Best 15 Apps Like Zelle to Have In 2026

Zelle offers unparalleled convenience in today’s digital age. Swift transactions enable users to send and receive money seamlessly, eliminating the need for physical currency or traditional banking processes.

Zelle’s integration with major banks streamlines transfers and fosters financial efficiency. Furthermore, apps like Zelle, often provide real-time notifications, enhancing financial awareness.

However, exploring alternatives to Zelle is crucial, as reliance on a single platform poses security and accessibility risks.

Diversifying usage ensures adaptability to evolving technologies, safeguarding against potential service disruptions or security breaches. Evaluating alternative options guarantees users optimal flexibility, security, and an informed approach to their financial transactions.

Apps Like Zelle – 10 Best Alternatives

| App Name | Features |

|---|---|

| Beem | Emergency cash up to $1,000, no interest/credit checks, diverse sending methods |

| Chime | Fee-free overdraft protection, early paycheck access, automatic savings |

| Cash App | Easy money transfers, stock/Bitcoin investing, free debit card |

| Stripe | No setup/monthly fees, supports various payment methods, 24/7 support |

| PayPal | Versatile payment solution, global transactions, merchant services |

| Apple Cash | Seamless Apple integration, cashback rewards, easy to use |

| Google Pay | Wide compatibility, secure online payments, recordkeeping |

| Payoneer | Global reach, low fees, digital payment services, freelancer-friendly |

| Venmo | Social payment app, easy to use, free with bank/debit card |

| Wise | Transparent exchange rates, multi-currency account, good for large transfers |

