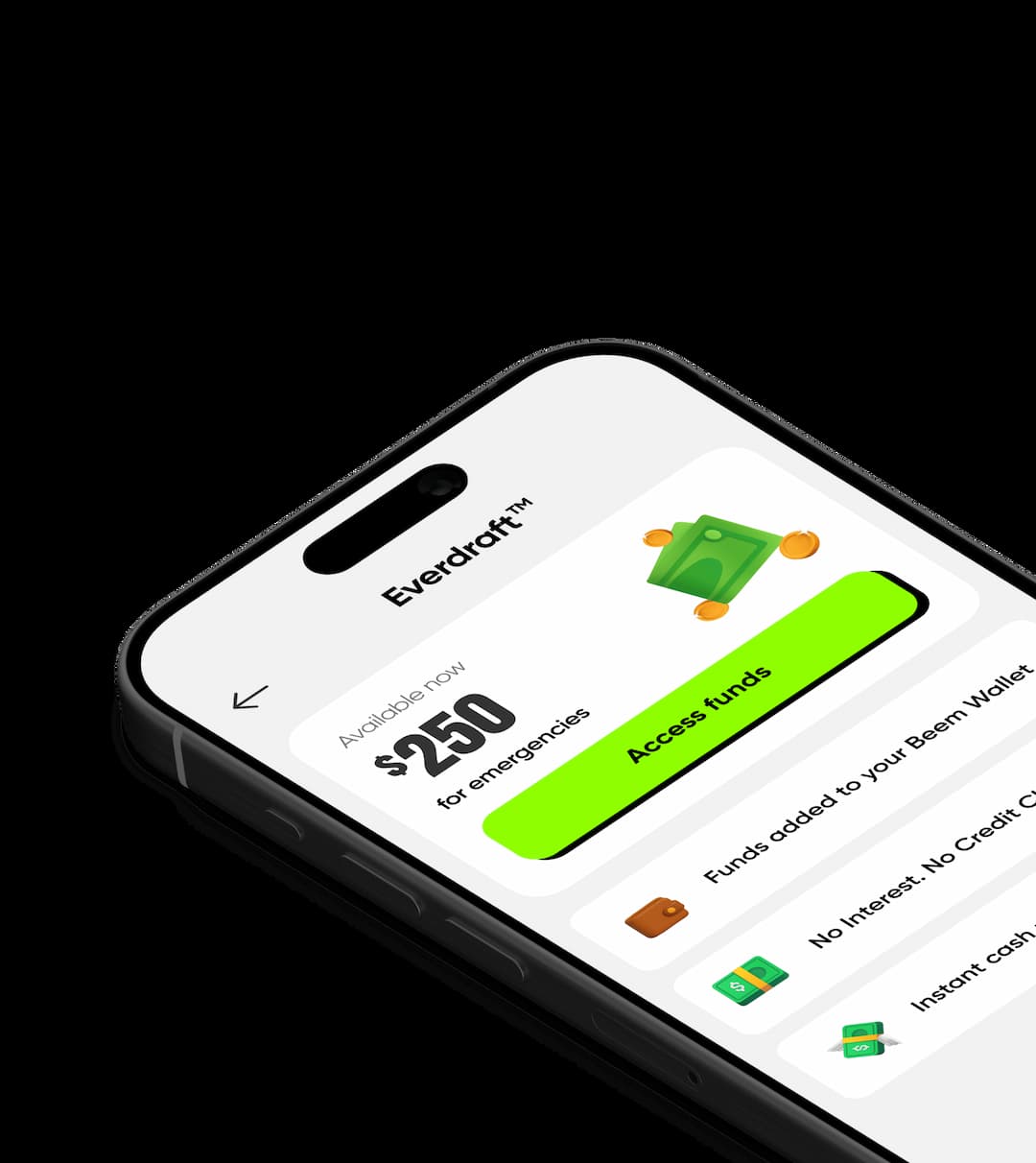

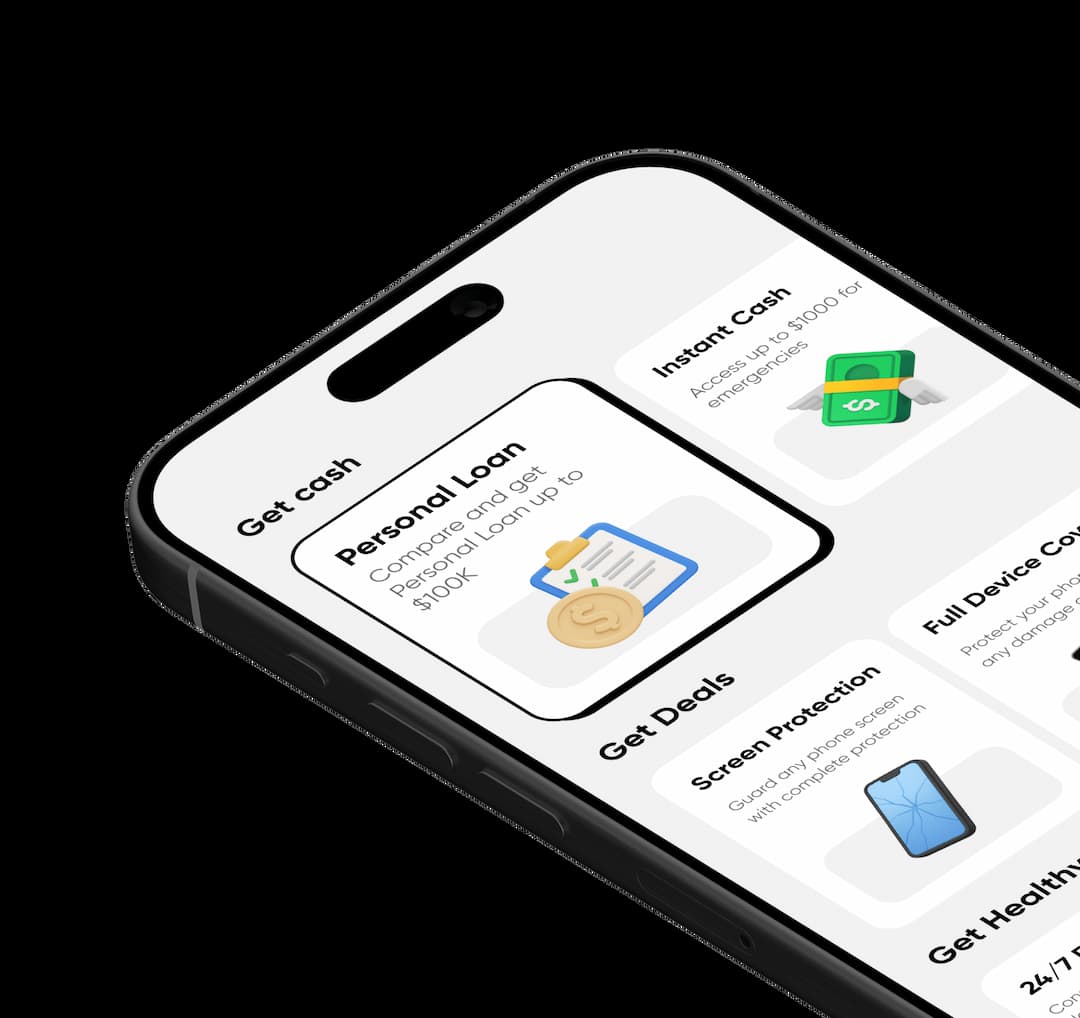

Tax season does not always align with cash flow. Whether you owe taxes, need to pay a tax preparer, or face unexpected expenses while waiting for your refund, Beem Everdraft™ can help. With Everdraft™, you can get up to $1,000 instantly when you need it most.

