Table of Contents

Disclaimer: This article is for informational purposes only and does not provide legal advice. It summarizes publicly available filings and government statements as of the “Updated on” date shown on this page. Allegations are not proof of wrongdoing, and the case may be pending, updated, or resolved after publication.

A lot of cash advance ads are built on two words: “up to.” Up to $500. Up to instant. Up to no fees. But when regulators file a case, the argument is usually that the typical experience didn’t match what the headline promised.

Cash advance apps exist for stressful moments, the week your account is tight, and you just need a small bridge to get through. That’s exactly why regulatory actions in this category matter. If you searched “Dave app FTC lawsuit” or “Dave lawsuit”, you’re probably trying to understand whether the concerns are about marketing, fees, tipping, subscriptions, or something else entirely, and whether it could affect you.

This article sticks to verifiable facts and primary-source documents. It explains what the Federal Trade Commission (FTC) and the U.S. Department of Justice (DOJ) have publicly alleged about Dave’s cash advance product, what Dave has said in response, and the consumer lessons that apply to any cash advance app. It is not legal advice.

Quick timeline of the Dave Cash Advance FTC Lawsuit

Here’s the simplest timeline, based on public filings and agency announcements:

- November 5, 2024: The FTC announced it filed a federal court complaint against Dave, alleging deceptive marketing around cash advances, undisclosed fees, and tip practices.

- December 30, 2024: The FTC announced it referred the case to the DOJ, and the DOJ filed an amended complaint adding Dave’s CEO, Jason Wilk, as a defendant and seeking civil penalties, consumer refunds, and an injunction.

- As of the FTC’s case page (last updated December 30, 2024), the case status is listed as pending.

This matters because many headlines make it sound like a settlement has already happened. The public FTC case listing describes it as pending, which means the allegations have not been adjudicated in court yet.

People Also Read: 5 Red Flags to Watch Out for in Cash Advance Apps

What the FTC and DOJ Allege in the Dave App Lawsuit

The FTC and DOJ allegations fall into a few buckets that are easy to understand if you translate them into real-life user experience: advertising claims, speed claims, fees, tips, charity messaging, and subscription cancellation.

1) “Up to $500” marketing, but many users allegedly did not see that amount

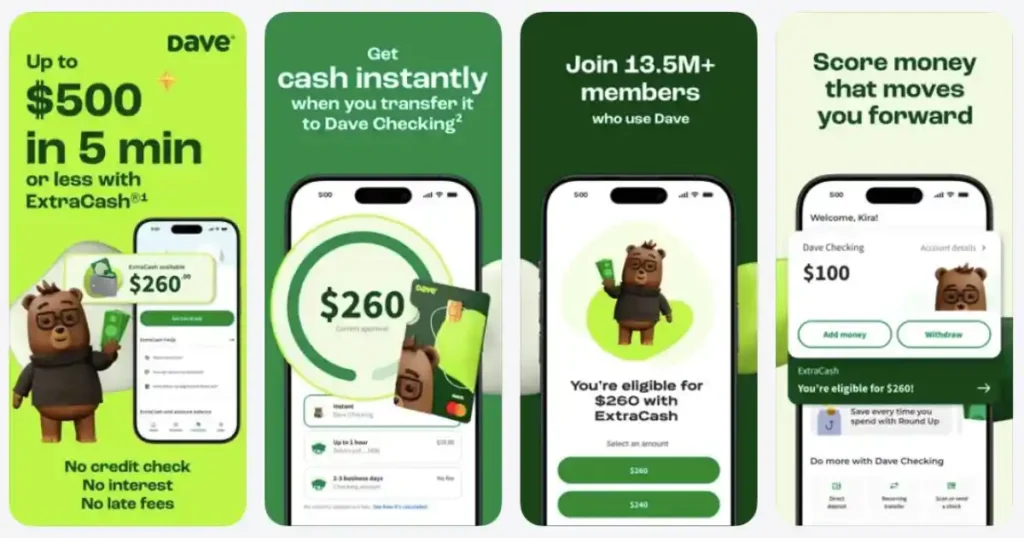

The FTC says Dave’s advertising was dominated by claims that consumers could receive “up to $500” and get it “instantly,” and alleges Dave offered the $500 amount only a tiny percentage of the time.

In the complaint, the FTC alleges that on average, more than 40% of new users were unable to obtain even a single offer of a cash advance in a calendar month, and among those who did get offers, only a very small fraction were for $500.

Consumer takeaway: “Up to” is not a promise. It’s a maximum that might apply to a small set of users under specific conditions. Any cash advance app that markets a large maximum should also communicate how rare that maximum is for typical users.

