Yes. You can have multiple cash advance apps installed on your phone, active accounts on all of them, and still use Beem without any conflict, penalty, or terms-of-service violation. Beem does not require exclusivity.

Neither do Dave, Brigit, EarnIn, Cleo, or any of the other major cash advance apps on the market. There is no rule against it, no technical block preventing it, and no “loyalty clause” buried in anyone’s terms of service.

That is the simple answer. But the more useful answer involves understanding why people use multiple cash advance apps, when it actually makes financial sense, when it becomes a warning sign, and how to structure a multi-app approach that works for you rather than against you.

Why People Use Multiple Cash Advance Apps

Nobody downloads five cash advance apps because they are bored. People stack cash advance apps for specific, practical reasons.

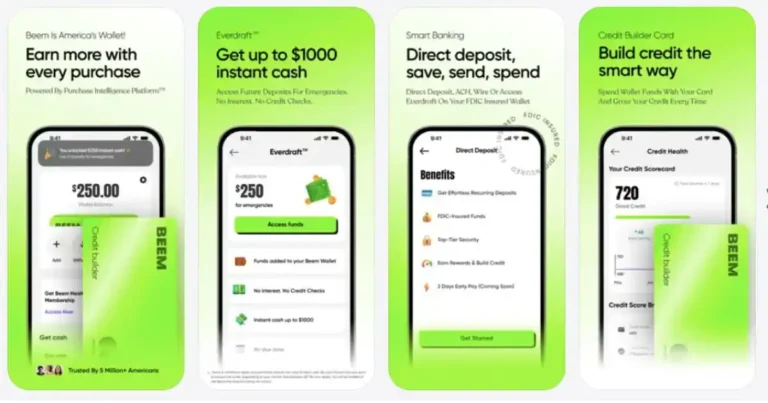

Different apps have different limits. Beem offers up to $1,000 through Everdraft™. Dave caps at $500. Brigit caps at $250. EarnIn allows $150 per day up to $750 per pay period.

A user whose emergencies occasionally exceed what one app can provide keeps a second or third app as backup for larger shortfalls.

New user limits start low. Most cash advance apps start new users at $50 to $150 and increase limits over time based on deposit history and repayment behavior. A user who just signed up for Beem might have a $200 starting limit while their profile builds.

Having Dave or EarnIn already established with a higher limit from months of usage provides a safety net during Beem’s ramp-up period.

Delivery speed varies. Some apps offer free instant delivery on certain advances while others charge $3 to $6 for express. A user with accounts on multiple apps can compare real-time delivery fees and choose the cheapest path to same-day funds for each specific advance.

Feature sets differ. Someone might use Beem for its AI toolkit (BudgetGPT, DealsGPT, PriceGPT) and Everdraft™ for larger advances, Dave for its Side Hustle gig connections and banking, and Brigit for its automatic advance feature that sends money before you overdraft.

Each app has a specialty. Using multiple apps is not about distrust in any single platform. It is about assembling the best tools for different situations.

Do Cash Advance Apps Know About Each Other?

This is the question people are most nervous about asking. The answer: generally, no.

Cash advance apps verify your income and spending through your linked bank account. They can see your deposits, your withdrawals, and your transaction history. If you take an advance from Dave and it shows up as a deposit in your bank account, Beem can technically see that transaction. The same is true in reverse.

However, cash advance apps do not communicate with each other directly. There is no shared database of “people who use advance apps” that platforms check against. Beem does not call Dave to ask if you have an outstanding advance. Dave does not flag your account because Brigit deposited $250 yesterday.

What the apps do see is the net effect on your bank account. If you have three outstanding advances from three different apps and your checking balance is $14, every app connected to that account can observe that your balance is low and your upcoming deductions are heavy.

This may affect the advance amount each app is willing to offer you. The algorithm does not care which specific app deposited or withdrew the money. It cares about your overall financial picture: income in, money out, balance remaining.

So while apps do not “know about each other” in any formal or coordinated way, the financial behavior created by using multiple apps simultaneously is fully visible through your bank account data.

When Using Multiple Cash Advance Apps Makes Sense

Having multiple cash advance apps is not inherently risky. In certain situations, it is genuinely the smarter approach.

During the Ramp-Up Period on a New App

When you first sign up for Beem, your Everdraft™ limit may start lower than the $1,000 maximum while the system evaluates your deposit patterns and builds your profile. During this ramp-up period, having an established account on Dave or EarnIn gives you access to higher limits from those platforms while your Beem limit grows.

