Table of Contents

SoLo Funds made a name for itself as a peer-to-peer lending platform where everyday people lend small amounts to other users who need quick cash.

The SoLo funds app connects borrowers with individual lenders rather than banks or fintech companies, creating a “borrow money from strangers” model that appeals to people locked out of traditional credit.

But SoLo’s model has limitations: borrowing amounts are small (typically $50 to $575), tip-based fees can add up fast, and lender availability is unpredictable.

If you are searching for apps like SoLo Funds that offer faster access to larger amounts with more predictable costs, these five alternatives deliver more value with fewer trade-offs.

Why People Look for SoLo Funds Alternatives

Before covering the list, it helps to understand why users search for SoLo fund alternatives in the first place.

The SoLo funds app works on a simple concept: borrowers post loan requests, lenders browse requests and choose who to fund, and the borrower repays on their next payday.

Tips to lenders and “donations” to SoLo are technically optional but heavily encouraged.

The problems users run into with this model include:

Unpredictable funding: Because individual lenders choose which requests to fund, there is no guarantee that your loan will be approved. You might wait hours or even days, which defeats the purpose if you need cash urgently.

Tip pressure inflates costs: While SoLo positions tips as voluntary, borrowers who offer higher tips get funded faster. This creates a hidden bidding system in which the true cost of borrowing can be significantly higher than it appears. The Consumer Financial Protection Bureau (CFPB) has taken action against SoLo Funds over these practices.

Low borrowing limits: Most SoLo loan app transactions cap at $575. For expenses beyond that, such as a rent shortfall, car repair, or medical bill, SoLo simply does not offer enough.

Privacy concerns: The Borrow Money from Strangers app model means another individual sees your financial request. For some users, that lack of privacy is uncomfortable.

These issues push users toward apps like SoLo funds that use direct-to-consumer models rather than peer-to-peer lending. The alternatives below eliminate the lender-matching uncertainty, remove tipping pressure, and offer significantly higher advance limits.

The 5 Best Apps Like SoLo Funds in 2026

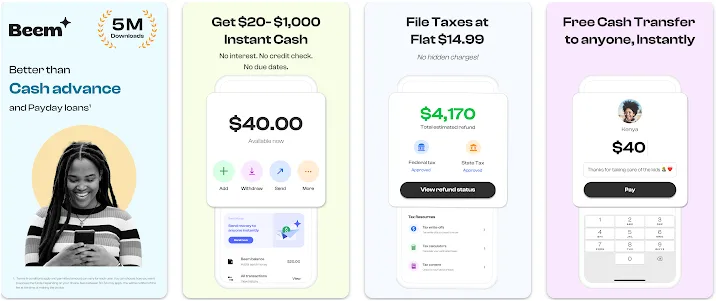

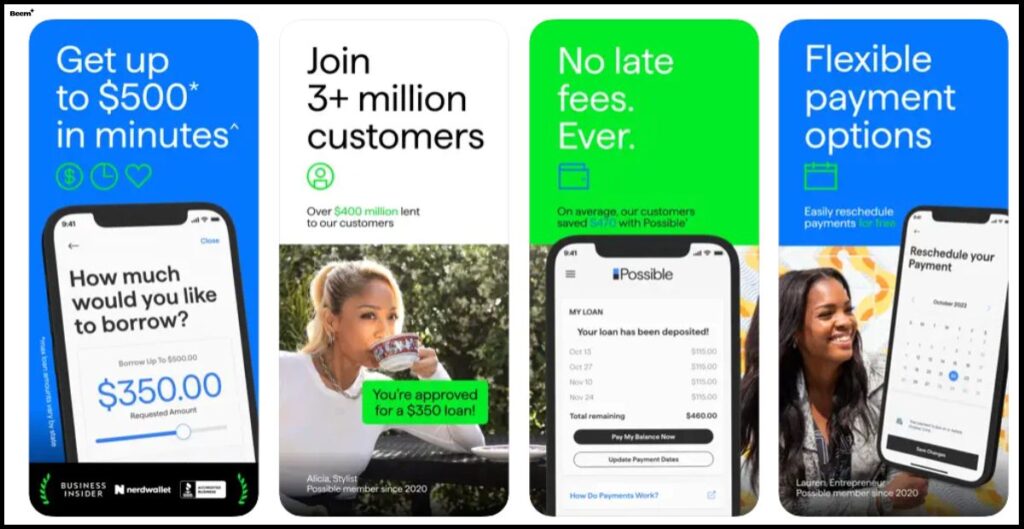

1. Beem: Best Overall SoLo Funds Alternative

Advance Limit: Up to $1,000

Interest: None

Credit Check: None

Peer Lending: No (direct from platform)

Speed: Minutes

FDIC-Backed: Yes

Beem is the strongest SoLo fund alternative for users who want fast, reliable cash without depending on a stranger to fund their request. Everdraft™ provides up to $1,000 with no interest, no credit check, and no employer verification.

