Table of Contents

When people search “Beem bank,” they are usually trying to answer one question: Where is my money actually held, and what protections apply?

That is a smart question. In fintech, the app you use and the regulated institution behind the scenes are not always the same entity. We think the infrastructure should be clear, not hidden. So here is the direct answer:

Beem is a financial technology company, not a bank. Banking services, including the deposit account, are provided by Cross River Bank, Member FDIC.

This blog explains what that means in real life: which parts of Beem are provided by a bank partner, how FDIC insurance works in this setup, what Upwardli does, and how to verify it yourself in under two minutes.

The Simple Answer To “What Bank Does Beem Use?”

When you see “beem bank” in search, you are really asking: Which FDIC-insured bank is behind the deposit account? On Beem pages that describe our deposit infrastructure, we disclose the partner bank clearly:

- Cross River Bank, Member FDIC, provides the banking services (including the demand deposit account).

- Beem’s direct deposit product is FDIC-insured up to $250,000 through Cross River Bank (subject to FDIC rules).

So if you want a crisp phrase for your mental model: Beem is the app and experience. Cross River Bank is the FDIC-insured bank behind the deposit account.

Why Fintech Infrastructure Looks Different Than Traditional Banking

Traditional banking is a single-brand relationship. You open an account at a bank, the bank runs the app, and the bank holds the deposits.

Modern fintech often uses a partner-bank model. The app is built by a fintech company (us), while certain regulated banking components are provided by an FDIC-insured bank (Cross River Bank). This structure can be powerful because it combines a modern user experience with regulated banking rails and protections.

It also creates confusion if companies are vague. We do not believe in vagueness here. That is why we say it plainly: Beem is not a bank and Cross River Bank provides the deposit account.

People Also Read: How BEEM Protects Against Fraud

What “Member FDIC” Means In The Beem Bank Conversation

FDIC insurance is one of the most important consumer protections in U.S. banking, but it only applies in the right context. When we say Cross River Bank is “Member FDIC,” it means Cross River Bank is an FDIC-insured institution. You can verify Cross River Bank’s insured status directly using the FDIC’s BankFind Suite.

The Key Clarity: FDIC Applies To Deposit Products, Not Everything

FDIC insurance generally applies to eligible deposit products held at an FDIC-insured bank, within standard limits and ownership rules. On Beem pages, we separate deposit products from non-deposit products explicitly:

- Deposit product is provided by Cross River Bank, Member FDIC and is FDIC-insured up to $250,000 through Cross River Bank.

- Line of credit is not a deposit product.

That separation matters because it’s how you keep the “beem bank” question honest. You always want to know: Is this a deposit product at an FDIC-insured bank, or something else?

Where Upwardli Fits In The Beem Infrastructure

If you have seen Upwardli mentioned alongside Beem, here is the clear explanation we publish on our own pages: Upwardli is the program manager of the Beem Card and is not an FDIC-insured bank.

Program manager is a common role in card programs. It means Upwardli helps operate the program layer, while the underlying banking services and deposit account are provided by the FDIC-insured bank partner (Cross River Bank). Also disclosed on our pages: The Beem Card may be used everywhere Mastercard is accepted.

The Beem Infrastructure, Broken Into Simple Layers

When people ask “what bank does Beem use,” they usually want a mental map. Here is ours.

Layer 1: The Beem App Experience

Beem is the app layer: the interface, feature discovery, and the “financial hub” experience. It’s where you interact with tools like Everdraft™ (instant cash advance feature) and other Beem products.

