If you have ever heard someone say they are “filing their taxes” or “waiting on their tax return,” you may have wondered what that actually means. Taxes can feel confusing at first, especially if you are filing for the first time or starting a new job. The good news is that once you understand the basics, the process becomes much easier to manage.

This beginner-friendly guide explains what a tax return is, why it matters, how to file taxes, and what to expect after you submit it.

Everything is explained in simple terms so you can feel confident handling your taxes without feeling overwhelmed.

What Is a Tax Return?

A tax return is a form or set of forms that you send to the Internal Revenue Service to report your income, expenses, and other financial details for the year. It tells the government how much money you earned, how much tax you already paid, and whether you owe more tax or are due a refund.

In most cases, when people say “tax return,” they are referring to the paperwork filed with the IRS. Technically, the money you get back is called a tax refund, but the two terms are often used interchangeably in everyday conversation.

Your tax return calculates your final tax bill for the year based on your income and tax situation.

Why Do You Have to File a Tax Return?

Filing a tax return is how the government checks that you paid the correct amount of taxes during the year. Most people have taxes withheld automatically from their paycheck, but that does not always mean the amount withheld was exact.

You may need to file a tax return to:

- Confirm you paid enough taxes

- Pay any remaining tax you owe

- Claim a refund if you overpaid

- Qualify for tax credits or deductions

- Stay compliant with federal tax laws

Failing to file when required can lead to penalties, interest, and problems down the road.

Who Needs to File a Tax Return?

Not everyone is required to file a tax return, but most working adults do. Whether you need to file depends on factors like your income, age, filing status, and type of income.

Generally, you must file a tax return if:

- Your income is above the IRS filing threshold for the year

- You are self-employed and earned $400 or more

- You had taxes withheld and want a refund

- You qualify for refundable credits like the Earned Income Tax Credit

Even if you are not required to file, it can still be beneficial if you are owed a refund.

Types of Income You Report on a Tax Return

A tax return includes more than just your paycheck. The IRS wants to know about most types of income you earned during the year.

Common income sources include:

- Wages from a job

- Freelance or contract income

- Tips and commissions

- Interest from savings accounts

- Investment income

- Unemployment benefits

- Gig work or side hustles

Each type of income is reported using specific forms, which are then summarized on your tax return.

What Is a Tax Refund?

A tax refund happens when you paid more taxes during the year than you actually owed. The IRS sends the extra money back to you after processing your tax return.

Refunds are common for people who:

- Had too much tax withheld from paychecks

- Qualify for tax credits

- Have dependents

- Earned less than expected during the year

Refunds are not free money. They are simply a return of your own money that you overpaid.

What If You Owe Taxes Instead?

If your tax return shows that you owe money, it means your withholding or estimated payments were not enough. This can happen if you:

- Are self-employed

- Have multiple income sources

- Did not update your withholding

- Earned more than expected

Owing taxes does not mean you did anything wrong. It just means you need to pay the remaining balance by the IRS deadline to avoid penalties.

Key Forms Used in a Tax Return

Understanding the most common tax forms can remove much of the confusion around filing a tax return. Each form serves a specific purpose and provides the IRS with details about your income and tax situation.

Knowing what these forms are and how they are used makes the filing process smoother and helps you avoid reporting errors.

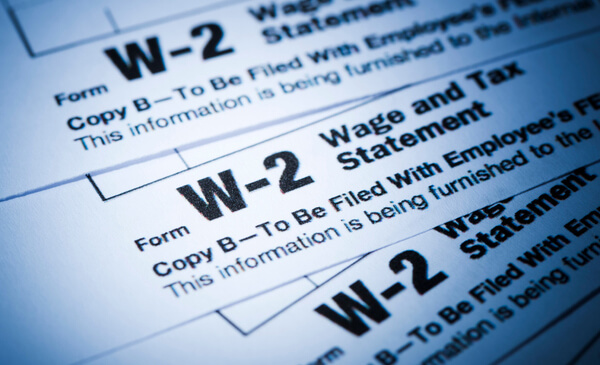

Form W-2

Form W-2 is used to report income earned as an employee. If you work for an employer, this is one of the most important documents you will receive during tax season. Your employer is required to send your W-2 by the end of January, either by mail or electronically.

The form shows your total wages for the year and how much federal, state, and other taxes were withheld from your paychecks. It may also include information about benefits such as retirement contributions or health insurance.

You use the details from your W-2 to accurately report your income and confirm whether the correct amount of tax was already paid on your behalf.

Form 1099

Form 1099 is used to report income earned outside of a traditional employer relationship. This typically applies to freelancers, independent contractors, gig workers, and people who earn side income. There are several types of 1099 forms, but they all serve the same purpose of reporting non-employee income.

If you received a 1099, it usually means taxes were not withheld from your payments. This income must still be reported on your tax return, and you may owe additional taxes on it. Even if you did not receive a 1099 for certain work, you are still responsible for reporting that income if you earned it.