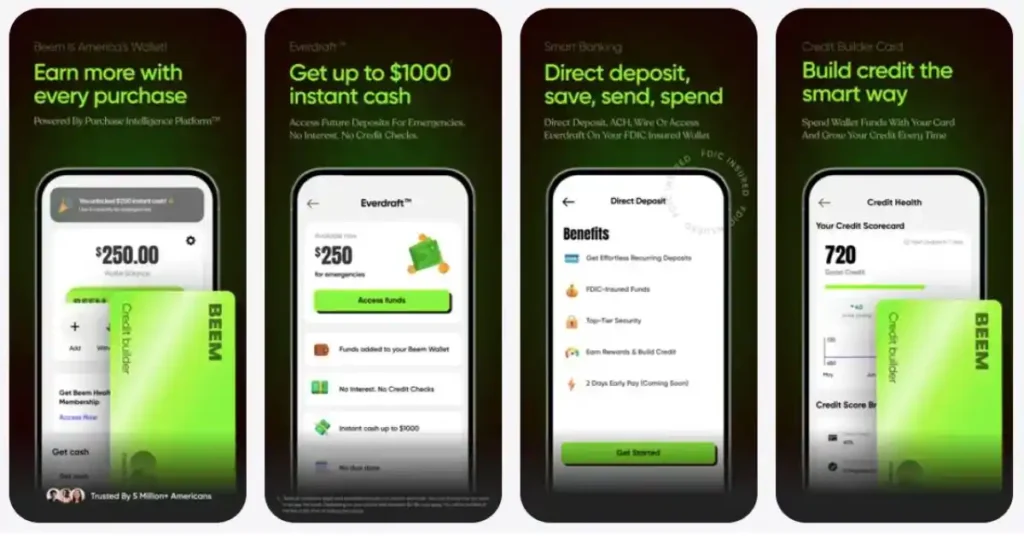

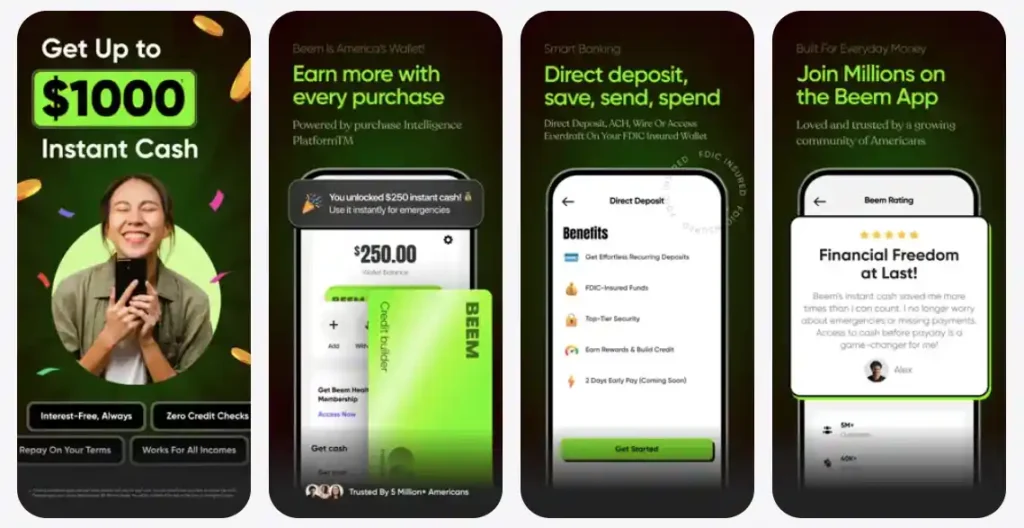

1. Beem

Beem, a robust alternative to Zelle, distinguishes itself as a #1 Smart Wallet App with a multifaceted approach to financial management.

Everdraft™ allows users to access instant cash up to $1,000 without interest, credit checks, or due dates, addressing emergency needs. Its versatility extends to sending money instantly to anyone without a bank account or the Beem app.

The Better Financial Feed™ aids in budget planning, credit monitoring, and identity theft protection, offering a comprehensive financial ecosystem.

Beem’s security measures, including PCI-DSS certification and bank-level encryption, ensure data protection, making it a secure and user-friendly financial solution.

Sending Limits

- Beem offers diverse options for instant cash, from sending money to anyone to gift cards, prepaid cards, bank transfers, and virtual credit cards.

- With sending options ranging from instant and free to 3-5 business days, Beem caters to various preferences and urgency levels.

Data Security

- Beem’s adherence to the Payment Card Industry Data Security Standard guarantees high protection for sensitive financial information.

- Employing industry-standard encryption for data transmission and storage,

- Beem prioritizes the privacy and security of user data, following best practices used by top global banks and FinTech companies.

