Earn up to 5%

APY on your

Savings Account

Get up to 5% APY. That’s 11x the national average* Put your money to work and watch it grow in a FDIC-Insured secure account.

Savings Interest Calculator

See how much interest

you could earn.

Savings shouldn't be a struggle

Grow your savings.

- Watch your money grow with high interest rate

It won't cost you a penny.

- No hidden or unnecessary fees.

Enjoy seamless experience

- Enjoy the seamless banking experience at your fingertips

Your savings are FDIC-insured.

- The funds in your account are insured up to $250,000.*

- Late fees

- Setup fees

- Hidden fees

- Annual fees

- Minimum balance fees

No fees. Period.

No fees. Period.

With Beem, I always know my money is going to successfully withdraw.

Renee S.

Secure and reliable I love that i can trust Beem with my financial needs always gets me funds when needed no stress about payback timing its peace of mind I really really need.

Breanna G.

Customer service rep Suresh Kashyap helped me fix an issue with multiple accounts by walking me through the required steps. About the app itself i liked the Everdraft option and the financial advice the app gave me.

Keri C.

I love use Beem app, it’s has variety of benefits not only just cash advance! I’m highly recommended for family and friends.

Amanda J.

They refer exclusively to other Beem offerings.

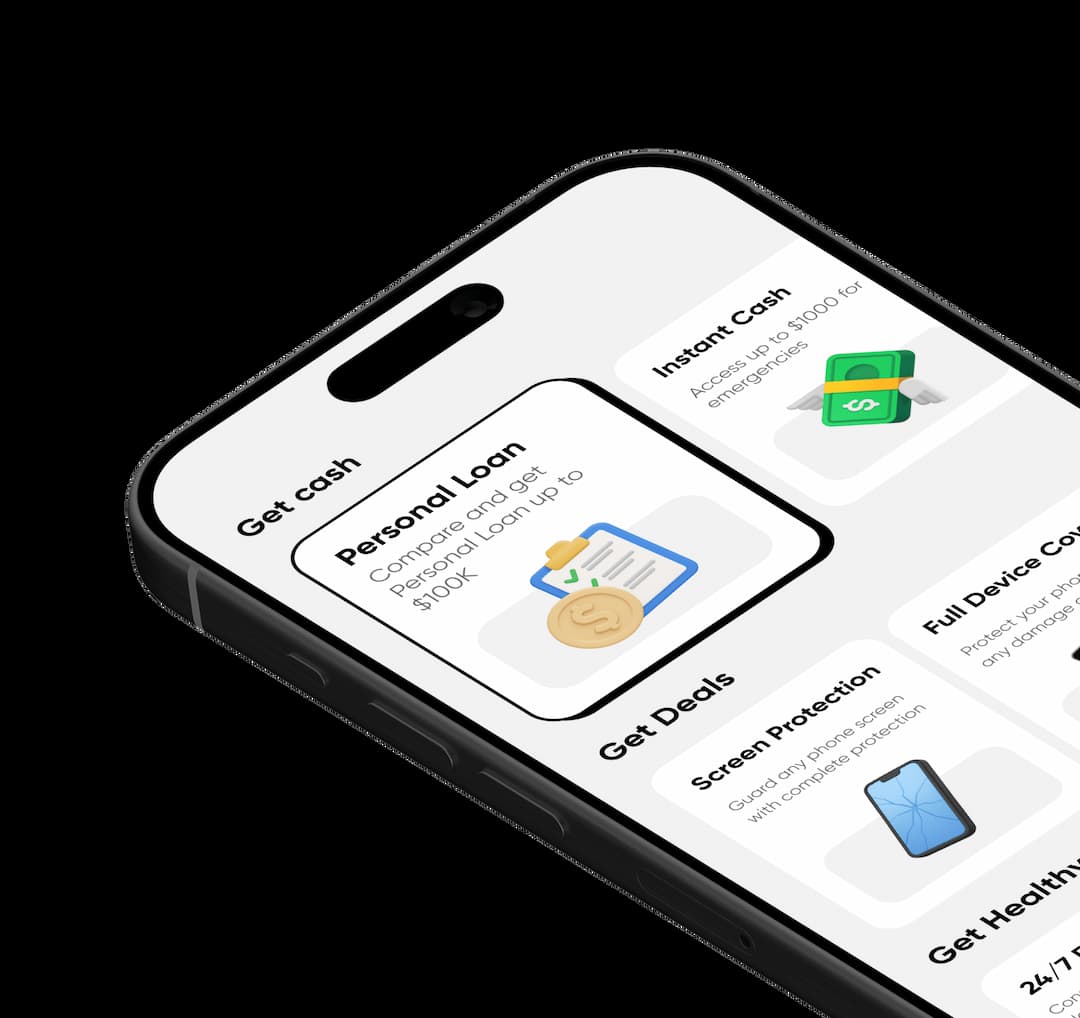

Do more with Beem

Fast personal loans, health program, & so much more!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