2) “Instant” advances allegedly required an express fee that was not clearly disclosed upfront

The FTC alleges that despite promising “instant” access, Dave required users to pay an “Express Fee” to receive advances instantly, and that this fee was not disclosed until after sign-up was complete and after the user had given Dave access to their bank account. The FTC described the express fee range as $3 to $25, and said users who did not pay had to wait two to three business days.

The amended complaint summary similarly alleges that users offered an advance had to pay an express fee of $3 to $25 to avoid waiting.

Consumer takeaway: “Instant” often means “instant if you pay.” The critical question is whether the app clearly discloses that cost before you link your bank and before you feel locked in.

3) Tip practices: alleged default tip charges and consent concerns

The FTC alleges that many consumers taking advances were charged an additional fee described as a “tip,” and that many consumers were unaware they were being charged or unaware there was any way to avoid the charge. The FTC described this “tip” as a surprise fee of 15% of the advance in many cases.

Consumer takeaway: A tip is only a tip if it is clearly optional and clearly avoidable. If the default experience nudges users into paying it, regulators may treat it as a fee in practice.

4) Charity-related messaging on tips: alleged mismatch between what users believed and what was donated

The FTC alleges users saw screens implying their tip selection would provide a certain number of “healthy meals” to children in need, but that Dave allegedly donated 10 cents per “percentage” selected and kept the remainder, and that this donation was not enough to provide the meals as represented.

The DOJ press release similarly alleges Dave’s app falsely represented it would purchase or pay for a certain number of meals based on the customer’s tip, while in reality it kept the vast majority and donated only a nominal sum.

Consumer takeaway: Any app tying charges to charitable impact must be extremely clear about how donations are calculated, how much is donated, and what “one meal” means in dollars. This is a recurring regulatory hot zone across industries, not just fintech.

5) Subscription “membership fee” and cancellation: alleged disclosure and “simple cancellation” issues

The FTC press release alleges Dave charged a $1 monthly membership fee debited directly from consumers’ bank accounts and failed to clearly and conspicuously disclose it, and also alleged that cancellation steps were not clear or easy to follow.

The DOJ press release alleges the defendants violated the Restore Online Shoppers’ Confidence Act (ROSCA) by enrolling customers in recurring monthly membership fees without clear disclosure of material terms and without providing a simple mechanism to cancel.

Consumer takeaway: Subscription mechanics can be as important as the cash advance itself. If you’re using any cash advance app, you should understand what is recurring, what is one-time, and how cancellation works before you link an account or request funds.

What Dave Has Said Publicly in Response

Dave has publicly disputed the allegations and said it intends to defend itself. In a company statement published via GlobeNewswire on December 31, 2024, Dave said the amended complaint was not a new lawsuit, called it government overreach, and said it believed the allegations included inaccuracies.

In that same statement, Dave said it had moved to a “simplified mandatory fee structure” that eliminates optional tips and express fees for its ExtraCash product, and said new members onboarded on or after December 4, 2024, were transitioned to the new structure, with existing members transitioning and full implementation by early 2025.

This is important context for consumers: regulators allege certain practices occurred, and the company says it changed aspects of its pricing experience. Those two things can both be true at the same time, and the court process is what determines whether the alleged conduct violated the law.

What This Means for Consumers who Used Dave

If you used Dave in the past, the most useful next step is not to panic. It’s a quick personal audit.

Start with your bank statements and identify four types of charges

The FTC allegations center on specific charge categories. Look back at your transaction history and try to identify:

- Membership fees (recurring)

- Express or instant transfer fees (delivery speed)

- Tips or tip-like charges

- Any other unexpected debits you don’t recognize

If you see charges you do not believe you authorized, document them with screenshots and dates. Then use the dispute and support channels that apply to you.

If you believe a charge was unauthorized, treat it as a banking and consumer-protection issue

In general, when you suspect unauthorized debits:

- Contact the merchant or app support to request clarification and resolution.

- Contact your bank to ask about dispute options and to stop future debits if needed.

- Consider reporting the issue to the FTC through its fraud and complaint portal if you believe it reflects deceptive practices.

This is not about “winning online.” It’s about creating a clean paper trail.

Understand what “pending” means in a lawsuit

Because the FTC case listing shows the matter as pending, there may not yet be a consumer refund process. Refund programs usually follow a settlement, judgment, or order that creates a distribution mechanism. For this case, the FTC and DOJ have said they seek consumer refunds and civil penalties, but that is not the same as “refunds are available now.”

A Simple Red Flag Checklist For Any Cash Advance App

The Dave app FTC lawsuit allegations highlight patterns that show up across the cash advance category. If you’re choosing any app in 2026, these are the risk points to pressure-test:

- The app advertises a large maximum, but does not clearly state how common that maximum is.

