Table of Contents

Living on veterans disability compensation can be steady, but it isn’t always flexible. Bills and life expenses do not politely wait for your deposit date. A prescription, a car repair, a utility shutoff notice, or even a grocery run can hit a few days before your payment lands, and that is how people end up searching for cash advance apps in the first place.

This guide is written for veterans with disability in 2026 who want a clear, practical way to evaluate cash advance apps for disabled veterans without getting dragged into high-cost debt. We will cover what matters most for veterans with disability income: deposit timing, eligibility rules, fees that quietly add up, and what to do if an app does not fit your situation.

A quick note on tone: the point here is not “just budget better.” Disabled veterans already know how to stretch dollars. The point is to create breathing room without creating a new financial problem.

Why Veterans Disability Income Creates A Unique Cash Flow Problem

VA disability compensation is typically paid monthly, and the payment you receive is generally for the previous month. Many sources explain this as being paid “in arrears,” and the schedule is commonly described as the first business day of the following month, with weekend and holiday adjustments that can shift the deposit date earlier.

That structure is predictable, but it is also rigid. When you have a fixed payment date and you are managing recurring expenses like rent, insurance, phone bills, utilities, co-pays, and groceries, the tightest squeeze often happens in the final week of the month. That is exactly where cash advance apps can be useful if they are transparent, reasonably priced, and aligned with recurring deposit income rather than employer payroll.

What disabled veterans should look for in cash advance apps in 2026

A good cash advance app for veterans disability should make five things clear before you commit:

1) Does it accept government benefits deposits as qualifying income?

Some apps are explicit about this. Some are vague. If an app requires “qualifying direct deposit,” look for the definition. Chime explicitly includes government benefits payers and lists the Department of Veterans Affairs.

2) Is there a real free option?

Many apps say “no interest,” but still charge for speed. A free option usually means standard ACH transfer that takes a few business days. Brigit, for example, describes free delivery in 2 to 3 business days and optional express delivery for a fee.

A free option matters because a flat instant fee can be painful when you only need a small amount.

3) How does repayment work and what is the risk to your bank account?

Most apps recover repayment automatically when a qualifying deposit arrives. That is convenient, but it can also collide with rent, utilities, or other auto-payments if your balance runs tight. You want an app that explains repayment clearly and does not hide the behavior in fine print.

4) What is the total cost for how you actually use it?

Subscription apps can be reasonable if you use them regularly. If you only need help once in a while, a subscription can become the biggest cost. On the other side, percentage-based fees can become expensive if you take larger advances.

5) Is it available in your state?

Some products are not available everywhere. Chime MyPay lists a set of states where it is currently not available. State availability is not exciting, but it is the difference between “sounds great” and “actually usable.”

People Also Read: Why Beem is America’s Favorite App

Cash Advance Apps Worth Considering For Veterans Disability In 2026

Below are options that can fit veterans disability income depending on your deposit setup, eligibility, and state. This is not a promise of approval. This is a practical shortlist based on what these products publicly say about qualifying deposits, fees, and delivery options.

