You need a quick $100 to cover an unexpected bill. You pull up your phone, see both Beem and Dave as options, and then pause. Which one is actually safe to hand your bank account details to?

That hesitation is completely reasonable. Cash advance apps have grown fast over the past few years, and so have stories about surprise charges, aggressive auto-debits, and shady data practices. Not every app that promises a fee-free advance actually delivers one. Not every app that claims bank-level security actually has it.

This article is not a features comparison. You can find those anywhere. This is a focused safety review of both Beem and Dave in 2026, covering data security, financial risk, regulatory history, and user complaints.

By the end, you will know exactly which app is safer and why, so you can make a confident choice without second-guessing yourself.

What Does ‘Safe’ Actually Mean for a Cash Advance App?

Before we compare Beem and Dave head-to-head, it is worth being clear about what safety means in the context of a cash advance app.

Most people think of it as one thing, but it actually breaks down into four separate dimensions.

1. Data Security

This covers how the app encrypts your personal information, whether it shares or sells your data to third parties, and what happens to your information if you close your account.

A safe app uses strong encryption (at minimum 256-bit AES), has a clear and readable privacy policy, and does not monetize your personal data without your knowledge.

2. Financial Safety

This is the one most people underestimate. A cash advance app can be technically secure from a data standpoint but still put your finances at risk through hidden fees, mandatory tips that inflate the true borrowing cost, or aggressive auto-debit repayment clauses that can trigger an overdraft in your linked bank account.

3. Identity Safety

Every cash advance app requires you to verify your identity. The question is how much data they actually need and how they store it. Apps that request access to your contacts, microphone, or camera without a clear reason are a red flag.

4. Legitimacy and Regulation

Is the app backed by an FDIC-insured banking partner? Has it faced regulatory action from the Federal Trade Commission or Consumer Financial Protection Bureau? A legitimate app is transparent about its banking partners and has a clean or explainable regulatory record.

With those four dimensions in mind, here is how Beem and Dave each hold up.

Is Beem App Safe? A Detailed Look

Beem is a financial wellness app that offers cash advances through its InstaPay feature, along with tools for bill pay, credit building, and financial tracking. Here is what the safety picture looks like across each dimension.

Data Security and Privacy

Beem uses standard industry encryption to protect data in transit and at rest. The app does not explicitly advertise the specific encryption standard it uses on its public-facing pages, which is a minor transparency gap compared to some competitors.

That said, Beem’s privacy policy states that it does not sell your personal information to third parties for their own marketing purposes.

One thing to pay attention to: Beem’s privacy policy does allow it to share data with service providers and partners who help operate the platform.

This is standard for most fintech apps, but you should read the current policy on Beem’s official website before linking your primary bank account, since policies can update.

Fees and Financial Risk

Beem’s InstaPay feature charges a small fee per advance, which varies based on the advance amount and the speed of transfer. There is also a monthly subscription that unlocks higher advance limits and additional features.

The fees are disclosed before you confirm a transaction, which is a positive sign for transparency.

The financial risk to watch for with Beem is the repayment auto-debit. Like most cash advance apps, Beem automatically debits the advance amount from your linked account on the repayment date.

If your account balance is low on that date, you could face an overdraft from your bank, which adds bank fees on top of Beem’s own costs. Always ensure you have sufficient balance before your repayment date.

App Permissions

Beem requests access to your bank account through Plaid, a widely used and regulated financial data aggregator. It does not appear to request unnecessary device permissions such as your contacts or camera outside of specific feature uses. This is a good sign from a privacy hygiene standpoint.

Regulatory and Complaint History

As of early 2026, Beem has not faced any significant public regulatory action from the FTC or CFPB. The app has a moderate volume of user reviews on the Google Play Store and Apple App Store, with complaints centered primarily on advance limit sizes and customer service response times rather than safety or fraud concerns.

| Safety Rating | 4.7 / 5 |

| Best For | Users who want a multi-feature financial app with transparent fee disclosure |

| Watch Out For | Auto-debit repayments on low-balance days; read the repayment date carefully |