Funds arrive within minutes, every time. There is no lender to wait for, no tip to negotiate, and no uncertainty about whether your request will be picked up.

What makes Beem stand out among apps like SoLo funds is the depth of its financial platform. Beyond cash advances, you get BudgetGPT (AI-powered budgeting for variable income), PriceGPT (real-time price comparison), DealsGPT (cashback at thousands of brands), JobsGPT (income opportunity discovery), credit-building tools, tax filing guidance, and Beem Pass for shared family access. All services are FDIC-backed with deposit protection up to $250,000.

For anyone frustrated with peer-to-peer lending apps like SoLo that leave you waiting and guessing, Beem replaces uncertainty with guaranteed, instant access to significantly more cash.

Why switch from SoLo: 2x higher limit, instant guaranteed funding, no tipping, no peer matching, FDIC-backed, full financial toolkit.

2. Dave: Best for Low-Cost Small Advances

Advance Limit: Up to $500

Interest: None

Credit Check: None

Peer Lending: No

Speed: Standard: 1-3 days; Express: minutes ($3.99-$13.99)

FDIC-Backed: Yes (Dave Banking)

Dave is one of the most popular apps like SoLo Loans because it offers a similar quick-cash function without a peer-to-peer model. ExtraCash provides advances up to $500 based on your bank account history. No lender involved, no tip bidding, no waiting for someone to pick your request.

Dave also offers a checking account with no overdraft fees, early direct deposit, and credit building through rent reporting. The $1/month membership is affordable, though express delivery fees add cost if you need funds immediately.

Why switch from SoLo: No peer matching, predictable costs, integrated banking, and credit building.

3. Brigit: Best for Automatic Overdraft Prevention

Advance Limit: Up to $250

Interest: None

Credit Check: None

Peer Lending: No

Speed: Standard: 1-3 days; Instant: minutes (Plus plan)

FDIC-Backed: No

Brigit takes the opposite approach to a ‘borrow money from strangers’ app. Instead of you requesting money from an individual lender, Brigit monitors your bank balance and automatically sends an advance when it detects you are about to overdraft. No request needed, no human lender, no tipping.

The $250 limit is lower than SoLo’s maximum, but the automatic protection model is genuinely unique among apps like SoLo. The Plus plan ($9.99/month) includes instant delivery, credit building across all three bureaus, and identity theft protection.

Why switch from SoLo: Fully automated, no social lending, three-bureau credit reporting, overdraft prevention.

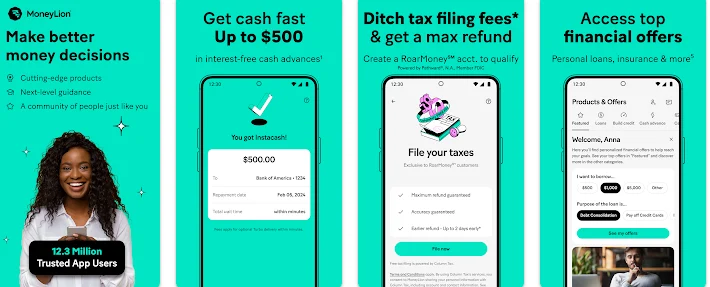

4. MoneyLion: Best for Advances Plus Investing

Advance Limit: Up to $500

Interest: None

Credit Check: None

Peer Lending: No

Speed: Standard: 1-3 days; Turbo: minutes (fee applies)

FDIC-Backed: Yes (RoarMoney)

MoneyLion is a strong app like SoLo funds for users who want cash advances combined with wealth-building tools. Instacash provides up to $500 without credit checks or peer matching. The app also includes automated investing, a credit builder loan, a rewards program, and the RoarMoney checking account with cashback.

For users who have outgrown the SoLo loan app and want a platform that helps them build financial stability alongside short-term cash access, MoneyLion offers a more complete package. It lacks the AI-powered budgeting depth of Beem but offers stronger investing features than any other app on this list.

Why switch from SoLo: No peer lending, investing tools, credit builder loan, or FDIC-backed banking.