Form 1040

Form 1040 is the main federal tax return form used by most individuals. It brings together all of your income information, deductions, credits, and tax payments to calculate your final tax outcome for the year.

On this form, you report income from W-2s, 1099s, and other sources, then apply deductions and credits to determine whether you owe taxes or are due a refund. Once completed, Form 1040 becomes your official tax return that you submit to the IRS, either electronically or by mail.

Filing Status Explained

Your filing status affects your tax rate and deductions. Choosing the correct status is important.

Common filing statuses include:

- Single

- Married filing jointly

- Married filing separately

- Head of household

- Qualifying surviving spouse

Your status depends on your marital and family situation as of the last day of the tax year.

Deductions vs Credits: What’s the Difference?

Tax deductions and tax credits both help lower how much you owe in taxes, but they do it in very different ways. Understanding this difference is important because it affects how much you actually save when you file your tax return.

Tax Deductions

Tax deductions reduce the amount of your income that is subject to tax. Instead of lowering your tax bill directly, deductions lower the portion of your income that the IRS uses to calculate your taxes.

For example, if you earned $50,000 and qualify for $5,000 in deductions, you are only taxed on $45,000 of income. Common deductions include student loan interest, retirement contributions, and certain education or business expenses.

The value of a deduction depends on your tax bracket. The higher your tax rate, the more you benefit from each dollar deducted.

Tax Credits

Tax credits reduce your tax bill dollar for dollar. This means they directly lower the amount of tax you owe, making them more powerful than deductions in most cases.

For instance, if you owe $2,000 in taxes and qualify for a $1,000 tax credit, your tax bill drops to $1,000. Some credits are refundable, which means they can increase your refund even if your tax bill is already zero. Because credits provide a direct reduction in taxes owed, they are generally more valuable than deductions when you qualify for them.

Standard Deduction vs Itemized Deductions

When filing a tax return, you must choose between taking the standard deduction or itemizing your deductions. This choice directly affects how much of your income is taxed, so understanding how each option works can help you reduce your overall tax bill.

Standard Deduction

The standard deduction is a fixed dollar amount set by the IRS that reduces your taxable income automatically. It is based on your filing status, such as single or married filing jointly. Most taxpayers choose the standard deduction because it is simple, requires no extra documentation, and often provides a larger tax benefit for people with straightforward finances.

With the standard deduction, you do not need to track or report individual expenses. This makes filing faster and reduces the risk of errors or IRS questions later on.

Itemized Deductions

Itemized deductions allow you to list specific qualifying expenses you paid during the year instead of taking the standard deduction. These expenses are added together, and the total amount reduces your taxable income.

Itemizing may make sense if your eligible expenses are higher than the standard deduction. Common itemized deductions include high medical expenses that exceed certain limits, large amounts of mortgage interest, significant charitable donations, and certain state and local taxes. Itemizing requires good recordkeeping, including receipts and statements, since you may need to prove these expenses if asked.

Choosing the Right Option

You can only choose one option each year, either the standard deduction or itemized deductions, not both. Most tax software automatically compares the two and applies whichever option gives you the better result.

Choosing the right deduction method can lead to meaningful tax savings and help ensure your return is filed accurately.

How to File a Tax Return

There are several ways to file your tax return, and the best option depends on how simple or complex your tax situation is. Your comfort level, budget, and time availability can also influence which method makes the most sense for you.

File Online

Filing online is the most popular option, especially for beginners. Tax software walks you through the process step by step, asking simple questions and filling in the correct forms based on your answers. These platforms automatically calculate your taxes, apply deductions and credits, and check for common mistakes before submission.

Electronic filing is also the fastest way to receive a refund if you are owed one. Many programs allow you to import forms like W-2s and 1099s directly, which reduces manual entry and helps prevent errors.

File With a Tax Professional

If your taxes are more complicated, working with a tax professional may be a better choice. A certified public accountant or tax preparer can help if you are self-employed, own a business, have investment income, or experienced major life changes such as marriage or buying a home.

A professional can also help identify deductions and credits you may miss on your own and provide guidance if you owe taxes. While this option costs more, it offers added confidence and personalized advice.

File by Mail

Filing a paper tax return by mail is still an option, though it is less common today. This method involves completing forms manually and mailing them to the IRS. Paper filing is slower, and refunds take longer to process. It also increases the chance of math errors or missing information.

If you choose to file by mail, double-check all entries, sign the return, and keep copies for your records. Using certified mail can provide proof of delivery.

Important Tax Deadlines to Know

The federal tax filing deadline is usually April 15. If that date falls on a weekend or holiday, the deadline moves to the next business day.

You can request an extension to file, but not to pay. Any taxes owed are still due by the original deadline.

What Happens After You File?

After you submit your tax return, the IRS reviews it for accuracy.

If everything checks out:

- Refunds are usually issued within a few weeks

- Payments are processed if you owe taxes

If there is an issue, the IRS may contact you for clarification or corrections.