Once your Everdraft™ limit reaches a level that covers your typical needs, you can phase out the other apps or keep them as dormant backups.

When One App’s Advance Is Outstanding

Beem operates on a one-active-advance-at-a-time model. If you have an Everdraft™ advance outstanding and a second unexpected expense hits before repayment, a separate app with its own independent advance can cover the second expense.

This is the legitimate “backup” use case. You are not stacking debt recklessly. You are handling two separate financial events that happened to overlap.

For Feature Diversification

This is the most strategic reason to maintain multiple apps. You might use Beem as your primary platform for Everdraft™ advances and AI financial tools, Brigit for its automatic overdraft protection (it monitors your balance and sends money proactively), and Dave for its Side Hustle gig connections when you need extra income.

Each app plays a different role. The advances are secondary to the unique features each platform provides.

When Comparing Express Delivery Fees

Express delivery costs vary: $0 to $5.99 depending on the app, the amount, and the delivery method. If you need $200 today and Beem’s express fee is $3.99 but EarnIn’s Lightning Speed is $1.99 for the same amount, choosing EarnIn for that specific advance saves $2. Over a year of occasional express deliveries, comparison shopping between apps reduces your total transfer costs.

When Multiple Cash Advance Apps Become a Problem

There is a clear line between strategic multi-app usage and a pattern that signals financial trouble. Here is where that line sits.

Taking Advances From Multiple Apps in the Same Pay Period to Cover the Same Gap

If you need $300 for groceries and you take $150 from Beem and $150 from Dave to reach $300, that is fine. But if you take $300 from Beem AND $300 from Dave because $300 was not enough and you are hoping to sort it out later, you now owe $600 from your next paycheck.

This is advance stacking, and it is the multi-app equivalent of maxing out multiple credit cards. Each individual advance is manageable. The combined repayment obligation is not.

Repaying One App’s Advance With Another App’s Advance

This is the cash advance version of a debt spiral. You take $200 from Dave to cover your Beem repayment, then take $200 from EarnIn to cover your Dave repayment, then take $200 from Brigit to cover your EarnIn repayment.

You have not solved anything. You have moved the same $200 of debt across four platforms and potentially added delivery fees at each step. If you catch yourself doing this, stop immediately. The problem is not which app to use. The problem is a structural income-vs-spending gap that advances cannot fix.

Your Combined Monthly Advance Repayments Exceed 25% of Your Take-Home Pay

A useful guardrail: if the total repayment amount across all your active advances would consume more than 25% of your next paycheck, you are overleveraged. On a $2,000 biweekly paycheck, that means combined outstanding advances should not exceed $500.

Beyond that threshold, your post-repayment balance is too thin to cover normal expenses, which means you will likely need another advance immediately after repaying, which is the beginning of a cycle.

You Cannot Name What Each App Is For

Healthy multi-app usage has a reason for each app. “Beem for large advances and budgeting. Brigit for automatic overdraft protection. Dave for gig connections.” If your answer is “I use all of them because I need as much money as possible from as many sources as possible,” that is not a strategy. That is a symptom.

The Smartest Multi-App Strategy for 2026

If you are going to use multiple cash advance apps alongside Beem, here is the structure that maximizes benefit while minimizing risk.

Primary app: Beem. Use Everdraft™ as your main advance source. The $1,000 limit is the highest on the market, which means Beem alone covers most emergencies without needing a second app. Route your primary direct deposit through the bank account linked to Beem to build your limit over time. Use BudgetGPT for budgeting, DealsGPT for cashback, and PriceGPT for price comparison.

Backup app: One additional app with a different specialty. Brigit if you want automatic overdraft protection. Dave if you want banking and gig work connections. EarnIn if you prefer the daily-draw model for small, frequent access. Keep one backup app active for the rare situation where your Everdraft™ instant cash advance is outstanding and a second expense hits.

Dormant apps: Everything else. You do not need five active instant cash advance apps. Two is sufficient for 99% of situations (primary plus backup). Keep other apps installed if you want, but do not actively maintain subscriptions on platforms you rarely use. Every $5.99 or $9.99 monthly subscription on a dormant app is money that could go toward savings instead.

The exit strategy: one app plus savings. The ultimate goal is to need fewer instant cash advance apps over time, not more. As your Beem Everdraft™ limit grows and your savings build (even $500 to $1,000 in a high-yield savings account), the need for backup apps disappears. The healthiest financial state is one advance app for occasional timing gaps plus an emergency fund for everything else. Every app you stop needing is a sign of progress.

Does Using Other Apps Affect Your Beem Account?

