Table of Contents

Most tip-based cash advance apps are not truly free for users. While they charge no stated interest, the combination of voluntary tips, express delivery fees, and monthly subscriptions creates a real annual cost that is rarely disclosed upfront. A user who tips $3 per advance and pays for instant delivery twice a month spends over $140 per year on a product marketed as free. Genuinely free alternatives, like Beem Everdraft™, charge no tips, no delivery fees, and no subscription.

Picture this: you are three days from payday, your account balance is $12, and an unexpected bill just landed in your inbox. You find a cash advance app with “free” in its description, get approved in minutes, and then comes the tip screen. A $4 amount is already selected. You are in a hurry, the confirm button is right there, and $4 feels reasonable for a service that just helped you out. You tap confirm.

What you did not realize is that this moment, repeated across every advance you take this year, will quietly cost you more than most people pay for a streaming subscription. This blog pulls back the curtain on how tip-based apps actually make money, what it costs real users over time, and what genuine transparency looks like.

What Does “Tip-Based” Actually Mean in a Cash Advance App?

A tip-based cash advance app asks users to leave a voluntary monetary contribution each time they request an advance. The app presents this tip as optional and frames it as a way to support the platform or keep the service accessible to everyone. No tip amount is required to complete the transaction, at least in theory.

In practice, tip-based pricing is a deliberate revenue model, not an act of goodwill on the app’s part. The platform sets a default tip amount, designs the interface to make accepting that default easier than removing it, and uses social or emotional framing to make users feel that leaving a tip is the right thing to do. The result is a pricing structure that functions economically like a fee but is structured legally to avoid being classified as one.

How Tip Prompts Are Designed to Cost You Money

The mechanics of tip prompts in cash advance apps are worth examining closely because the design choices are not accidental. They are engineered to maximize tip acceptance while maintaining the appearance of user choice.

Pre-Selected Default Amounts

When you reach the tip screen in most cash advance apps, a tip amount is already selected for you. It is rarely zero. The default is typically between $1 and $5 for smaller advances, and some apps default to a percentage of the advance amount for larger requests. Users who do not actively notice and change the pre-selected amount accept the default without making a conscious choice to tip.

Asymmetric Interface Design

The button to accept the suggested tip is almost always the most prominent element on the screen. It is large, brightly colored, and positioned as the natural next step in the flow. The option to reduce or remove the tip is smaller, less prominent, and in some apps requires tapping through to a secondary screen. This design asymmetry, known as a dark pattern in UX design, steers users toward the choice that benefits the company rather than the one that serves the user.

Emotional and Social Framing

Many tip prompts include copy that frames leaving a tip as an act of community support. Phrases like “help keep this service free for everyone” or “support our mission” attach a social cost to removing the tip. Users who would otherwise skip it may feel that doing so is selfish or harmful to other users. This framing is not technically dishonest, but it introduces an emotional variable into what should be a neutral financial decision.

Per-Transaction Frequency

Unlike a subscription fee that you pay once regardless of usage, tip prompts appear on every single advance request. This means the more you rely on the app, the more you pay. For the users who need cash advances most frequently, the tip model extracts the most money, which is the inverse of how a genuinely supportive financial product should work.

Breaking Down the Real Annual Cost

The true cost of a tip-based cash advance app only becomes visible when you calculate across a full year of typical usage. Here is what that looks like across three realistic user profiles.

The Occasional User

This user takes one advance per month, accepts the $3 default tip, and pays a $3.99 express delivery fee to get funds the same day. Monthly cost: $6.99. Annual cost: $83.88. On a typical $150 advance, this represents an effective annual cost rate that would never appear in any advertised figure but is very real in the user’s bank account.

The Regular User

This user takes two advances per month, accepts the default tip, pays for express delivery each time, and subscribes to the app’s premium tier at $9.99 per month to access higher advance amounts. Monthly cost: $23.97. Annual cost: $287.64. This user almost certainly downloaded the app believing it was free.

The Dependent User

This user takes three or more advances per month, tips on each one, pays for instant delivery every time, and maintains a premium subscription. Their annual cost can exceed $400, making their “free” cash advance app one of their more significant recurring financial expenses, and one that almost certainly was never budgeted for.