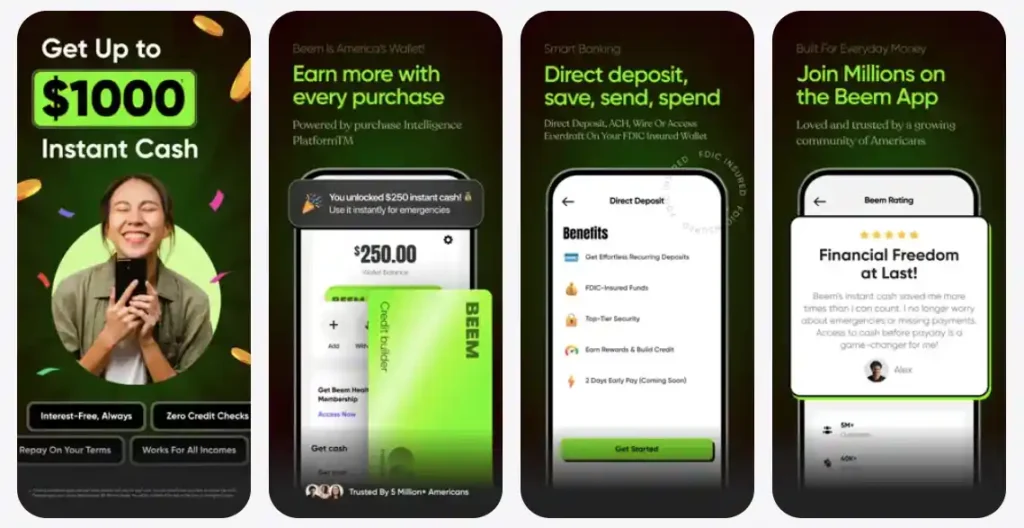

Beem

Beem’s Everdraft™ is designed as a deposit and activity-based cash advance feature. Beem describes Everdraft™ as reviewing income and account activity to determine eligibility and emphasizes that there is no hard credit inquiry involved. The Beem app also positions Everdraft™ as a financial bridge tied to the next incoming deposit and states you are not taking out a loan.

For veterans’ disability income, the key advantage is predictability through plan structure. Beem’s pricing page shows plan tiers with emergency cash access ranging from $10 on Lite to up to $1,000 on Pro. It also shows that standard bank transfer is free with a stated 3 to 5 business day timeline and that instant debit delivery is available with plan-based starting fees.

If you want a cash advance app where access levels and delivery costs are clearly separated, Beem is built around that approach.

Chime

Chime MyPay is one of the clearest examples of a product that explicitly calls out government benefits deposits as qualifying direct deposits. It defines qualifying direct deposits to include government benefits payers and lists the Department of Veterans Affairs as an example.

Chime also describes MyPay pricing in a straightforward way: there are no mandatory fees, money can arrive fee-free within 24 hours, and there is an option to receive money instantly for a fee that is generally described as $2 to $5 per advance. It also notes MyPay is not currently available in certain states, which matters if you are trying to set this up quickly.

If your veterans disability deposit is landing as a qualifying direct deposit into a Chime Checking Account, this is one of the more direct fits.

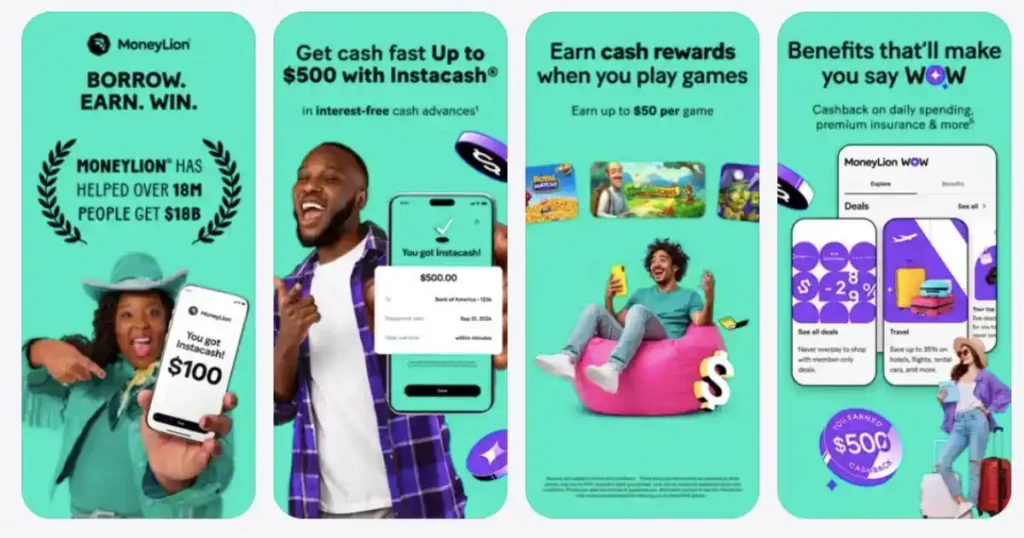

MoneyLion

MoneyLion positions Instacash as scaling with qualifying income and notes that setting up direct deposits into a RoarMoney account can increase available Instacash amounts.