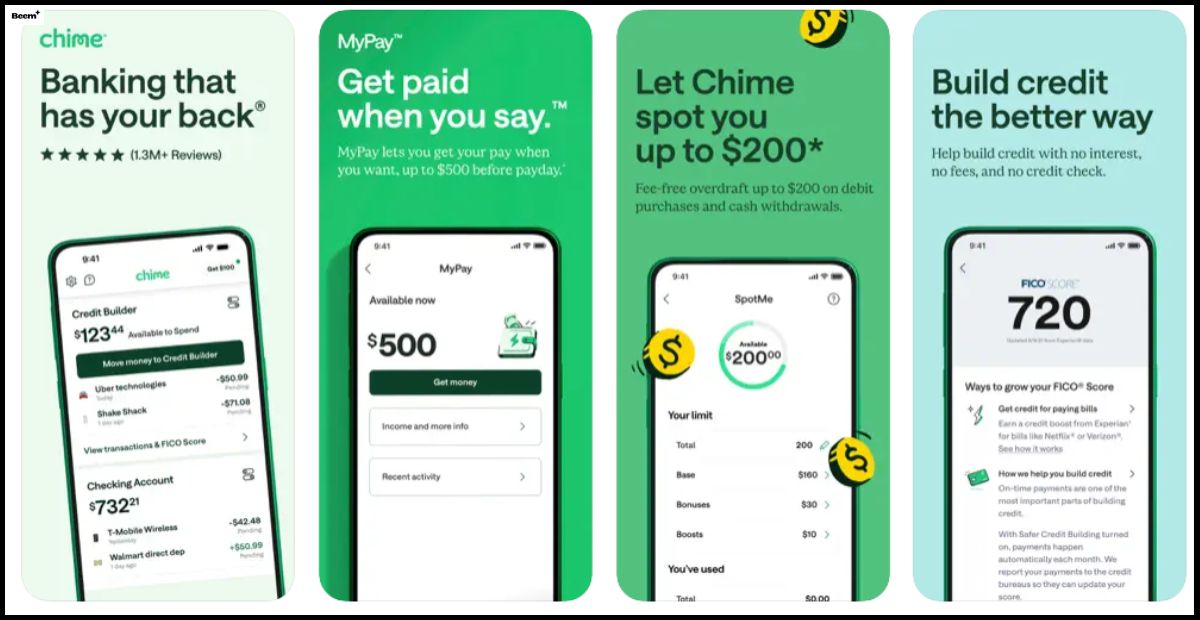

2. Chime

Chime emerges as a compelling Zelle alternative, offering a comprehensive financial ecosystem with unique features.

Unlike Apps like Zelle, Chime stands out by providing fee-free overdraft protection through its ‘SpotMe’ program, allowing users to overdraw up to $200 on debit card purchases without fees.

The app also offers early access to paychecks with direct deposit, up to two days earlier than traditional methods. However, users must consider limitations such as the absence of joint accounts and potential fees for cash deposits.

Chime’s emphasis on digital banking, early direct deposit, and no hidden fees positions it as a user-friendly alternative to Zelle.

Pros

- Chime’s ‘SpotMe’ program offers fee-free overdraft protection, allowing users to overdraw up to $200 on debit card purchases.

- Users who make direct deposits through Chime gain early access to their paychecks, receiving funds up to two days earlier than traditional methods.

- Chime facilitates automatic savings, enhancing financial planning and discipline.

- Chime distinguishes itself by avoiding hidden fees, including overdrafts, foreign transactions, minimum balances, and monthly expenses.

Cons

- Mobile check deposits are only available if users have direct deposits, potentially limiting accessibility for some users.

- Chime does not allow the opening of joint accounts, restricting shared financial management.

- Depositing cash through partners like Walmart or 7-Eleven may incur additional costs.

Sending Limits

- Chime’s ‘SpotMe’ program offers unlimited overdraft limits, ranging from $40 to $200.

- Users are automatically approved for a credit limit, starting at $20, with the potential to increase based on repayment history.

Data Security

- Chime’s commitment to transparency in fee structures aligns with security practices, ensuring users are informed about financial transactions.

- Chime’s digital banking model includes secure features like early direct deposit, contributing to a secure financial experience.

3. Cash App®

Cash App emerges as a dynamic apps like Zelle, offering a versatile platform for swift money transfers and unique financial functionalities.

With its user-friendly interface and fee-free debit card and bank account transfer options, Cash App stands out as a robust choice. However, users must weigh the lack of FDIC insurance, non-cancellable transactions, and fees for instant transfers.

The app’s sending limits, identity verification options, and commitment to data security through encryption and two-factor authentication further define its role in the digital payment landscape.

Cash App provides a distinctive blend of convenience and financial opportunities in a realm abundant with alternatives.

Pros

- Cash App allows users to send and receive money without transaction fees for debit card and bank account transfers.

- It offers stock and Bitcoin investing opportunities, providing users diversified financial functionalities.

- Cash App provides a debit card for easy cash withdrawals and purchases.

- The app’s straightforward interface enhances the user experience, making transactions accessible to a broad audience.

Cons

- Cash App is only FDIC-insured if users have a Cash Card, potentially impacting the security of funds.

- Once transactions are accepted, they cannot be canceled, introducing a limitation in user control.

- While some transfers are free, fees are applicable for instant transfers, adding a cost element to specific transactions.

Sending Limits

- Cash App imposes daily and weekly sending limits, restricting users to a maximum of $250 per week and up to $1,000 per month.