This instant cash access provides flexibility during tax season, helping you cover tax payments or related costs without disrupting your budget. Instead of stressing about short term cash gaps, Everdraft™ gives you breathing room to file on time and stay financially stable while managing your tax obligations.

Together, Beem's tracking tools, estimation features, and Everdraft™ cash access create a more manageable tax filing experience. By staying organized and having support when money is tight, you can approach tax season with greater confidence and less stress.

For the 2026 tax year, the IRS standard deduction amounts are higher due to inflation adjustments. These amounts reduce how much of your income is subject to federal income tax and depend on your filing status.

Here are the standard deduction amounts for tax year 2026:

- Single or Married Filing Separately: $16,100

- Married Filing Jointly or Qualifying Surviving Spouse: $32,200

- Head of Household: $24,150

If you are age 65 or older or legally blind, you may qualify for an additional standard deduction on top of these amounts.

Most taxpayers choose the standard deduction because it is higher and simpler than itemizing. However, if your eligible itemized deductions exceed these amounts, itemizing may still make sense.

The new tax regime in 2026 refers to the updated federal tax structure that applies to income earned during the 2026 tax year. While the U.S. tax system has not been completely overhauled, several inflation based adjustments, deduction changes, and reporting rules shape how taxpayers calculate and file their returns.

The goal of this regime is to simplify filing for most people while keeping the system aligned with economic changes.

Federal income tax brackets for 2026 have been adjusted upward to account for inflation. This means income thresholds for each tax rate are higher, allowing taxpayers to earn more before moving into a higher bracket. While tax rates themselves may stay the same, these adjusted limits can lower overall tax liability for many filers.

The standard deduction has increased again for 2026. This change benefits most taxpayers and continues the trend toward simpler filing. Because the standard deduction is higher, fewer people need to itemize deductions, which reduces paperwork and complexity.

Taxpayers can still choose between taking the standard deduction or itemizing deductions. Itemizing may make sense if deductible expenses such as mortgage interest, charitable contributions, or eligible medical expenses exceed the standard deduction amount. The option remains open so taxpayers can choose whichever method results in lower taxes.

Some itemized deductions remain limited under the 2026 tax regime. Caps on state and local tax deductions continue to apply, and certain miscellaneous deductions are still restricted. These limits make the standard deduction more appealing for many households.

The Child Tax Credit continues to be an important benefit for families. While income limits and credit amounts depend on current rules, this credit remains a major way families can reduce their tax bill directly.

The Earned Income Tax Credit remains available for low to moderate income workers. Income thresholds and credit amounts are adjusted for inflation, helping eligible taxpayers receive meaningful tax relief.

Education related credits and energy efficiency credits continue under the 2026 regime, offering tax savings for qualifying tuition expenses and approved home improvements.

The new tax regime places stronger emphasis on reporting digital assets. Any income, gains, or losses related to cryptocurrency transactions must be reported. This includes selling crypto, trading assets, or earning digital income. Accurate recordkeeping is essential to remain compliant.

Employees who rely primarily on W 2 income often benefit from the higher standard deduction and adjusted tax brackets.

Families may see meaningful tax savings through credits like the Child Tax Credit and Earned Income Tax Credit.

Self employed individuals still have access to business related deductions, though they must meet IRS requirements and maintain proper records.

The 2026 tax regime favors simplicity for most taxpayers. Higher standard deductions and adjusted brackets reduce the need for complex calculations. However, individuals with higher expenses, multiple income sources, or business income should still review itemizing options carefully.

Understanding how the new regime works helps you plan ahead, estimate taxes more accurately, and avoid surprises during filing season.

The new tax regime in 2026 is not a complete system overhaul, but it introduces important adjustments that affect how much tax you owe and how you file. With higher standard deductions, inflation adjusted brackets, continued credits, and stricter digital asset reporting, taxpayers who stay informed and organized will be best positioned to file accurately and confidently.