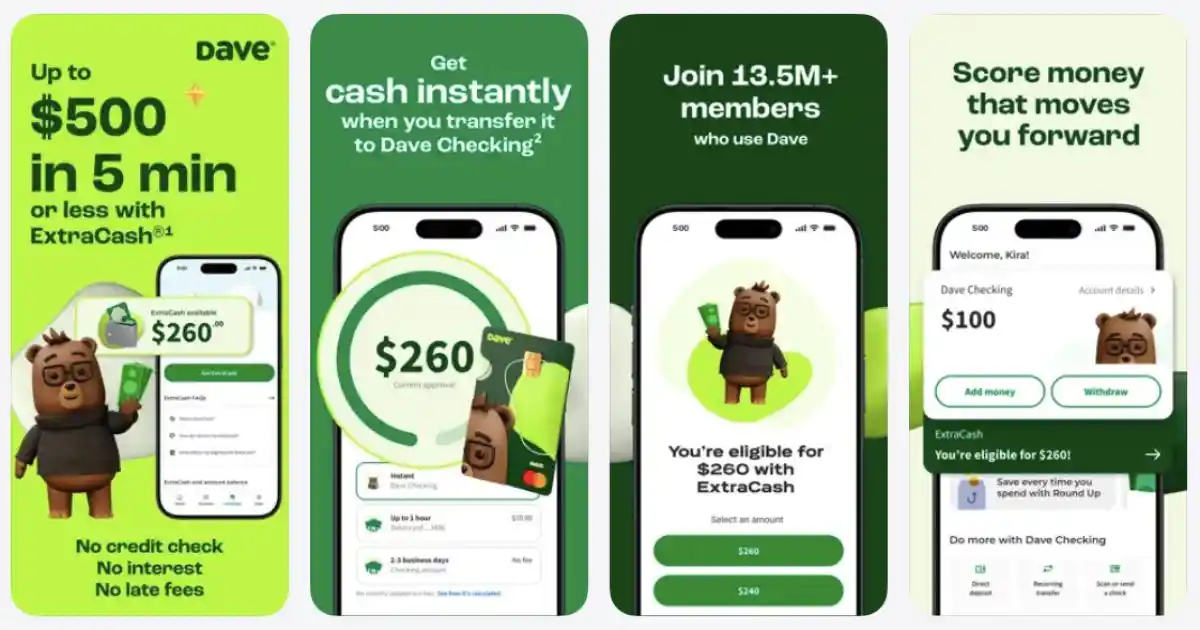

Is Dave App Safe? A Detailed Look

Dave is one of the most widely used cash advance apps in the United States, with tens of millions of registered users.

It offers ExtraCash advances of up to $500, a Dave Banking account (a demand deposit account), and a side hustle job board. Here is how Dave scores on safety.

Data Security and Privacy

Dave uses 256-bit AES encryption for data storage and TLS for data in transit, which meets the standard for financial applications. Dave Banking accounts are FDIC-insured up to $250,000 through Evolve Bank and Trust, which is a meaningful safety credential.

The FDIC backing means that if something were to go wrong with Dave’s banking partner, your deposited funds would be protected.

Dave’s privacy policy is detailed and publicly available. It does share data with third-party service providers, analytics vendors, and marketing partners. If you are concerned about data sharing with advertising networks, you should review the policy carefully and use the opt-out options Dave provides.

Fees and Financial Risk

Dave charges a $1 per month membership fee, which is among the lowest in the category. ExtraCash advances are technically free, but Dave strongly nudges users toward leaving a tip, and it also charges an express transfer fee if you want your advance in under an hour rather than the standard one to three business days.

The tips are optional, but the way they are presented in the app interface has drawn criticism from consumer advocates.

The financial risk model is similar to Beem. Dave auto-debits the advance amount from your linked account or Dave Banking account on the repayment date.

Users who link an external bank account should be particularly careful, since Dave’s repayment debit can arrive at an unexpected time relative to your paycheck schedule.

App Permissions

Dave uses Plaid to connect to external bank accounts. It does not request device permissions beyond what is needed to operate the app. The Dave Banking feature requires standard identity verification, including a government-issued ID and Social Security Number, which is normal for a banking product.

Regulatory and Complaint History

This is where Dave’s safety profile gets more complicated. In 2024, the FTC took action against Dave, alleging that the app misled consumers about the size of cash advances they could receive, made it difficult to cancel the monthly membership, and used tips as a disguised fee.

Dave settled the matter and made changes to its practices.

This regulatory history does not mean Dave is unsafe today, but it is a meaningful data point. It indicates that the FTC scrutinized Dave’s practices and found them problematic enough to pursue enforcement action.

Users should be aware of this history and read all disclosures carefully before signing up.

| Safety Rating | 3.5 / 5 |

| Best For | Users who want FDIC-insured banking combined with cash advances |

| Watch Out For | Optional tips presented in a way that encourages payment; FTC settlement history |

Beem vs Dave: Direct Safety Comparison

Here is how both apps compare across the key safety dimensions in one place.

| Safety Factor | Beem | Dave | Safer Choice |

| Data Encryption | Industry standard encryption | 256-bit AES + TLS | Tie |

| FDIC Insurance | Yes | Yes, via Evolve Bank and Trust | Tie |

| Hidden Fee Risk | Low (disclosed upfront) | Medium (tip nudge + express fee) | Beem |

| Third-Party Data Sharing | Yes, with service providers | Yes, including ad networks | Beem (narrower scope) |

| App Permissions | Standard (Plaid-based) | Standard (Plaid-based) | Tie |

| Regulatory Complaints | No major public actions | FTC settlement in 2024 | Beem |

| Membership Cost | $1.99/month | $1/month | Dave |

| Repayment Auto-Debit Risk | Yes (monitor your balance) | Yes (monitor your balance) | Tie |

Note: Always verify current fees and policies directly with Beem and Dave, as terms may have changed after this article was published.