- Users can increase their transfer limits by verifying their identity and linking a bank account.

Data Security

- Cash App employs encryption technology to safeguard user data and transactions, ensuring a secure environment.

- Users can enhance security by setting up two-factor authentication and adding protection to their accounts.

4. Stripe

Stripe emerges as a robust apps like Zelle, particularly tailored for businesses seeking seamless payment solutions.

With over a decade of experience, Stripe offers an intuitive interface supporting various payment methods and international currencies. The absence of setup, cancellation, or monthly fees adds to its appeal, complemented by 24/7 customer support.

However, the open API and tools may pose challenges for those without software development experience, and high-risk merchants could face account freeze risks.

Stripe’s transaction fees are transparent, and its PCI Level 1 certification, HTTPS, and TLS usage ensure robust data security.

Pros

- Stripe distinguishes itself by not charging setup, cancellation, or monthly fees.

- It supports many payment methods, including wire transfers, major credit/debit cards, and digital wallets.

- Offering over 135 currencies, Stripe facilitates global transactions with ease.

- Users can create a personalized online checkout experience to suit their business needs.

- Stripe provides around-the-clock customer support, ensuring assistance when needed.

Cons

- The open API and tools may be challenging for users without software development experience.

- While robust for online sales, Stripe has limited functionality for in-person transactions.

- High-risk merchants may encounter account freeze or termination issues.

Sending Limits

- Stripe imposes a limit of $999,999.99 for single transactions.

Data Security

- Stripe’s PCI Level 1 Service Provider certification ensures adherence to stringent security standards.

- AES-256 encryption, HTTPS, and TLS guarantee secure connections for user data protection.

5. Paypal®

PayPal is a formidable Zelle alternative, offering a contract-free payment solution for merchants and consumers.

Its versatility allows businesses to leverage payment portals, management services, and financing options, while consumers can utilize PayPal for secure and private transactions, invoice payments, money transfers, and online purchases.

Despite its popularity, PayPal faces criticisms for poor customer service, higher fees, and hefty chargeback fees, including a reputation for freezing funds without notice.

While offering convenience, PayPal’s per-transaction fees range from 2.29% to 3.49%, and spending limits exist until account verification.

Pros

- PayPal supports transactions with all major card brands, enhancing accessibility.

- It seamlessly integrates as a payment gateway with eCommerce shopping carts, simplifying the payment process.

- Users can send and receive payments in 25 currencies, promoting global transactions.

- Merchants can accept customer payments with or without a PayPal account, broadening the user base.

Cons

- PayPal faces criticism for its poor customer service reputation.

- Compared to other platforms, PayPal is known for having higher transaction fees.

- The platform imposes hefty chargeback fees, impacting businesses.

- Funds can take up to three days to clear, potentially affecting transaction speed.

Sending Limits

- Without verification, PayPal for Business limitations transfers to $4,000.

- Verified accounts can send around $60,000 per transaction, with some currencies facing individual transaction limits of up to $10,000.

- There is no limit on the total amount users can transfer in a day.

Data Security

- PayPal emphasizes secure and private transactions for users, ensuring the confidentiality of financial information.

- The platform employs encryption technology to safeguard user data during transactions, maintaining a secure payment environment.

6. Apple Cash®

Apple Pay, specifically Apple Cash, emerges as a distinctive Zelle alternative for users, seamlessly integrating with Apple services and providing a user-friendly experience.

While its ease of use and cashback rewards enhance its appeal, limitations arise as it’s exclusive to Apple users and may need to be compatible with older iPhone generations.

Transfers are convenient within the Apple ecosystem, but funds can only be transferred between devices.

With sending limits ranging from $1 to $10,000 per message and robust data security features like end-to-end encryption and Touch ID/Face ID authorization, Apple Cash offers a secure and convenient payment option for users within the Apple ecosystem.

