Five apps. All promising fast cash before payday. All claiming zero interest. All saying they are different from payday lenders and better than the competition. But line them up side by side and the differences are significant enough to cost you hundreds of dollars per year if you choose the wrong one.

This is not a ranking based on vibes or brand loyalty. It is a feature-by-feature, dollar-by-dollar comparison of Gerald, Dave, EarnIn, Brigit, and Beem across every metric that actually matters when you need money before Friday: how much you can get, how fast it arrives, what it costs, what strings are attached, and what else the app does for you beyond the advance itself.

The table tells the story before a single paragraph of analysis. But the numbers alone do not capture the user experience differences, the hidden costs, and the trade-offs that determine which app is actually best for your situation.

Here is what each app gets right, what it gets wrong, and who it is best for.

Gerald: The Fine Print Problem

Max advance: $100 | Cost: Free (but requires a purchase)

Gerald advertises “free” cash advances up to $100 with no fees, no interest, and no subscription. On paper, that sounds appealing. In practice, Gerald’s model has a catch that makes it fundamentally different from every other app on this list.

To unlock a cash advance with Gerald, you must first make a purchase through Gerald’s built-in Cornerstore marketplace. You buy a product (gift cards, phone plans, subscription services) through Gerald’s partner retailers, and only after completing that purchase does your cash advance become available. The advance itself costs nothing. The mandatory purchase costs $15 to $30 or more, depending on what you buy.

This is not a hidden fee. Gerald is transparent about the purchase requirement. But it effectively transforms a “free $100 advance” into a “$100 advance that costs $15 to $30 in forced spending.”

If you were going to buy that gift card or phone plan anyway, Gerald works. If you were not, you are paying $15 to $30 to access $100, which is an effective cost of 15% to 30% for a two-week advance. Annualized, that is comparable to a credit card cash advance.

Gerald’s $100 maximum is also the lowest on this list by a wide margin. For users facing a $300 grocery shortfall or a $600 car repair, $100 does not solve the problem.

Gerald holds an F rating from the Better Business Bureau, driven by customer complaints about the purchase requirement, advance delivery issues, and customer service responsiveness. The BBB rating is not the only factor in evaluating a cash advance app, but an F is unusually low for a consumer-facing financial product.

Best for: Users who regularly shop for gift cards, prepaid phone plans, or subscriptions through Gerald’s Cornerstore and view the advance as a bonus on spending they would do anyway.

Limitations: $100 cap, mandatory purchase to unlock advances, BBB F rating, limited availability, no financial tools beyond the advance.

Dave: The All-in-One Banking Play

Max advance: $500 | Cost: $5/month

Dave has evolved well beyond its original identity as a simple cash advance app. In 2026, Dave is a full digital banking platform that happens to include cash advances as one feature among many.

ExtraCash advances go up to $500 with no interest, no credit check, and no mandatory tipping. New users start with lower limits ($50 to $150) that build over time with consistent direct deposits and on-time repayments. Express delivery is available for a fee, and standard delivery takes one to three business days.

Dave’s real strength is the ecosystem around the advance. Dave Spending is a full checking account with no overdraft fees, no minimum balance, and early direct deposit (up to two days early). The Dave debit card offers cashback at select merchants.

Automatic budget alerts warn you when upcoming bills are about to hit your account. And the Side Hustle feature connects users to gig work opportunities (Instacart, Amazon Flex, Uber Eats, and others) when extra income is needed.

All of this for up to $5/month. In terms of pure value per dollar, Dave is one of the best deals in consumer fintech.

Best for: Users who want a complete banking replacement (checking account, debit card, budget alerts, gig connections) with cash advances as an integrated feature. Ideal for people who prefer one app handling everything.

EarnIn: The Earned Wage Access Pioneer

Max advance: $150/day, $750/pay period | Cost: Free (tips optional) | BBB Rating: Not rated

EarnIn pioneered the “earned wage access” model: you access money you have already worked for but have not yet been paid. The app connects to your bank account, monitors incoming deposits, and lets you cash out up to $150 per day, with a per-pay-period maximum of $750.

EarnIn’s daily model maps naturally to workers with predictable shift-based income. If you worked Tuesday through Friday and need $100 today, EarnIn lets you access it based on what you have already earned, not what you might earn next week.

This feels less like borrowing and more like getting your own money early, which is psychologically easier for users uncomfortable with the idea of a “cash advance.”

The pricing model is unique. EarnIn does not charge a subscription. Instead, it asks for optional tips after each cash-out. You can tip $0 and use the service indefinitely. However, tipping unlocks higher limits and faster access over time. Users who never tip may find their maximum stuck at lower levels. The tip model is genuinely optional in the sense that the app works without it, but the incentive structure encourages tipping for a better experience.