Common Tax Filing Mistakes to Avoid

Mistakes can delay refunds or trigger IRS notices.

Common errors include:

- Incorrect Social Security numbers

- Math mistakes

- Missing income

- Wrong filing status

- Forgetting to sign the return

Double-checking your information helps prevent these problems.

What If You Cannot Pay Your Taxes Right Away?

If you owe taxes and cannot pay in full by the deadline, do not panic. The IRS offers payment plans and other options.

In the short term, covering tax payments can be stressful, especially if the bill comes unexpectedly. Some people use temporary cash solutions to handle immediate obligations.

For example, Beem Everdraft™ allows eligible users to access $10 to $1,000 in instant cash advances when funds are tight. This can help cover essential expenses or tax payments while you work out a longer-term plan.

On top of your unlocked Everdraft™ amount, the Beem Boost feature can help you unlock additional cash, giving you more flexibility when timing matters.

How Long Should You Keep Tax Records?

The IRS generally recommends keeping tax records for at least three years. In some cases, longer retention is wise, especially if you:

- Underreported income

- Claimed certain deductions

- Own a business

Keeping digital copies can make recordkeeping easier.

How Tax Returns Affect Your Financial Life

Your tax return plays a role beyond tax season.

It may be used to:

- Verify income for loans

- Apply for financial aid

- Prove eligibility for benefits

- Support rental or mortgage applications

Filing accurately and on time helps protect your financial reputation.

Filing Taxes for the First Time

Filing taxes for the first time can feel intimidating, but the process is more manageable than it seems once you understand the basics. Everyone starts somewhere, and first-time filers often have simpler tax situations, which makes this a good opportunity to build confidence and good habits early.

Start by Gathering Your Documents

Before you file, collect all the documents that show how much money you earned and how much tax was already paid. This usually includes Form W-2 from an employer or Form 1099 if you earned income from freelance, gig, or contract work. You may also need bank statements, records of interest earned, or documents related to education expenses if applicable.

Having everything in one place saves time and reduces the risk of forgetting income, which can cause issues later.

Choose the Right Filing Method

Most first-time filers benefit from using online tax software. These platforms are designed for beginners and explain each step in simple language. You answer basic questions about your income and situation, and the software fills out the correct forms for you. It also checks for common mistakes before you submit your return.

If your situation feels confusing or you are unsure about certain income sources, a tax professional can provide reassurance and guidance.

Understand Your Filing Status

Your filing status affects your tax rate and deduction amount. Common options include single or head of household, depending on your living situation and dependents. Choosing the correct status is important because it directly impacts how much tax you owe or how much refund you may receive.

Review Before You Submit

Take time to review your tax return before submitting it. Double-check your name, Social Security number, income amounts, and bank details for direct deposit. Small errors can delay refunds or lead to IRS notices, even on simple returns.

What to Expect After Filing

Once you file your first tax return, the IRS processes it and determines whether you owe taxes or are due a refund. Refunds filed electronically are usually issued within a few weeks. If you owe taxes, payment is typically due by the filing deadline.

If money is tight and you need short-term help covering expenses or tax-related costs, tools like Beem Everdraft™ can provide temporary relief. Eligible users can access $10 to $1,000 in instant cash advances, and the Beem Boost feature may unlock additional cash when timing matters.

Filing taxes for the first time is a learning experience. With preparation and attention to detail, it becomes a routine task that gets easier every year.

Self-Employed and Freelance Tax Returns

If you are self-employed, your tax return includes additional responsibilities.

You may need to:

- Report business income and expenses

- Pay self-employment tax

- Make estimated quarterly payments

Keeping organized records throughout the year makes filing much easier.

What to Do If You Make a Mistake on Your Tax Return

Mistakes happen. If you realize an error after filing, you can submit an amended return to correct it.

Fixing errors promptly helps avoid penalties and confusion later.

Understanding State Tax Returns

In addition to your federal tax return, you may also need to file a state tax return. State rules vary, but the process is similar.

Some states have income tax, while others do not. Always check your state’s requirements.

Tips to Make Filing Easier Next Year

A little preparation goes a long way.

Helpful habits include:

- Updating withholding when your income changes

- Tracking expenses year-round

- Saving tax documents in one place

- Reviewing your tax situation annually

These steps can reduce stress and improve accuracy.

Final Thoughts on Tax Returns

A tax return is simply a yearly snapshot of your financial activity, used to make sure your taxes are accurate. While the process may seem complicated at first, understanding the basics makes it far more manageable.

Filing on time, reporting income honestly, and knowing your options if you owe taxes can help you stay in control of your finances. And if cash flow becomes a challenge during tax season, short-term tools like Beem Everdraft™ can provide temporary support while you take care of important obligations.

With the right knowledge and preparation, filing a tax return becomes less of a burden and more of a routine financial task you can handle with confidence.