Pros

- Apple Cash integrates seamlessly with Apple services, providing a cohesive user experience.

- The platform is easy to use, especially within the Apple ecosystem.

- Users can enjoy cashback rewards as an added transaction incentive.

Cons

- Limited to Apple users, excluding non-Apple device users.

- It may not be compatible with older iPhone generations, limiting accessibility.

- Funds can only be transferred between Apple devices, restricting cross-device functionality.

Sending Limits

- Users can send or receive messages starting with $1 and up to $10,000.

- There’s a weekly sending or receiving limit of $10,000, and the maximum balance that can be held is $20,000.

Data Security

- Apple Cash employs end-to-end encryption for secure transactions.

- Touch ID or Face ID is required for transaction approval, adding an extra layer of security.

- Transactions are monitored for fraud and unauthorized activity, ensuring financial safety.

- Two-factor authentication with the Apple ID is required for payments, further enhancing data security.

7. Google Pay®

Google Pay is a versatile Zelle alternative with broad compatibility, allowing users to make online secure payments.

While its layered security measures enhance safety, limitations arise with NFC technology and its availability in certain countries. The platform offers additional uses beyond transactions, but bank participation may be limited.

Robust recordkeeping is a benefit, although bank account transfers may be slower. Google Pay imposes maximum limits of $2,000 per single transaction, $2,500 daily total, and up to 15 daily transactions.

It encrypts payment data for online security, positioning itself as a reliable and feature-rich alternative to Zelle.

Pros

- Google Pay is widely compatible, making it accessible across various platforms.

- The online platform employs multiple layers of security to ensure safe transactions.

- Beyond transactions, Google Pay offers additional functionalities, enhancing its utility.

- Google Pay maintains robust recordkeeping, aiding users in tracking their financial activities.

Cons

- The use of NFC technology is a limitation, potentially impacting certain transactions.

- Google Pay may have limited availability in certain countries, restricting its global reach.

- The list of participating banks may be limited, affecting the user base.

- Transfers to bank accounts may be slower, posing a drawback for users seeking faster transactions.

Sending Limits

- The maximum amount for a single transaction is USD 2,000.

- The daily maximum total transaction amount is USD 2,500.

- Users can perform up to 15 transactions per day.

Data Security

- Google Pay encrypts payment data when users pay online, ensuring the safety of sensitive information.

- The platform prioritizes secure transactions, instilling confidence in users regarding the safety of their payments.

8. Payoneer

Payoneer emerges as a robust Zelle alternative, especially for businesses with a global reach. Payoneer operates in over 200 countries, facilitating secure and scalable transactions for freelancers, digital marketers, and e-commerce sellers.

With withdrawal limits of up to $5,000 per day and 30 withdrawals daily, Payoneer offers flexibility. While receiving payments from other Payoneer customers is free, transactions from non-Payoneer clients may incur a 1–3 percent fee.

The platform prioritizes security through regular audits and risk assessments, ensuring safe financial transactions.

Payoneer’s global presence, low costs, and comprehensive digital payment services make it a preferred choice for international freelancers and businesses.

Pros

- Payoneer operates in over 200 countries, making it a versatile choice for international transactions.

- Users can withdraw up to $5,000 per day and make 30 withdrawals daily, providing flexibility.

- Payoneer offers relatively low fees, enhancing its affordability for freelancers and businesses.

- It provides various digital payment services, including a cashflow solution for e-commerce vendors.

- Payoneer allows users to pay VAT directly from their accounts, streamlining financial processes.

Cons

- Payments from clients not using Payoneer may incur a 1–3 percent fee, depending on the payment method.

- In cases of bank risk factors, Payoneer may move funds to safer banks, potentially causing temporary disruptions.

Sending Limits

- Users can withdraw up to $5,000 daily with 30 daily withdrawals.

- Payoneer limits point-of-sale transactions to 30 per day with a total daily limit of $2,500.

Data Security

- Payoneer payments are conducted through a secure financial platform that undergoes regular audits.