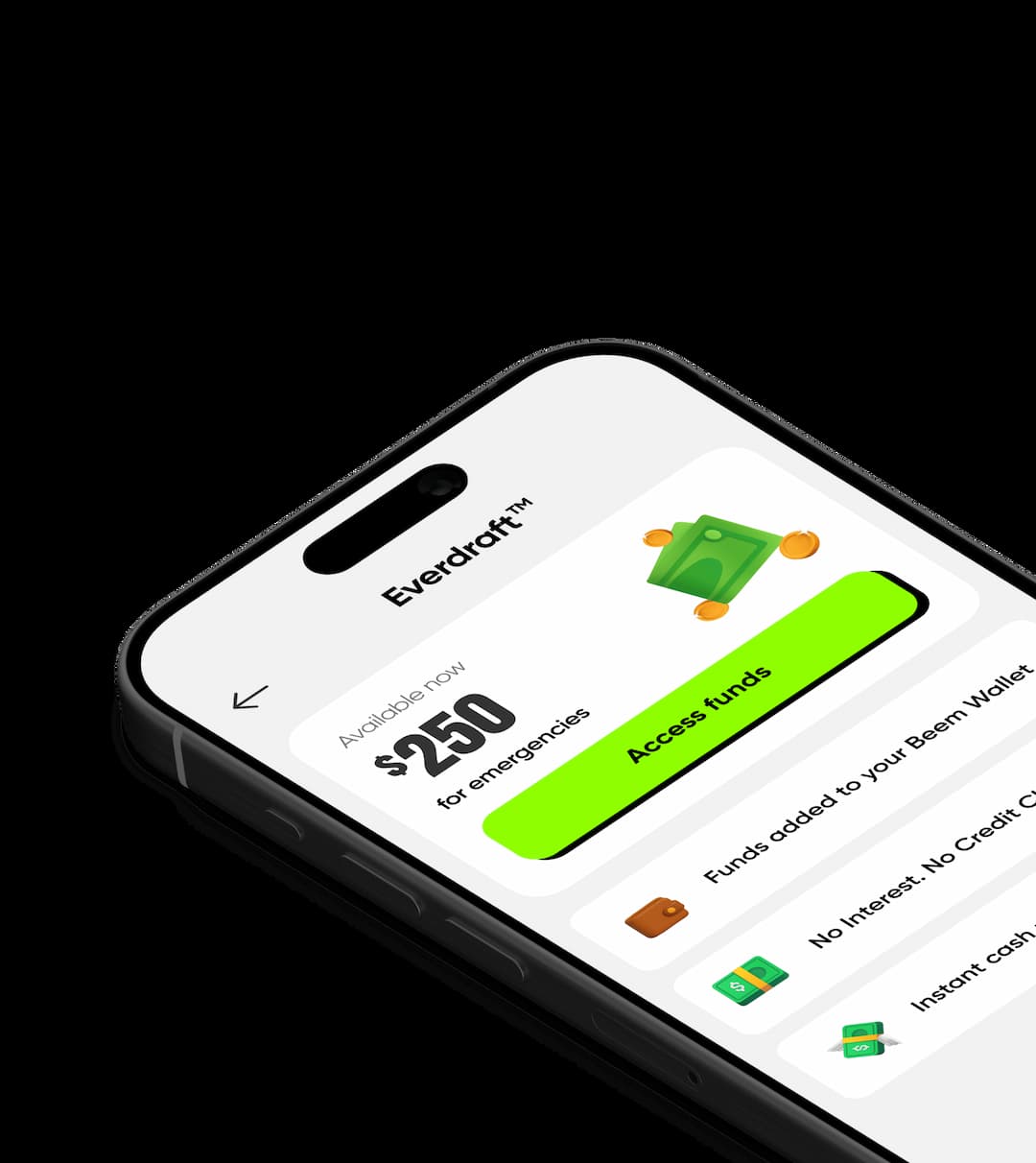

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

Save up to 40% on interest rates

Get personal loans up to $100k! Compare & find the best offers.

Get up to $1000 instant cash

Access future deposits for emergencies. No interest & no credit checks!

People Also Search For Beem

To open a High Yield Savings Account, you must share your identification and other relevant documents per the bank's requirements. The application process for HYSA is straightforward and can often be completed online.

You may need to provide the following documents:

- Valid government-issued ID (such as a driver's license or passport)

- Social Security Number (or Tax Identification Number)

- Address proof (like a utility bill or lease agreement)

Additionally, some banks may require documents to verify your identity and comply with regulatory requirements for a high-yield savings account. You can start the application process once you have gathered the necessary documents. Many banks offer a user-friendly online application process, allowing you to open a high-yield savings account from the comfort of your home.

Follow these simple steps to open your high-yield savings account.

- Research: Compare different banks and their account offerings.

- Gather Documents: Prepare your identification, Social Security number, and initial deposit.

- Choose an Account: Select the bank and account that aligns with your needs.

- Apply Online: Complete the application form on the bank's website.

- Fund the Account: Transfer your initial deposit to activate the account.

- Verify Information: Confirm your identity as required by regulations.

- Start Saving: Begin depositing funds and watching your savings grow.