They also publish a pricing table showing regular delivery fees as $0 and optional Turbo delivery fees that vary by disbursement amount and whether funds go to a RoarMoney account or an external account.

For disabled veterans, this option can be a fit if you are comfortable routing deposits or maintaining an account setup that MoneyLion treats as qualifying. The key thing to watch is the Turbo fee structure and whether the faster delivery option is worth it for the amount you actually need.

Varo

Varo advertises cash advances in a smaller range initially, describing access between $20 and $250 now, with the ability to build up to $500 over time. It also states there is no interest, no credit check, and a flat fee per advance, with the fee range tied to the amount.

This can be a good fit if your goal is a smaller bridge amount and you prefer a one-time fee model rather than monthly subscriptions. The tradeoff is that it may not meet needs for larger emergencies and eligibility can vary.

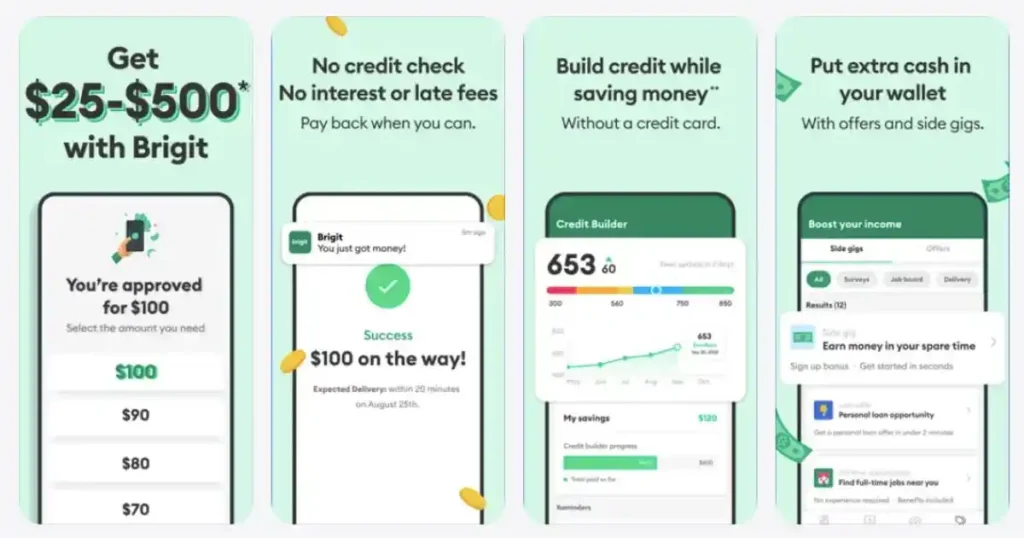

Brigit

Brigit describes a free delivery option that arrives in 2 to 3 business days and express delivery for a fee. Brigit also includes disclosures about eligibility ranges and that a monthly subscription may apply.

For disabled veterans, Brigit can be a fit if your deposit pattern and account activity meet its eligibility requirements and the subscription cost feels worth it for how often you actually need support. If you only need one small advance occasionally, subscription apps should be evaluated carefully.

Dave

Dave’s fee schedule is more detailed than many consumers expect. The published ExtraCash fee schedule describes an overdraft or “ExtraCash fee” that can be 5% of each overdraft amount, with a $5 minimum, and also lists optional express and ACH fees depending on delivery route.

This does not automatically make Dave “bad,” but it does mean it is critical to understand your total cost before using it as a veterans disability bridge. Percentage-based or minimum-based fees can feel heavy when the advance amount is small.

Klover

Klover describes advances with no interest or credit checks and positions a standard delivery option as free, with optional express fees to expedite disbursement. This can be useful if you are seeking a basic cash advance app and are comfortable choosing free standard delivery most of the time.

