Table of Contents

Cash advance apps have a complicated reputation, and some of it is deserved. Using Beem without long-term debt cycles represents a different approach, designed to give users short-term flexibility without encouraging repeat borrowing.

When short-term borrowing tools are used to patch a structural income problem, each advance delays rather than solves the underlying issue, leaving users more financially constrained with every passing month. That cycle is real, damaging, and exactly what Beem is designed to help users avoid.

The distinction between using a cash advance as a bridge versus a crutch comes down to one question: Is the gap a timing problem or an income problem? A timing problem resolves when the next paycheck arrives. An income problem does not, and no cash advance product can substitute for income that is not there. Understanding that distinction is what separates users who benefit from Beem from those who become dependent on it.

Understanding What a Debt Cycle Actually Is

The Anatomy of a Cash Advance Debt Cycle

A debt cycle begins innocuously. An unexpected expense arises, an advance is taken, and repaid when the next paycheck arrives. The problem begins when repaying the advance leaves the account short for the current pay period’s expenses. A second advance covers that shortfall. The next paycheck covers both, but just barely, leaving the account thin and the cycle repeating.

With high-interest products, this compounds rapidly because each advance costs more than the original shortfall. Even with a zero-interest product like Everdraft, the cycle can persist if the underlying cash flow math does not support both repaying the advance and covering normal expenses from the same paycheck. The dependency becomes the problem, not the cost.

The Difference Between a Bridge and a Crutch

A bridge connects two points that income would normally connect if timing were different. A bill is due Wednesday, the paycheck arrives Friday, the advance bridges three days, and next month you may not need it at all.

A crutch compensates for something that is not there. You take an advance because income is not sufficient to cover expenses even after it arrives. Repaying leaves you short, so another advance follows earlier in the next cycle. The crutch is doing structural work that income should be doing, and no bridge product can substitute for that indefinitely.

People Also Read: Beem App Review

Why Beem’s Design Reduces Debt Cycle Risk

Zero Interest Eliminates Compounding Cost

The primary mechanism by which payday loan cycles become inescapable is compounding interest. At a typical payday loan APR of 400 percent, a $300 advance costs $345 to repay in two weeks. If the borrower cannot cover the full amount, the loan rolls over, and fees accumulate again. The debt grows faster than the ability to repay it.

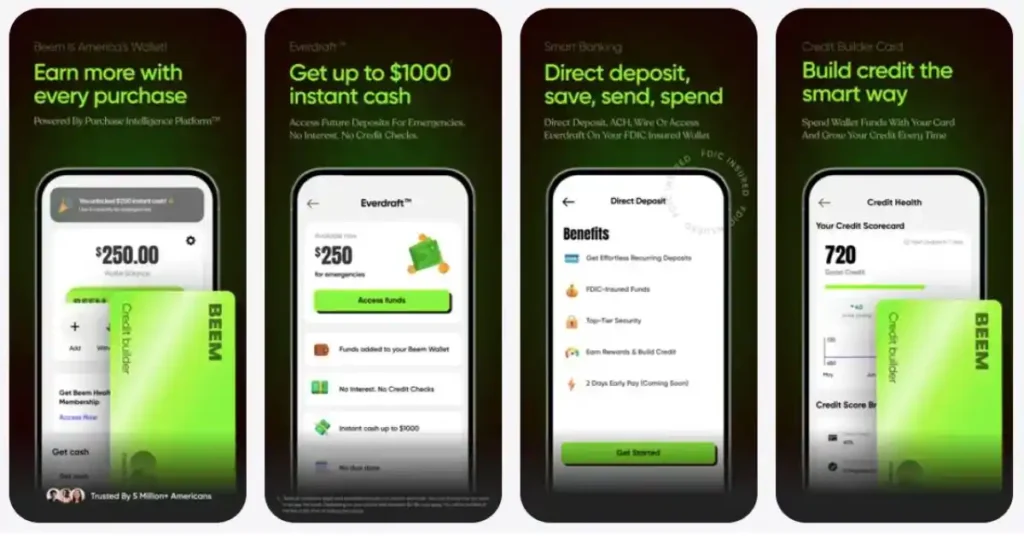

Everdraft charges zero interest. The $300 advance must be repaid in full regardless of how many pay cycles pass. This eliminates the compounding cost mechanism that makes payday cycles structurally inescapable. With Everdraft, the ceiling on harm is the original advance amount, not a number that grows indefinitely.

Repayment Aligned With Income Arrivals

Everdraft repayment is triggered by incoming deposits rather than a fixed calendar deadline. This alignment means the repayment event and the income event occur simultaneously, reducing the risk that repayment occurs before income arrives and leaving the account short of normal expenses.