It is not guaranteed that tax refunds will universally be bigger in 2026, because refunds depend on individual circumstances rather than a single change in the tax code. However, several factors in the 2026 tax year could influence whether you receive a larger refund compared with prior years.

Because the standard deduction increases with inflation each year, many taxpayers will have a lower taxable income. If your taxable income goes down as a result, you could owe less tax and receive a larger refund, especially if your withholding or estimated payments remain the same.

Higher standard deductions simplify filing and can push more income into non taxable territory, which may increase refunds for people who take the standard deduction.

The IRS also adjusts tax brackets for inflation in 2026. When income thresholds rise, some taxpayers remain in lower tax brackets even if their earnings increase. This adjustment reduces your tax liability and can result in a bigger refund if withholding does not change proportionally.

Credits like the Child Tax Credit, Earned Income Tax Credit, and other refundable credits can directly increase your refund. If you qualify for more or larger credits based on income limits and dependent status, your refund may be higher than previous years.

Employers often update payroll withholding tables based on IRS guidance. If withholding is adjusted to reflect lower tax liability, your paychecks may increase throughout the year, which could reduce the size of your refund at filing because you’ve already kept more of your earnings during the year.

Your personal income and financial situation strongly influence refund size. If you earn more, have additional side income, or change filing status, these can affect your tax liability and refund independent of IRS adjustments.

If you make contributions to tax advantaged accounts, reduce withholding, or claim fewer deductions and credits, your refund might be smaller even if the baseline tax rules change.

To get a clearer idea of whether your refund might be bigger in 2026, consider:

- Reviewing your withholding early in the year to make sure it aligns with your goals

- Using updated tax rates, deductions, and credits for planning

- Tracking changes in income, dependents, and eligible credits

Tools that estimate tax liability and refunds based on real data can help you anticipate outcomes before filing.

Tax refunds in 2026 are not automatically larger for everyone, but many taxpayers may see higher refunds because of:

- Larger standard deductions

- Inflation adjusted tax brackets

- Expanded or refundable tax credits

How these factors affect your refund depends largely on your income, filing status, withholding, and eligibility for deductions and credits. Planning ahead and reviewing your tax situation during the year can help you make informed decisions and maximize your refund where possible.

The standard deadline to file federal taxes in 2026 is April 15. Extensions allow filing until October 15, but taxes owed must still be paid by April.

Yes. Electronic filing remains the most common and efficient way to file taxes and receive refunds faster.

Updates may include adjustments to the Child Tax Credit, inflation-related changes to deductions, and continued reporting requirements for digital assets.

Using financial tools that track income and expenses throughout the year can provide a more accurate refund estimate before filing.

Yes. Any taxable crypto transactions must be reported, including sales, trades, and income earned from digital assets.

Late filing can result in penalties and interest. Filing an extension helps avoid late-filing penalties, though payment deadlines still apply.

Most electronic refunds are issued within about three weeks, while paper returns take longer to process.

Only eligible self-employed individuals can deduct home office expenses if IRS criteria are met.

The IRS offers payment plans that allow you to pay over time while staying compliant.

Double-check information, file early, and keep organized records throughout the year.

Filing taxes in 2026 doesn't have to be overwhelming. With a clear understanding of current tax rules, proper preparation, and smart use of available tools, you can approach tax season with confidence.

Staying informed, organized, and proactive throughout the year makes filing smoother and helps you make better financial decisions long after your return is submitted. read more...

Estimate Your Refund Instantly

with Beem’s Free Calculator

Take the guesswork out of tax season. Get a clear estimate of your federal and state tax refund in minutes - all for free.

Do more with Beem

Fast personal loans, health program, & so much more!