Red Flags to Watch Out For in Any Cash Advance App

Whether you choose Beem, Dave, or a different app entirely, there are universal warning signs that every borrower should know before linking their bank account to any cash advance platform.

| Red Flags That Should Make You Pause |

| The app requests access to your contacts, microphone, or camera with no clear explanation for why those permissions are needed. |

| Fee disclosures only appear after you have already entered your bank credentials. Legitimate apps show you the cost before you commit. |

| The privacy policy uses vague language like ‘we may share your information with select partners’ without specifying who those partners are or what they do with your data. |

| The repayment terms are buried in fine print and the app does not send you a reminder before the auto-debit date. One unexpected debit can cascade into overdraft fees that cost more than the advance itself. |

| The advance amount you qualify for is significantly lower than what was advertised. This was a core issue in the FTC case against Dave and is a pattern worth watching for across the category. |

| There is no accessible customer support channel. If something goes wrong with your account and you cannot reach a human, you are exposed to prolonged financial risk. |

| The app has no clear process for disputing an incorrect charge or canceling your membership. Hidden cancellation barriers are a known dark pattern in subscription-based fintech apps. |

The best habit you can build before signing up for any cash advance app is to spend ten minutes reading its privacy policy and fee schedule. It is not the most exciting task, but it is the most protective one.

Which App Is Safer: Our Verdict

After reviewing both apps across data security, financial risk, app permissions, and regulatory history, Beem comes out as the safer choice for users whose primary concern is avoiding regulatory red flags and opaque fee structures.

Beem has not faced any significant public enforcement action, and its fees are disclosed clearly before you confirm a transaction. The tip-nudge dynamic that drew FTC scrutiny toward Dave is not a feature of Beem’s model in the same way.

That said, Dave is not an unsafe app. Its FDIC-insured banking product is a genuine safety advantage for users who want to keep their money in a protected account. And Dave’s $1 per month membership is significantly cheaper than Beem’s subscription tier, which matters if budget is a concern.

| How to Choose Based on Your Situation |

| Choose Beem if you value clean regulatory history and straightforward fee disclosure over all other factors. |

| Choose Dave if FDIC-insured banking is your top priority and you are comfortable monitoring for tip prompts and express transfer fees. |

| Avoid both if you are in chronic financial distress. Cash advance apps solve short-term gaps but do not fix structural budget problems. Consider a nonprofit credit counseling service if you find yourself relying on advances repeatedly. |

Final Thoughts

Beem and Dave are both real, functional cash advance apps that millions of people use without incident. But ‘safe enough for most people’ and ‘the safest choice for you’ are two different things, and this review exists to help you see the distinction clearly.

Beem wins on regulatory cleanliness and upfront fee disclosure. Dave wins on FDIC-insured banking and lower membership costs. Neither app is perfect, and both carry the same universal risk of auto-debit repayments catching your account at the wrong time.

If you are going to use either app, do three things before you sign up: read the current fee schedule, read at least the key sections of the privacy policy, and set a calendar reminder for your repayment date. Those three steps will protect you from 90% of the problems users report with cash advance apps.

| Quick Safety Checklist Before You Sign Up |

| Read the full fee schedule, not just the headline claim. |

| Check the privacy policy for data sharing and selling language. |

| Confirm whether the app is backed by an FDIC-insured banking partner. |

| Set a reminder for your repayment date and check your balance the day before. |

| Know how to cancel your membership before you sign up, not after. |

Stay informed, read the fine print, and use cash advance apps as the short-term tools they are designed to be.

Frequently Asked Questions

Is Beem a legitimate app?

Yes, Beem is a legitimate financial app. It is not a scam. The app operates as a licensed financial services provider and uses standard industry security practices. That said, like any financial app, you should read its privacy policy and fee disclosures before linking your bank account.

Is Dave app safe to link my bank account to?

Dave is generally safe to link your bank account to. It uses industry-standard encryption and connects to external accounts through Plaid, a regulated and widely used financial data service.

The main risks with Dave are financial rather than technical: the tip model, express transfer fees, and auto-debit repayments. Manage your balance carefully around your repayment date.

Does Beem sell your data?

According to Beem’s privacy policy, it does not sell your personal information to third parties for their own marketing purposes. It does share data with service providers who help operate the platform. You should check the current privacy policy on Beem’s official website for the most up-to-date information.

Has Dave had any security breaches?

Dave experienced a data breach in 2020 in which user information was exposed via a third-party service provider. Dave disclosed the breach and took corrective action. There have been no similarly significant public security incidents reported since then. The 2024 FTC action was about marketing practices and fee disclosure, not a data security breach.

Which cash advance app is safest in 2026?

Based on our analysis of regulatory history, fee transparency, data practices, and user complaints, Beem has a cleaner safety profile than Dave as of early 2026. However, the safest cash advance app is always the one you fully understand before using it. Read the terms, know your repayment date, and keep enough balance to cover the auto-debit.

Can Beem or Dave overdraft my account?

Neither Beem nor Dave directly overdrafts your account. However, both apps use auto-debit to collect repayments from your linked bank account.

If your balance is lower than the repayment amount on that date, your bank may process the debit and charge you an overdraft fee, or it may decline the debit and trigger a failed payment with the app. Either outcome creates additional costs and potential account issues. Always verify your balance a day or two before your scheduled repayment.

NOTE: This article is for informational purposes only and does not constitute financial advice.