No Rollover Mechanism

Payday loans are frequently rolled over when borrowers cannot afford full repayment, with new fees added each time. Beem does not offer a rollover mechanism. Advances repay when deposits arrive, removing one of the key structural features that deepen debt cycles over time.

Limits That Reflect Real Financial Capacity

Everdraft limits are based on the user’s actual financial profile rather than a maximum the platform can offer, regardless of repayment capacity. Users are less likely to access advances that exceed what their income can comfortably repay in a single cycle, reducing the risk of a repayment obligation that strains the next pay period.

People Also Read: BEEM Approval Process Explained

The Five Signs You Are Using Beem as a Bridge, Not a Crutch

Honest self-assessment is the most important tool in responsible cash advance use. Here are the five clearest signs that your Everdraft use is functioning as intended.

Sign 1: Your Advance Is Fully Repaid Each Cycle

If every Everdraft advance is fully repaid when your next income arrives and you begin the following pay cycle with your full paycheck available for normal expenses, you are using Everdraft as a bridge. The advance resolved a timing gap, and your financial position at the start of the new cycle is essentially the same as it would have been without the gap.

Sign 2: You Do Not Need an Advance Every Single Pay Cycle

If you request an Everdraft advance every pay period without exception, that pattern suggests the advance is functioning as a structural income supplement rather than an occasional timing tool. Occasional use, responding to specific timing mismatches rather than recurring every month, is the hallmark of bridge use.

Sign 3: The Gap You Are Bridging Has a Clear End Date

Timing gaps have natural end dates: the next paycheck, the delayed client payment, the benefit deposit that is three days late. If the gap you are bridging has a clear, specific end date when income will arrive and the advance will be repaid, you are bridging a timing gap. If the gap does not have a clear end date because it is created by income that is simply insufficient, you are using the advance to compensate for a structural shortfall.

Sign 4: Your Financial Position Is Stable or Improving Over Time

If your overall financial position, measured by your savings balance, your debt levels, and your ability to cover expenses without advances, is stable or improving over time, Everdraft is serving its intended purpose. If your financial position is deteriorating despite regular Everdraft use, the advance is not solving the underlying problem.

Sign 5: You Are Using Beem’s Financial Tools, Not Just Everdraft

Users who engage with BudgetGPT, PriceGPT, and Beem’s credit-building feature alongside Everdraft are using the platform as a comprehensive financial tool rather than a single-function advance dispenser. This broader engagement is a strong indicator of financially constructive use.

People Also Read: How Beem Fits Into a 50/30/20 Budget Framework

What to Do If You Recognize Dependency Forming

Recognizing a dependency pattern early is significantly easier to address than recognizing it after months of compounding financial stress. Here is what to do if you notice signs of dependency in your Everdraft use.

Step 1: Diagnose the Root Cause Honestly

Use BudgetGPT to analyze your income and spending over the past two to three months. Identify specifically why the gap exists in each cycle. Is it a timing issue, where income arrives slightly after expenses are due? Or is it a structural issue, where your total monthly income is genuinely insufficient to cover your total monthly expenses? The answer determines the appropriate response.

Step 2: Address Timing Gaps With Structural Solutions

If the gap is a timing issue, consider whether adjusting payment due dates with creditors could eliminate it without requiring an advance. Many utility companies, credit card issuers, and subscription services allow payment date changes with a simple request. Aligning payment due dates with your income deposit schedule is a permanent solution to timing gaps that currently require an advance.

Step 3: Address Income Shortfalls Directly

If the gap is a structural income shortfall, the solution is not a financial product. It is an income increase, an expense reduction, or both. Use BudgetGPT to identify specific expense categories where reduction is possible. Explore income opportunities, including additional hours, a side project, or a different employment arrangement. Everdraft can provide stability while you work on the structural solution, but it is not a substitute for making that structural change.

Step 4: Build a Liquidity Buffer to Eliminate the Need for Advances

The ultimate goal of responsible Everdraft use is to use it infrequently enough that building a small liquidity buffer becomes possible. Once a buffer of 1 to 2 weeks of essential expenses is in place, the timing gaps that currently require an advance can be absorbed by the buffer. This is the transition from reliance on Everdraft as a liquidity facility to reliance on your own accumulated resources, which is exactly the financial progression Beem’s tools are designed to support.

People Also Read: Beem Subscription Billing: When And How You’re Charged

How Beem’s Full Suite of Tools Supports Debt-Free Financial Progress

Everdraft is one component of a much broader financial platform. Using Beem’s complete toolkit transforms the platform from a cash advance service into a genuine financial wellness companion.