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

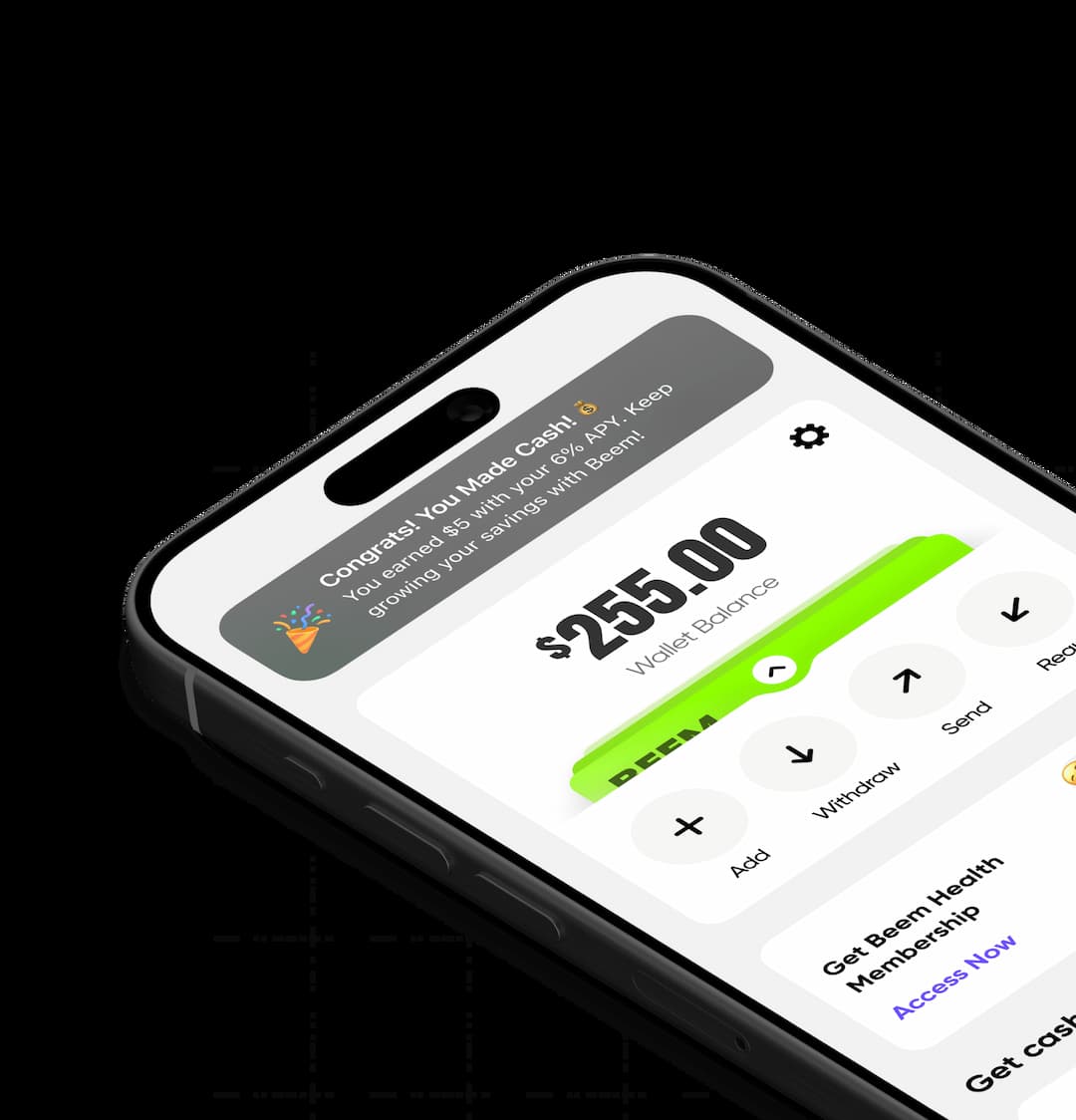

Get 5% APY on your savings account

Open a high-yield savings account & grow your money.

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

Get 5% APY on your savings account

Open a high-yield savings account & grow your money.

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

Get 5% APY on your savings account

Open a high-yield savings account & grow your money.