Balance Shield is a useful add-on feature: it monitors your bank balance and alerts you (or automatically sends a small transfer) when your account drops below a threshold you set.

Best for: Hourly workers with predictable schedules who prefer daily access to small amounts rather than one larger lump-sum advance. Ideal for users who want a tip-based model with no mandatory subscription.

Limitations: $150 daily cap means you cannot access large amounts quickly. The $750 per-pay-period limit is competitive but not the highest. No banking features, no AI tools, no credit building. Tipping dynamics can feel ambiguous about what is truly “optional.”

Brigit: The Automatic Safety Net

Max advance: $250 | Cost: Free (Lite) / $9.99/month (Plus) | BBB Rating: A+

Brigit does something no other app on this list does: it sends you money without you asking for it. Brigit Plus monitors your bank balance around the clock and automatically deposits up to $250 into your account when it detects your balance is about to drop dangerously low. No app to open. No request to submit. No buttons to tap. You go about your day and Brigit handles the rest.

This proactive model is genuinely unique in the cash advance space. Every other app requires you to notice a problem, open the app, request an advance, and wait for delivery. Brigit eliminates the entire sequence.

For users who keep forgetting to request advances until after the overdraft has already hit, this automation is worth the $9.99/month by itself. At most banks, a single avoided overdraft ($35) pays for three and a half months of Brigit Plus.

Beyond advances, Brigit Plus includes a finance tracker, credit score monitoring (view only, not building), and identity theft protection. Brigit Lite (free) provides basic budgeting tools without the automatic advance or credit monitoring features.

Best for: Users who want hands-off overdraft protection and are willing to pay $9.99/month for the convenience. Ideal for people with variable income whose balances dip unpredictably and who do not always catch shortfalls in time.

Limitations: $250 maximum is the lowest active-advance ceiling after Gerald. The $9.99/month subscription is the highest on this list. Credit monitoring is view-only (Brigit does not build your credit). No banking, no AI financial tools, no gig connections.

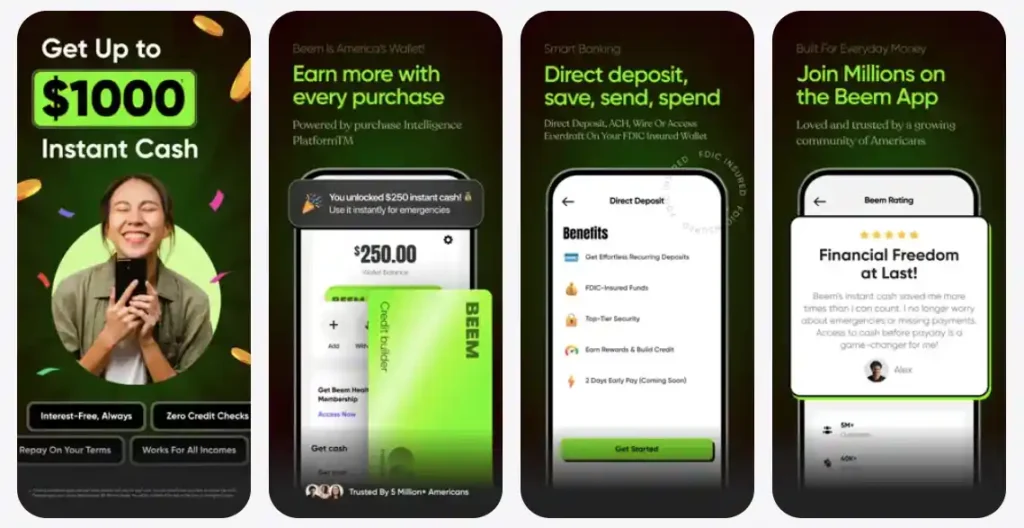

Beem: The Highest Limit Plus an AI Financial Toolkit

Max advance: $1,000 | Cost: Beem membership | BBB Rating: A+

Beem closes this comparison with the highest advance limit on the market and the most comprehensive feature set beyond the advance itself.

Everdraft™ provides cash advances up to $1,000 with zero interest, no credit check, and no mandatory purchase requirement.

For users whose emergencies regularly exceed $250 (car repairs, medical copays, insurance payments, rent shortfalls), Beem is the only app on this list that consistently covers the full amount in a single advance.

But what separates Beem from this comparison is not just the advance amount. It is the AI toolkit that addresses the financial patterns that create the need for advances in the first place.

BudgetGPT builds personalized spending plans that adapt to variable income. Not a generic budget template that assumes you earn the same amount every month, but an AI-driven plan that learns your actual income rhythm and spending patterns and adjusts accordingly.