People Also Read: Cash Advance Apps With Flexible Repayment Options in 2026

The Express Delivery Fee: The Most Overlooked Hidden Cost

If tip prompts are the most discussed hidden cost in cash advance apps, express delivery fees are the most consistently overlooked. And for many users, they represent a larger annual expense than tips do.

The standard delivery option offered by most cash advance apps takes two to three business days. For a product that exists to solve urgent financial problems, two to three days is often useless. If you need money to cover an overdraft today, fill your gas tank before work tomorrow, or pay a bill before a late fee kicks in, standard delivery won’t solve your problem.

Express delivery, which costs between $2.99 and $7.99 depending on the app and the advance amount, is the only option that actually serves the purpose.

This means that, for most users in most genuine cash advance situations, the express delivery fee is not optional. It is a mandatory cost of using the product for its intended purpose, dressed up as a convenience upgrade.

Why “No Interest” Is Not the Same as “No Cost”

The marketing around cash advance apps leans heavily on the absence of interest. This is technically accurate and genuinely meaningful. Cash advances are not loans in the traditional sense, and not charging interest distinguishes them meaningfully from payday lenders and high-rate credit products.

But the absence of interest does not mean the absence of cost. It means the cost is structured differently. When a user pays $3 in tips, $4.99 in express fees, and $9.99 in subscription charges in a single month for a $200 advance, the total cost of that advance is $17.98, an effective rate that would be considered extremely high if it appeared in an APR disclosure. It never appears that way because each component is framed as something other than interest.

The consumer finance principle to apply here is simple: the total cost of a financial product is the sum of everything you pay to use it, regardless of what each component is called. Tips are a cost. Express fees are a cost. Subscription charges are a cost. When you add them together, the true price of a tip-based cash advance app becomes clear.

What Genuine Transparency Looks Like in a Cash Advance App

A genuinely transparent cash advance app clearly communicates its full cost structure, charges nothing beyond what it explicitly discloses, and does not use interface design or emotional framing to generate revenue through user inertia.

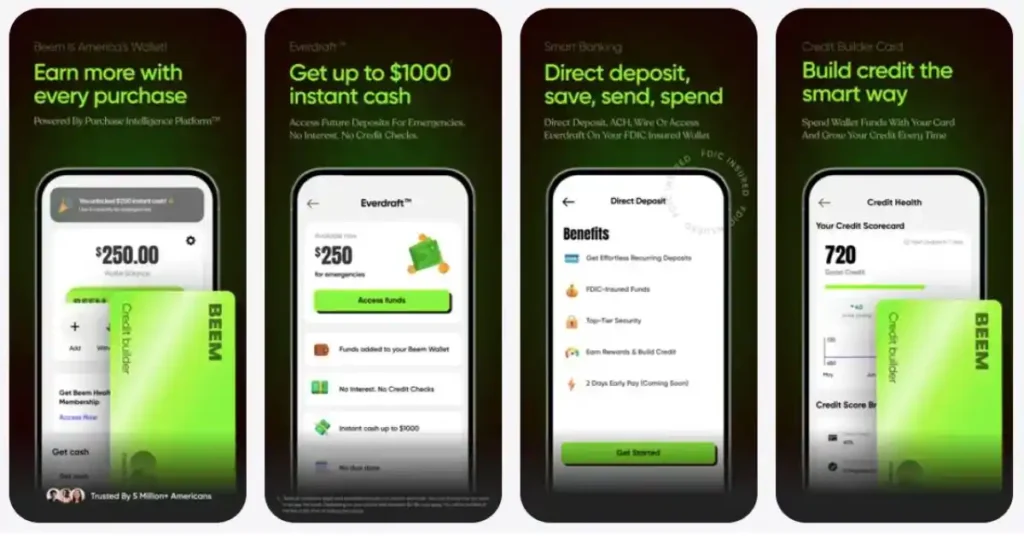

Beem Everdraft straightforwardly meets this standard. There are no tips, no express delivery fees, and no subscription paywall. The total cost of borrowing through Everdraft is zero beyond the amount you borrow, and that is disclosed clearly before you ever connect your bank account.