- Payoneer’s Risk Committee assesses risk rates and ensures secure fund management by moving money to safer banks.

- Payoneer collects personal information for user identification, including name, date of birth, IP address, and email address.

9. Venmo

Venmo is a popular Zelle alternative, functioning as a social payment app with digital wallet capabilities.

Users can store funds in the app, simplifying money transfers to friends and family without immediate withdrawals from their bank accounts. Account setup involves linking a bank account, debit, or credit card; transactions are free when using the former.

Venmo’s socially engaging interface and wide acceptance make it a preferred choice. While it excels in user ratings and ease of use, privacy settings and transaction visibility can be adjusted.

However, users should note potential delays in cashing out to a bank account.

Pros

- Venmo is highly rated on iOS and Android platforms, ensuring a positive user experience.

- Transactions are free when linking a bank account, debit card, or prepaid card.

- Venmo offers a social component, displaying transactions on a news feed without specific amounts.

- Users can adjust privacy settings to control who sees their transactions for added confidentiality.

Cons

- Using a credit card incurs a 3% transaction fee, involving some users’ costs.

- Cashing out to a bank account may take one to three business days, causing potential delays.

Sending Limits

After identification verification, individuals may contribute up to $60,000 weekly, giving them flexibility.

Data Security

- Venmo ensures user security through identity verification during setup.

- Users control privacy settings, choosing who can view transactions.

- Funds received appear instantly, with bank transfers taking 1-3 days for added security.

10. Wise

Wise is a global money transfer service distinguishing itself with transparency on exchange rates. While not always the cheapest option, it avoids unfair exchange rates that are ordinary in traditional banks.

With over 13 million users, Wise enables international transactions worth £8 billion monthly. Registration is user-friendly, offering alternatives like Apple, Facebook, or Google accounts.

Identity verification is required, but Wise’s pricing depends on the amount, currency, and payment method using the mid-market exchange rate.

Although not ideal for Indian users seeking debit card features, Wise excels for large transfers and offers a multi-currency account.

Pros

- Wise avoids marked-up exchange rates, providing transparency and fairness.

- Easy account setup with Apple, Facebook, or Google account registration options.

- Lower fees for substantial sums make Wise advantageous for large transfers.

- Wise offers a free multi-currency account, facilitating transactions in various currencies.

Cons

- Wise may not be the most cost-effective option for users seeking the cheapest international transfers.

- Wise debit card features are not available for Indian users, limiting functionality.

Sending Limits

The minimum amount for sending INR to other currencies is INR 5,000.

Data Security

- Wise ensures secure transactions by verifying user identity through photo ID and proof of address.

- While initiating the first transfer may trigger identity verification, Wise prioritizes data protection.

Which Zelle Alternative Is Right For You?

Beem is one of the best Zelle alternative is right for you.

When choosing the best Zelle alternative:

- Consider transaction fees, supported features, and international capabilities.

- Assess if the platform aligns with your usage patterns, such as personal transfers or business payments.

- Evaluate the app’s security measures, user reviews, and customer support.

- Look for flexibility in sending limits and diverse payment methods.

- Additionally, check for integration with other apps and websites for seamless transactions.

The best alternative should cater to your needs, whether low fees, international transfers, or user-friendly features, ensuring a tailored and efficient payment experience.

Also Read: Why Zelle Won’t Let Me Send Money to Someone

Conclusion

When seeking a Zelle alternative, the choice depends on your unique financial needs. Beem stands out with its multifaceted financial management, while Chime offers fee-free overdraft protection.

Cash App provides versatility with stock and Bitcoin investing, and Wise ensures transparency in exchange rates for international transfers.

Apple Cash and Google Pay prioritize seamless integration and security within their ecosystems. Stripe caters to businesses, and Venmo’s social payment app is widely accepted.

Payoneer excels in global transactions for freelancers and businesses. Consider factors like fees, security, and specific features to find the alternative that best suits your requirements.