Directly, no. Beem does not penalize you for having accounts with Dave, Brigit, EarnIn, or any other platform. Your Everdraft™ eligibility and limit are determined by your bank account activity, not by which other apps you use.

Indirectly, your behavior across all apps shows up in your bank data. If multiple advance repayments are pulling from the same account and leaving your balance consistently low, Beem’s algorithm sees a riskier financial profile. That could translate to a lower advance limit or slower limit growth compared to a user whose bank account shows healthier patterns.

The practical takeaway: using other apps will not get you banned from Beem or reduce your limit as a punishment. But the combined effect of multiple repayments draining your account can affect the financial signals Beem’s system reads.

The best way to maintain strong Everdraft™ access while using other apps is to keep your bank balance healthy and ensure you never overcommit across platforms.

How to Transition From Multiple Apps to One

If you are currently juggling three or four emergency advance apps and want to simplify, here is a gradual transition plan.

Step 1: Pick your primary. Choose the app with the highest limit, the best features for your situation, and the lowest cost. Beem’s combination of $1,000 Everdraft™ advances with zero interest, AI budgeting, cashback, and price comparison makes it the strongest single-app option for most users.

Step 2: Repay and pause secondary apps. Clear any outstanding advances on your backup apps. Do not close the accounts. Just stop actively requesting advances from them. Cancel paid subscriptions on apps you are not using.

Step 3: Build your primary limit. Focus your direct deposit and financial activity through the bank account linked to your primary app. Consistent deposits and on-time repayments grow your Everdraft™ limit faster when your bank data is clean and predictable.

Step 4: Start building savings. Every subscription canceled on a secondary app ($5 to $10/month) and every express delivery fee avoided ($2 to $6 per advance) is money that can go into a high-yield savings account. Over six months, that is $50 to $100 redirected toward a cash buffer that reduces your need for advances at all.

Step 5: Keep one backup dormant. Maintain one secondary app with a free tier (no active subscription) as emergency backup. If you ever face a situation where your Everdraft™ advance is outstanding and a second expense hits, the backup is ready without having cost you anything in the meantime.

FAQ: Multiple Cash Advance Apps and Beem

Can you use Beem and Dave at the same time?

Yes. You can have active accounts on both Beem and Dave simultaneously. Neither app restricts you from using other cash advance platforms. You can take an Everdraft™ advance from Beem and an ExtraCash advance from Dave in the same pay period if needed. Just ensure your combined repayments do not exceed what your next paycheck can comfortably absorb.

Do cash advance apps check if you use other apps?

Cash advance apps do not directly communicate with each other or check a shared database of users. However, they can see your bank account activity, including deposits from other advance apps and repayment withdrawals. Multiple advance-related transactions visible in your bank data may influence how each app’s algorithm assesses your financial profile and determines your advance limit.

Can using too many cash advance apps hurt you?

Having multiple accounts does not hurt you. Overusing them does. If combined advance repayments from multiple apps consume more than 25% of your next paycheck, you risk a cycle where every repayment triggers the need for another advance. The number of apps is not the problem. The total amount borrowed across all of them relative to your income is what matters.

Will using other apps lower my Beem Everdraft™ limit?

Not directly. Beem does not reduce your limit as a penalty for using other platforms. However, if multiple advance repayments are draining your bank balance and creating a pattern of low or negative balances, Beem’s algorithm may read those signals as higher risk, which could affect your limit. Keeping your bank account healthy regardless of how many apps you use protects your Everdraft™ access.

How many cash advance apps should you have?

Two is the practical sweet spot for most people: one primary app (Beem, for the highest limit and best feature set) and one backup for situations where your primary advance is outstanding. More than two active subscriptions typically costs more in monthly fees than the flexibility is worth. The long-term goal is one app plus an emergency fund.

Is it better to use one cash advance app or several?

One strong app is better than several weak ones. If your primary app offers a high enough advance limit to cover your typical emergencies (Beem’s Everdraft™ goes up to $1,000), you rarely need a second source. Multiple apps make sense during the ramp-up period when your primary limit is still building, or for feature diversification (e.g., Brigit for automatic advances, Dave for gig connections). Once your primary limit is established and you have savings, consolidating to one app simplifies your finances and reduces subscription costs.

Disclaimer: Cash advance app features, limits, and terms are subject to change. Always verify current terms directly with each provider. Using multiple cash advance apps simultaneously carries the risk of overcommitting repayment obligations. This article is for informational purposes only and does not constitute financial advice. Beem is not a bank. Banking services are provided by FDIC-insured partner institutions.