This approach is possible because Beem’s revenue model is built around its broader financial services platform rather than on extraction from the cash advance product itself. BudgetGPT, smart money transfers, credit-building tools, personal loans, and other Beem services create a sustainable business without relying on the cash advance feature to generate revenue through opaque pricing.

When a platform does not need to extract tips, delivery fees, or subscription fees to stay profitable, it can design the product around your actual financial needs rather than maximizing what you pay per transaction. That alignment of incentives is what genuine transparency looks like in practice.

How to Audit Any Cash Advance App Before You Download It

Before you connect your bank account to a cash advance app, these five questions will tell you most of what you need to know about its true cost.

What is the default tip amount, and how easy is it to set it to zero? Open a review of the app’s tip screen before downloading. If reviews mention difficulty removing the tip or a high default amount, treat that as a meaningful signal about how the app is designed to interact with your money.

Is instant or same-day delivery free, or does it cost extra? For any genuine cash advance use case, you need funds quickly. If the app charges a fast-delivery fee, add that fee to every advance you take when calculating your true annual cost.

Is there a monthly or annual subscription fee? If so, calculate what you would pay over 12 months, including months when you do not take an advance. A $9.99 monthly subscription represents $119.88 per year, whether you borrow once or twenty times.

What is the maximum advance amount without a subscription? Some apps advertise high limits but restrict them to premium subscribers. Understand what you can actually access on the free tier before deciding if the app meets your needs.

Is the platform FDIC-backed? FDIC backing for eligible deposit accounts is a meaningful indicator of financial credibility and stability. It is one of the clearest signals that a platform is operating with the financial seriousness required to handle your money.

People Also Read: Variable Fee Cash Advance Apps Explained: Real Costs and Hidden Charges

The Bottom Line

The cash advance category has a language problem. Products that generate hundreds of dollars in annual revenue per user through tips, delivery fees, and subscriptions describe themselves as free because they do not charge interest. That description is technically defensible and practically misleading.

Real transparency in a financial product means the cost you pay is the cost you were told about. It means the interface is designed to serve you, not to steer you toward choices that benefit the platform. It means that when a company says its product is free, the word carries its full meaning, not just a narrow technical one.

Beem Everdraft is free in the complete sense. No tips. No delivery fees. No subscription. No interest. Up to $1,000 based on your financial behavior, delivered instantly, at a total additional cost of zero. Download the app now!

When you are already managing a tight budget, that is not just a better deal. It is a fundamentally different kind of product, one built on the belief that people navigating financial challenges deserve tools that are honest about what they cost.

People Also Ask

1. Are tips on cash advance apps really voluntary?

Tips are technically voluntary on most cash advance apps. Still, pre-selected default amounts and an interface design that makes removing the tip unintuitive mean many users end up paying them without making a conscious choice. Over a full year of regular use, these tips can add up to $36-$100 or more.

2. What is the true annual cost of a tip-based cash advance app?

The true annual cost depends on usage frequency and which optional charges you accept. A user who takes two advances per month, accepts a $3 default tip, pays a $3.99 express delivery fee each time, and subscribes to a premium tier at $9.99 per month pays nearly $288 per year on a product marketed as free and interest-free.

3. Why do cash advance apps use tips instead of fees?

Tips are classified as voluntary payments rather than fees or interest under most consumer lending regulations. This means they do not need to be disclosed in APR calculations or fee schedules, unlike interest and mandatory charges.

4. Does Beem Everdraft charge any tips or delivery fees?

No. Beem Everdraft charges no tips, no express delivery fees, and no monthly subscription. Instant fund delivery is included in the core product at no additional cost, and there is no tip prompt at any point in the advance request process.

5. How is Beem Everdraft free if other apps need tips to stay profitable?

Beem generates revenue through its broader platform of financial services, including smart money transfers, personal loans, credit building tools, and AI-powered financial products like BudgetGPT. This means Beem does not need to extract tips, delivery fees, or subscription revenue from the cash advance product to sustain the business.