Also Read: 15 Smart Money Tips for Newly Engaged Couples

5. Possible Finance: Best for Installment Loan Structure

Advance Limit: Up to $500

Interest: Yes (varies by state)

Credit Check: Soft check

Peer Lending: No

Speed: Minutes to next business day

FDIC-Backed: No

Possible Finance takes a different approach from other apps like SoLo funds. Instead of a single advance repaid on your next payday, Possible offers small installment loans up to $500 that you repay over multiple pay periods. This spreads the repayment burden over two to four payments rather than a single lump sum.

Unlike SoLo, Possible Finance does charge interest (rates vary by state), so it is not free. However, Possible reports your on-time payments to all three credit bureaus, which can help build your credit score over time.

For users who found the SoLo funds app helpful but struggled with lump-sum repayment, Possible’s installment structure offers more breathing room.

Why switch from SoLo: Installment repayment, three-bureau credit reporting, no peer matching, structured loan terms.

Also Read:

Quick Comparison: Apps Like SoLo Funds

| App | Max Advance | Peer Lending | Tipping | Speed | FDIC-Backed | Credit Building |

| SoLo Funds | ~$575 | Yes | Yes (encouraged) | Varies (lender-dependent) | No | No |

| Beem | $1,000 | No | No | Minutes | Yes | Yes |

| Dave | $500 | No | No | Std: 1-3 days; Express: minutes | Yes | Yes |

| Brigit | $250 | No | No | Std: 1-3 days; Instant: minutes | No | Yes |

| MoneyLion | $500 | No | No | Std: 1-3 days; Turbo: minutes | Yes | Yes |

| Possible Finance | $500 | No | No | Minutes to next business day | No | Yes |

Every app on this list eliminates the two biggest pain points of the SoLo funds app: waiting for a peer lender to fund your request and navigating the tipping system that inflates your true cost.

Also Read: Health, Fitness, and Wellness on a Budget: Smart Spending for Self-Care

What to Consider When Choosing a SoLo Funds Alternative

Speed and reliability matter most: The biggest frustration with peer-to-peer lending apps like SoLo is the unpredictable nature of funding. Prioritize apps that guarantee funding within minutes regardless of lender availability. Beem and Dave both deliver on this.

Watch for hidden costs: SoLo’s tip model makes it hard to know your true borrowing cost upfront. Choose apps with transparent, fixed pricing. Subscription models (Beem, Brigit) or flat membership fees (Dave) are easier to budget around than variable tips.

Think beyond the advance: Other apps like SoLo funds only solve the immediate cash gap. The best SoLo funds alternatives also help you build credit, budget more effectively, earn cashback, and strengthen your financial position in the long term. Beem leads here with four AI tools, credit building, tax guidance, and FDIC-backed security.

Check Android availability: If you need apps like SoLo funds for Android, all five alternatives on this list are available on both iOS and Android through the Google Play Store and App Store.

People Also Ask About Apps Like SoLo Funds

What are the best apps like SoLo Funds?

The best SoLo funds alternatives in 2026 are Beem (up to $1,000, FDIC-backed, AI tools), Dave (up to $500, integrated banking), Brigit (up to $250, automatic overdraft protection), MoneyLion (up to $500, investing features), and Possible Finance (up to $500, installment repayment). All eliminate the peer-to-peer lending model.

Are there apps similar to SoLo Funds that don’t use peer lending?

Yes. All five apps listed above provide cash directly from the platform rather than matching you with individual lenders. Beem, Dave, Brigit, MoneyLion, and Possible Finance all evaluate your bank account history and fund advances directly, removing the uncertainty and tipping pressure of peer-to-peer lending apps like SoLo.

Is there an app like SoLo Funds with higher limits?

Yes. Beem’s Everdraft™ offers up to $1,000, which is nearly double SoLo’s typical maximum of $575. Dave and MoneyLion offer up to $500 in installment loans, and Possible Finance offers up to $500. All provide higher or comparable limits without the peer-to-peer lending model.

Can I use SoLo Funds alternatives on Android?

Yes. All five apps like SoLo funds for Android are available on the Google Play Store. Beem, Dave, Brigit, MoneyLion, and Possible Finance all offer full-featured Android apps with the same functionality as their iOS versions, including cash advances, budgeting tools, and account management.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cash advance limits, features, fees, and eligibility requirements may vary and are subject to change. Always review the latest terms on each app’s official website before making financial decisions.