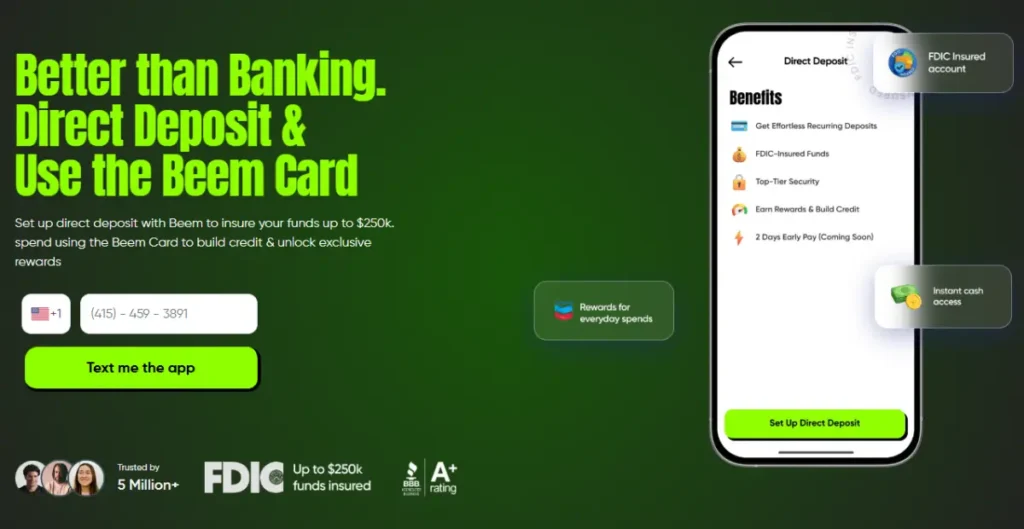

Layer 2: Regulated Banking Services

For banking services and deposit accounts, we rely on our regulated partner:

- Cross River Bank provides banking services including the demand deposit account, and deposits are FDIC-insured up to $250,000 through Cross River Bank.

Layer 3: Card Program Operations

For the Beem Card program structure:

- Upwardli is the program manager (not an FDIC-insured bank).

- The Beem Card is usable wherever Mastercard is accepted.

Layer 4: Security Controls That Protect Access

On our security page, we explain the standards and controls we lean on:

- Security based on frameworks such as NIST CSF, PCI-DSS, and SOC 2, with up-to-date certifications by third-party auditors.

- Biometric login support (Face ID / Touch ID) for added safety.

People Also Read: How FDIC Insurance Works

How To Verify “Beem Bank” Yourself In Two Minutes

You do not need to trust a blog post. You can verify the infrastructure quickly.

Step 1: Check Our Disclosure On Beem Pages

Our Direct Deposit and Credit Builder Card pages state:

- Banking services, including the demand deposit account, are provided by Cross River Bank, Member FDIC.

- Deposits are FDIC-insured up to $250,000 through Cross River Bank.

- Upwardli is program manager of the Beem Card and not an FDIC-insured bank.

- Line of credit is not a deposit product.

Step 2: Verify Cross River Bank In FDIC BankFind

Use the FDIC’s BankFind Suite to confirm the institution is FDIC-insured. Cross River Bank appears in the FDIC database (example: details page for Cross River Bank). That is the cleanest way to validate “beem bank” without relying on marketing.

What This Infrastructure Means For You As A Beem User

1) Your Deposit Account Is Backed By A Regulated Bank Partner

Because the deposit account is provided by Cross River Bank, the deposit product is eligible for FDIC insurance up to the stated limits and conditions described on our pages.

2) Clarity On What Is And Is Not A Deposit Product

We explicitly state that a line of credit is not a deposit product. That protects users from confusing “FDIC-insured deposits” with every financial feature in an app.

3) A More Modern App Layer, With Bank-Backed Deposit Infrastructure

This is the point of the model: you get a modern product experience while deposit accounts are provided by an FDIC-insured bank.

How To Understand Beem Bank

| What You’re Using In Beem | Who Provides The Underlying Infrastructure | What You Should Know |

| Deposit account / banking services | Cross River Bank, Member FDIC | Deposit product is FDIC-insured up to $250,000 through Cross River Bank (subject to FDIC rules). |

| Beem Card program layer | Upwardli (program manager) | Upwardli is not an FDIC-insured bank; the card is usable wherever Mastercard is accepted. |

| “FDIC insurance” claims | FDIC applies to deposit products held at FDIC-insured banks | You can verify Cross River Bank in FDIC BankFind Suite. |

| Beem security posture | Beem security program | Security based on NIST CSF, PCI-DSS, SOC 2; biometric login supported. |

| Line of credit mention (if shown) | Cross River Bank (as disclosed) | Line of credit is not a deposit product (so FDIC deposit insurance does not apply to it as a “deposit”). |

How FDIC Coverage Works When You Use Multiple Apps

One FDIC detail matters a lot for fintech users, and most people only learn it after they have already opened multiple accounts.

FDIC insurance is generally $250,000 per depositor, per FDIC-insured bank, per ownership category, not “$250,000 per app.”

Why that matters in the beem bank conversation: if you have multiple deposit accounts that are ultimately provided through the same FDIC-insured bank, those balances can be added together for insurance purposes within the same ownership category.