BudgetGPT: Identifying the Patterns That Create Gaps

BudgetGPT does not just track spending. It surfaces the specific patterns that create the cash flow gaps requiring advances in the first place. Regular use of BudgetGPT often reveals specific spending categories where small, consistent reductions would eliminate the timing gap, making advances unnecessary rather than just making them more affordable.

Credit Building: Creating Access to Better Financial Products

Beem’s credit-building feature reports positive payment activity to credit bureaus over time, gradually improving the credit profile that determines access to lower-cost financial products.

As your credit score improves, you gain access to personal loans with lower APRs, credit cards with more favorable terms, and eventually a financial product mix that provides liquidity at even lower cost than Everdraft. The credit-building feature turns responsible Beem use into a pathway toward a stronger overall financial position.

Beem Boost: Rewarding Responsible Use With Greater Capacity

Beem Boost increases Everdraft limits for users who demonstrate responsible use over time. Repaying advances promptly, maintaining positive account activity, and using the platform’s financial tools all contribute to Beem Boost eligibility. This reward structure creates a positive incentive for exactly the behaviors that prevent dependency: prompt repayment, stable account management, and financial tool engagement.

PriceGPT and DealsGPT: Reducing the Spending That Creates Gaps

PriceGPT and DealsGPT help users spend less on the things they are already buying. Every dollar saved through smarter purchasing reduces the cash flow gap that might otherwise require an advance. Over time, consistent use of these tools can meaningfully reduce the frequency of gaps, making Everdraft use increasingly occasional rather than increasingly routine.

Debt Cycle Risk: Beem Everdraft vs. High-Interest Alternatives

| Factor | Beem Everdraft | Payday Loan | Credit Card Cash Advance |

| Interest charged | 0% | 300% to 400% APR typical | 25% to 30% APR, immediate accrual |

| Rollover option | No | Yes, with additional fees | Yes, minimum payment extends the debt |

| Compounding cost risk | None | High | Moderate to high |

| Repayment alignment | With income deposits | Fixed next payday | Minimum monthly payment |

| Debt cycle risk | Low with responsible use | High structural risk | Moderate with minimum payments |

| Credit score impact | None | Sometimes | Yes, utilization and payment history |

| Transparency | Full upfront disclosure | Often obscured | Disclosed but complex |

People Also Read: What Makes Beem Different From Payday Stores in 2026?

Final Thoughts

The difference between a financial tool and a debt trap has never been the tool itself. It has always been the combination of the tool’s design and the user’s relationship with it.

Beem’s zero-interest model, income-aligned repayment, and absence of rollover mechanisms make it one of the least structurally risky cash advance tools available. But structural safety is only half the equation. The other half is the financial habits, honest self-assessment, and proactive gap management that responsible users bring to the platform.

Used as a bridge for genuine timing gaps, supported by BudgetGPT’s real-time financial awareness, and complemented by credit-building and savings habits that reduce advance frequency over time, Beem becomes a platform that genuinely improves financial stability rather than one that merely manages financial instability.

That progression from managing instability to building stability is the financial journey the Beem app is designed to support, and it begins with the intentional, eyes-open use described in this guide.

People Also Ask

1. Can Beem Everdraft create a debt cycle?

Everdraft’s zero-interest model eliminates the compounding cost that makes payday loan debt cycles structurally inescapable. However, dependency can still form if advances are used to compensate for a structural income shortfall rather than a timing gap. Responsible use means bridging genuine timing gaps, repaying promptly, and using BudgetGPT to address the underlying patterns that create gaps.

2. How do I know if I am using Everdraft responsibly?

The clearest indicator is whether each advance is fully repaid when the next paycheck arrives and whether you begin each new pay cycle with your full income available for normal expenses. If repaying an advance leaves you short in the current period and requires another advance, that pattern warrants a root cause review using BudgetGPT.

3. What should I do if I feel dependent on Everdraft?

Start with an honest root cause analysis using BudgetGPT to determine whether the gap is a timing issue or a structural income shortfall. Timing issues can often be resolved by adjusting payment due dates. Structural shortfalls require income growth or expense reduction.

4. How does Beem help users build financial independence over time?

Beem’s credit-building feature improves your credit profile, helping you access better financial products. BudgetGPT identifies spending patterns that create gaps. PriceGPT and DealsGPT reduce everyday spending. Beem Boost increases your Everdraft limit as you demonstrate responsible use.

5. Is there a limit to how often I can use Everdraft?

Everdraft advances are repaid before a new advance can be requested, which structurally prevents multiple simultaneous advances from accumulating. This built-in reset mechanism ensures each advance cycle is discrete and complete before the next begins, reducing the risk of multiple overlapping obligations that characterize more complex debt cycles.