People Also Read: Cash Advance Apps for Social Security Recipients

Cash Advance Apps For Disabled Veterans Check (2026)

This table is meant to help you filter quickly. Exact eligibility and availability can change, so treat this as a comparison of publicly described models, not a guarantee.

| App | Can qualify from government benefits deposits? | Typical maximum mentioned | Free delivery option | Fast delivery cost model | What to know |

| Beem Everdraft™ | Deposit and activity based eligibility (not payroll only) | Up to $1,000 on Pro plan | ACH 3 to 5 business days, free | Instant to debit starts at plan-based fees | Plan tiers make access predictable |

| Chime MyPay | Explicitly includes government benefits payer deposits, mentions VA | Up to $500 | Fee-free within 24 hours | Instant fee generally $2 to $5 per advance | Not available in some states |

| MoneyLion Instacash | Direct deposit into RoarMoney can increase access | Up to $1,000 depending on income | Regular delivery $0 | Optional Turbo fees vary by amount and destination | Good if you are OK with their account setup |

| Varo Cash Advance | Qualifying account linked (deposit requirements vary) | $20 to $250 now, build to $500 | Not positioned as “free,” fee per advance | Flat fee per advance, range by amount | Best for smaller advances |

| Brigit | Eligibility varies, subscription may apply | Eligibility-based, range varies by user | 2 to 3 business days, free | Express delivery fee may apply | Subscription cost matters if you use it rarely |

| Dave | Depends on linked account and product structure | Up to $500 marketed historically | ACH free | Fees include % and minimum-based components | Understand the fee schedule first |

| Klover | Linked account based eligibility, express optional | Up to $400 | Standard delivery described as free | Optional express fee disclosed at request | Useful if you stick with standard delivery |

Last Thoughts

Cash advance apps can be genuinely useful for disabled veterans in 2026, especially when the cash crunch is about timing rather than long-term affordability. The key is choosing an app that aligns with veterans disability deposits, keeps fees transparent, and gives you a truly free option when you can wait.

If you want a clear, plan-based structure and deposit-driven eligibility, Beem’s Everdraft™ is built around that model, with access tiers and delivery options that are spelled out up front. Whichever option you choose, the goal stays the same: solve the short-term gap without creating a long-term financial burden.

People Also Ask

1. Can disabled veterans use cash advance apps with VA disability deposits?

Yes, some cash advance apps can work with veterans disability income as long as your deposit is treated as a qualifying direct deposit or the app’s eligibility system recognizes your recurring deposit pattern. The important detail is that not all apps define qualifying deposits the same way, so you should look for products that explicitly include government benefits deposits or rely on deposit and account activity rather than employer payroll verification.

2. Which cash advance apps are most compatible with veterans disability income?

Apps that either explicitly accept government benefits deposits as qualifying income or evaluate recurring deposits tend to be more compatible than wage-only products. Chime explicitly lists government benefits payer deposits and names the Department of Veterans Affairs as an example, while Beem describes eligibility based on income and account activity rather than hard credit checks.

3. Do cash advance apps charge interest like payday loans?

Many cash advance apps position themselves as no-interest options, but they can still cost money through subscriptions, instant delivery fees, and other service fees. The real comparison is not “interest vs no interest.” The real comparison is your total out-of-pocket cost for the amount you need and how often you use it.

4. What is the safest way to use cash advance apps on veterans disability income?

Use them as a bridge, not a routine. Keep advances as small as possible, choose free standard delivery whenever timing allows, and keep a small buffer in your linked account so repayment does not collide with rent or utilities. If you find yourself advancing every month, it may be time to reduce recurring pressure instead of relying on repeated advances.

5. Are there consumer protections for veterans who get trapped by high-cost lenders?

There are protections and resources, but they vary. MLA protections are strongest for active duty servicemembers and certain dependents, while veterans may need to rely on state protections and general consumer protection tools. The CFPB provides financial resources that specifically include veterans and military families, and it can be a practical place to learn your options or file a complaint if you believe a lender violated rules.