- “Instant” is marketed, but the fee to get instant delivery is not obvious until after you link your bank.

- Tips are presented as optional, but the user interface defaults to a high amount or makes it emotionally difficult to select a lower amount.

- The app charges a recurring membership fee, but you cannot clearly see it before enrollment or cancel easily.

- The app uses charitable messaging tied to charges, but donation math is unclear.

These are not “anti-fintech” rules. They are “don’t get surprised” rules.

People Also Read: Is Beem Legit

Where Beem Fits Into This Conversation

Beem’s position is simple: emergency cash should be transparent, understandable, and built for real-life timing gaps, not confusion.

Beem’s Everdraft™ page states that Everdraft™ is designed to help users access future deposits for emergencies, with no interest, no credit checks, and no income restrictions, and that users subscribe to a plan to unlock Everdraft™. It also states that the Beem app will automatically recover what was borrowed once a verified deposit hits.

Beem’s pricing page publicly lists plan prices and access tiers, and it separates membership cost from delivery speed costs by showing plan-based “starting at” instant debit card fees and also listing free standard ACH transfer timing.

The consumer-first takeaway is not “pick our app.” It’s this: choose a product where the economics are understandable before you commit. When pricing, speed, and subscription are clearly disclosed, you can make a real decision instead of a stressed one.

What the Dave lawsuit allegations mean in real life

| Allegation category (as described by FTC/DOJ) | What it can look like to a user | What to check | What to do next |

| “Up to $500” marketing vs typical eligibility | You sign up expecting $500, but see far smaller offers or none | Your offer history and actual advance amounts | Treat “up to” as a maximum, not an expectation; compare apps based on typical access, not ads |

| “Instant” requires fee | You select instant, then see an express fee late in the flow | Whether speed is free or paid, and when it’s disclosed | Use free standard delivery when possible; only pay for speed when the alternative is costlier |

| Tip charged or hard to avoid | Tip defaults high or is confusing to reduce | Tip line items and tip UI behavior | Look for apps where tips are clearly optional and easy to decline; dispute if you believe you didn’t consent |

| Charity messaging tied to tip | You believe your tip funds meals in a direct way | Donation disclosures vs what you believed you were funding | Avoid decision-making based on emotional screens; look for clear donation math and disclosures |

| Membership fees and cancellation | You notice a recurring fee and can’t easily stop it | Recurring debits and subscription settings | Cancel through the official channel for the platform you used and keep proof; ask your bank to block future debits if necessary |

Conclusion

The “Dave app FTC” story is bigger than one company. It’s about how cash advance apps should be judged: not by ads, not by maximum numbers, but by what a typical user experiences, what fees are disclosed and when, how consent is handled, and how easy it is to stop recurring charges.

The Dave lawsuit is still pending, according to the FTC’s case listing, and the allegations will ultimately be decided by the court. In the meantime, the consumer lesson is immediate: demand clarity up front, especially in products designed for people living paycheck to paycheck.

People Also Ask: Questions on Dave Cash Advance FTC Lawsuit

1. What is the Dave Cash Advance FTC lawsuit about?

The FTC lawsuit against Dave alleges the company used misleading marketing about the size and speed of its cash advances, charged fees that were not clearly disclosed upfront, and charged “tips” without valid consumer consent, along with allegations involving charitable-meals messaging and membership fee disclosure and cancellation. The case was referred to the DOJ, which filed an amended complaint adding CEO Jason Wilk and seeking consumer refunds, civil penalties, and an injunction.

2. Is the Dave lawsuit a criminal case?

Based on the FTC and DOJ announcements, this is a civil enforcement action, not a criminal prosecution. The agencies describe seeking civil penalties, consumer redress, and injunctive relief to stop alleged unlawful practices, and the court process determines the outcome.

3. Are refunds available right now for Dave users?

Public FTC and DOJ communications state that the government is seeking consumer refunds, but the FTC’s case page lists the matter as pending and does not describe an active refund program for this specific case. Refund processes typically require a settlement or court order that establishes how refunds will be distributed.

4. What did Dave say about the FTC allegations?

Dave has said it believes the government’s allegations include inaccuracies, characterized the amended complaint as government overreach, and stated it intends to defend itself. Dave also said it moved to a simplified mandatory fee structure that eliminates optional tips and express fees for its ExtraCash product, with a transition beginning for new members in December 2024 and full implementation in early 2025.

5. How can I protect myself when using any cash advance app in 2026?

Use a simple rule: understand the total cost before you connect your bank or take money. That means reading the membership fee terms, knowing whether “instant” requires a fee, checking whether tips are truly optional and easy to decline, and confirming cancellation steps. If something looks off, document it, contact support, and use your bank’s dispute channels when appropriate.