DealsGPT automatically surfaces cashback opportunities and discounts on purchases you are already making. PriceGPT compares prices across retailers so you never overpay at checkout. Together, these tools recover money you would otherwise lose to overspending and missed deals, typically hundreds of dollars per year.

JobsGPT connects users to income opportunities matched to their skills and location, covering full-time, part-time, gig, and remote roles across all 50 states.

Beem also offers free credit building features, making it the only app in this comparison that actively helps improve your credit score rather than just monitoring it (Brigit) or ignoring it entirely (Gerald, Dave, EarnIn).

Beem is available in all 50 states with no geographic restrictions on any feature.

Best for: Users who want the highest possible advance limit combined with AI tools that reduce their reliance on advances over time. Ideal for anyone whose financial challenges go beyond a single timing gap and include budgeting, deal-finding, price optimization, income diversification, or credit building.

Head-to-Head: How Each App Stacks Up by Use Case

The “best” cash advance app depends on what you need it for. Here is a use-case guide.

| Scenario | Best App | Why |

| Largest possible advance | Beem | $1,000 max, no other app comes close |

| Complete banking replacement | Dave | Full checking, debit card, early deposit, Upto $5/month |

| Hands-off overdraft protection | Brigit | Automatic advances before you overdraft |

| Daily access to small amounts | EarnIn, BEEM | $150/day earned-wage access model |

| AI budgeting and price tools | Beem | BudgetGPT, DealsGPT, PriceGPT, JobsGPT |

| Finding extra income | Beem or Dave | JobsGPT (Beem) and Side Hustle (Dave) |

| Free Credit building | Beem | Only app with active credit-building features |

| Lowest monthly cost | EarnIn or Gerald | Both free (Gerald requires purchase, EarnIn encourages tips) |

| Best BBB rating | Brigit, BEEM | A+ rating |

Gerald’s “free” model is the most expensive on this list when you factor in mandatory purchases. Dave is the cheapest for active users. EarnIn’s cost depends entirely on tipping behavior. Brigit’s subscription is the highest fixed cost. Beem provides the most cash advance access per dollar spent.

The last row is the most revealing: max annual advance access. Over a year, Beem users can access up to $24,000 in zero-interest bridge funding. Gerald users max out at $2,400. That is a tenfold difference in financial flexibility from apps that all claim to serve the same market.

FAQ: Gerald vs Dave vs EarnIn vs Brigit vs Beem

Which cash advance app has the highest limit?

Beem offers the highest cash advance limit at up to $1,000 per advance through Everdraft™ with zero interest. Dave follows at $500, EarnIn at $750 per pay period ($150/day), Brigit at $250, and Gerald at $100. For users who need more than $250 per advance, Beem and Dave are the only viable options in this comparison.

Is Gerald really free?

Gerald does not charge a subscription fee or interest on advances. However, you must complete a purchase through Gerald’s Cornerstone marketplace (gift cards, phone plans, subscriptions) before your cash advance unlocks. These purchases typically cost $15 to $30 or more, making the “free” advance cost 15% to 30% of the amount borrowed. Gerald is free only if you were already planning to buy what Cornerstore sells.

Which cash advance app is best for gig workers?

Beem and Dave are the best options for gig workers. Beem’s Everdraft™ advances verify income through bank transaction history rather than employer verification, and JobsGPT connects users to additional gig opportunities. Dave’s Side Hustle feature similarly connects users to gig work (Instacart, Amazon Flex, Uber Eats). EarnIn also works for gig workers but its $150 daily cap limits usefulness for larger expenses.

Which app has the lowest fees?

EarnIn has the lowest mandatory fees at $0 (tip-based model, tips are optional). Dave charges upto $5/month with no other mandatory fees. Gerald is technically free but requires purchases that cost $15 to $30 per advance cycle. Brigit Plus costs $9.99/month. All five apps charge zero interest on advances.

Can I use more than one of these apps at the same time?

Yes. You can maintain active accounts on Gerald, Dave, EarnIn, Brigit, and Beem simultaneously. None of these apps require exclusivity. However, taking advances from multiple apps in the same pay period increases your combined repayment obligation, so monitor your total outstanding advances relative to your next paycheck to avoid overcommitting.

Which cash advance app builds credit?

Beem is the only app in this comparison that offers active credit-building features. Brigit provides credit score monitoring (view only) on its Plus plan but does not report to credit bureaus. Gerald, Dave, and EarnIn do not offer credit building or monitoring. If improving your credit score is a priority alongside cash advances, Beem is the only option that serves both needs.

Disclaimer: App features, fees, advance limits, and ratings are subject to change. Always verify current terms directly with each provider. BBB ratings reflect the bureau’s assessment at time of writing and may have been updated since publication. This article is for informational purposes only and does not constitute financial advice. Beem is not a bank. Banking services are provided by FDIC-insured partner institutions.