We disclose that our deposit product is provided through Cross River Bank, Member FDIC, and FDIC-insured up to $250,000 through Cross River Bank. So the practical takeaway is simple:

- If Beem is your only deposit relationship with that bank, the rule is straightforward.

- If you also use other products that rely on the same partner bank, you should understand aggregation and ownership categories so your insurance expectations stay accurate.

People Also Read: How Cash Advance Apps Protect Your Banking Data

What Happens If The Partner Bank Fails

People ask “what bank does Beem use” partly because they want to understand worst-case protection, not just day-to-day infrastructure.

FDIC insurance is designed for a specific scenario: an FDIC-insured bank fails. In that situation, the FDIC’s role is to protect insured deposits up to the coverage limits, typically by making insured funds available through an acquiring bank or by paying depositors.

Since our deposit product is provided by Cross River Bank, Member FDIC, the FDIC framework is the protection layer behind deposit funds, within FDIC rules and limits.

This segment adds value because it clarifies what “Member FDIC” is actually for: it’s not a marketing badge, it’s a bank-failure protection system with defined limits.

Why We Spell Out “Line Of Credit Is Not A Deposit Product”

If you skim fintech pages quickly, it’s easy to assume FDIC covers “everything in the app.” That is not how FDIC works, and we do not want users to be confused about it.

On our disclosure, we explicitly separate deposit products from non-deposit products and state: “Line of credit is not a deposit product.”

Here is the reason that sentence matters: FDIC insurance applies to eligible deposit products held at FDIC-insured banks within coverage limits and ownership rules. A line of credit is not a deposit account, so it should not be framed as FDIC-insured “deposit coverage.”

This is a trust move. Clear separation prevents users from assuming protections that are not designed for that product type.

Who Is Responsible For What In The Infrastructure

Fintech infrastructure can feel confusing because multiple entities can be involved, and customers deserve clarity on who does what.

Here is the clean way to think about it using our own disclosures:

- Beem: We build the app experience and communicate how the products work. We also publish our security posture and standards on our security page.

- Cross River Bank, Member FDIC: provides the banking services including the demand deposit account, and the deposit product is FDIC-insured up to $250,000 through Cross River Bank (subject to FDIC rules).

- Upwardli: program manager for the Beem Card, and we disclose Upwardli is not an FDIC-insured bank.

Why this matters for users: When you understand the roles, it becomes easier to understand disclosures, protections, and where “bank-level” rules apply versus where the app layer applies.

Conclusion

The “beem bank” question is really about transparency. You deserve to know where the deposit account lives, who regulates it, and what protections apply.

Here is the clean infrastructure summary: The Beem app is a fintech platform. Cross River Bank, Member FDIC, provides the banking services and direct deposit account, and deposits are FDIC-insured up to $250,000 through Cross River Bank (subject to FDIC rules). Upwardli is the program manager for the Beem Card and is not an FDIC-insured bank.

If you want to double-check it yourself, you can. That is how we believe trust should work in fintech: clear disclosure, verifiable facts, and infrastructure that is easy to understand.

People Also Ask

1. Is Beem A Bank?

No. Beem is a financial technology company, not a bank. That means we build the app experience and the financial tools you use, while regulated banking services (including the demand deposit account) are provided through our partner bank, Cross River Bank, Member FDIC. This structure is common in fintech because it combines a modern app layer with bank-backed infrastructure and protections.

2. What Bank Does Beem Use?

For banking services and the deposit account infrastructure, Beem uses Cross River Bank, Member FDIC, as the partner bank that provides the demand deposit account. If you’re searching “beem bank,” this is the most direct answer: your deposit account is bank-backed through Cross River Bank.

3. Is My Money FDIC Insured With Beem?

Yes, it is FDIC-insured up to $250,000 through Cross River Bank, subject to standard FDIC rules and limits (like per depositor, per bank, per ownership category). It’s important to understand that FDIC coverage applies to eligible deposit products held at the FDIC-insured bank, not to every financial feature inside an app.

4. What Is Upwardli’s Role?

Upwardli is the program manager for the Beem Card program. That means Upwardli supports the card program operations layer, but it is not an FDIC-insured bank. The deposit account and banking services are still provided through the FDIC-insured bank partner, as disclosed on our pages.

5. How Can I Verify The Beem Bank Information?

You can verify it in two quick ways: Check our disclosures on Beem pages, where we state Cross River Bank is the provider of the deposit account and describe FDIC coverage. Independently confirm Cross River Bank’s FDIC-insured status using the FDIC’s BankFind Suite.